CONTENTS OF LAST ISSUE

Here is accounting coming, rocking and sighing

According to the established tradition, at the beginning of the year, we will cover the main changes in the principles of accounting and accounting reporting.

For several years, legislative changes has mainly focused on the intention to increase business transparency, universal electronic document management, and alignment with IFRS. Since 2021, a few more steps have been taken.

“Balance” income tax

Starting from 2020, organizations, except for those applying simplified accounting methods, have to apply revised Russian Accounting Regulation (PBU) 18/02 “Accounting for Corporate Income Tax Calculations”. Despite the fact that the latest revision has been put into effect since the beginning of 2020, many accountants will deal with it only in the 1st quarter of 2021 when preparing annual accounting statements for 2020. We have already discussed the procedure for applying the balance method, so there is no need to dwell on the income tax in detail, but it is worth mentioning the main aspect.

The main change in the accounting procedure for corporate income tax calculations is the change of the “cost” method to the balance method and recognition of most differences as temporary.

The revised PBU 18/02 expressly classify the following accounting events as temporary differences:

- Revaluation of assets for accounting purposes;

- Impairment of financial investments for accounting purposes;

- Differences between the rules for creating bad debt provisions;

- Recognition of estimated liabilities.

Materials and supplies inventories are now INVENTORIES

Since January 1, 2021, PBU 5/01 “Accounting of Materials and Supplies Inventories” has become invalid. Now organizations shall apply Federal Accounting Standard 5/2019 “Inventories”. In 2020, application of the standard was voluntary, now the standard has become mandatory for all organizations, except for microenterprises that apply simplified accounting methods, including simplified accounting statements, and public sector organizations.

What does this mean in real terms? Let us briefly review the main changes.

It is possible not to apply the standard to accounting of inventory held for management purposes. Now purchased office supplies may be recognized as current expenses in the period at the time of their purchase. In order to apply this approach, an organization should fix this accounting method in the accounting policy.

It is no longer possible to classify low-value fixed assets (worth up to 40,000 rubles) as materials and supplies inventories and to recognize the costs of their acquisition at the same time. If an asset is planned to be used in the organization for more than 12 months, such an asset should be recognized as a fixed asset (subject to other conditions for recognition of the fixed asset).

The cost value of inventories may now include the interest associated with the acquisition (creation) of inventories, which shall be included in the cost of the investment asset.

The actual cost of inventory is formed taking into account discounts (reduced by the discount amount). This rule shall not be applied by organizations entitled to apply simplified accounting methods.

In case inventories are acquired in installments for a long term, the cost of goods that would be paid as an immediate payment shall be recognized as the cost value; the difference should be accounted for as interest on loan obligations. This rule shall not be applied by organizations entitled to apply simplified accounting methods.

Inventories that are paid for in non-monetary funds are estimated at the fair value of the property transferred to pay for the inventories. The fair value is an estimate based on market data, rather than an entity-specific estimate. If it is not possible to estimate the property transferred to pay for the inventories at the fair value, the estimate is made at the fair value of the inventories.

Organizations entitled to apply simplified accounting methods may determine the actual value of such inventories as the sum of the carrying amount of transferred assets.

Inventories received by an entity free of charge shall be estimated at the fair value of such inventories.

Terms “direct costs” and “indirect costs” are introduced to the Federal Accounting Standard. The actual cost value of the finished product shall be determined taking into account direct and indirect costs (procedures for distribution of indirect costs shall be determined by the organization itself).

Work in progress is officially classified as inventories and the procedure for forming the value of work in progress is fixed. The standard also specifies a list of costs that are not included in the cost value of work in progress and finished products.

If the capacity utilization in the reporting period has significantly decreased compared to the normal level, semi-fixed production costs shall be included in the cost value of inventories to the extent proportional to the volume of products produced in the reporting period relative to the normal level of utilization. The remaining part of semi-fixed production costs shall be included in the financial results for the reporting period as part of expenses for ordinary activities.

The procedure for subsequent evaluation has been changed. Inventories shall be measured as of the reporting date at the lower of their actual cost value and estimated sale price less costs required to prepare and sell the inventories. Organizations entitled to apply simplified accounting methods may estimate inventories as of the reporting date at the actual cost value.

Quite a lot of changes have been made, and they will significantly affect the procedure for accounting of inventories (former materials and supplies inventories). Consequences of changes to accounting policies due to the start of the standard implementation may be reflected retrospectively or prospectively at the choice of the organization (to be fixed in the accounting policy). The applicable procedure should be disclosed in the accounting statements.

New federal accounting standards are on their way

By Order of the Russian Ministry of Finance No. 204н dated September 17, 2020, two new federal accounting standards were approved and put into effect:

- Federal Accounting Standard 6/2020 “Fixed Assets”;

- Federal Accounting Standard 26/2020 “Capital Investments”.

These standards will become mandatory from 2022, but the organization may decide to apply the standards ahead of time.

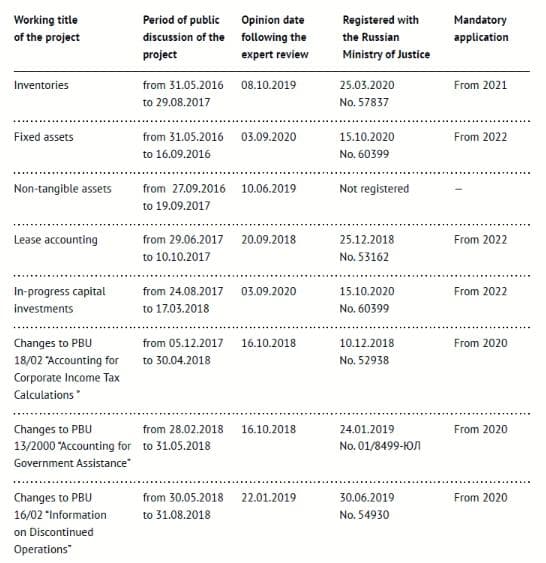

Below is a summary of the progress in the development of federal accounting standards (development of federal standards includes changes in Accounting Regulations):

As the table shows, public discussion of all projects will be completed by the end of the first quarter of 2021. Standards, which will be approved and published in the 1st half of 2021, may become mandatory starting from 2022. So far, three standards will be mandatory starting from 2022: Federal Accounting Standard 6/2020 “Fixed Assets”, Federal Accounting Standard 26/2020 “Capital Investments”, and Federal Accounting Standard 25/2018 “Lease Accounting”.

It should be noted that alignment of Russian accounting with international accounting irrevocably distances the accounting procedure from the rules of tax accounting. Therefore, hopes for unified accounting in Russian organizations have not materialized and are unlikely to materialize in the near future.

Direct payments to the Social Insurance Fund, cancellation of the credit system

Since January 1, 2021, numerous regions, including Moscow, have joined the Direct Payments project.

The Direct Payments project aims at changing the payment of benefits under mandatory social insurance against temporary disability and maternity leave and applies to all insurers (employers) of employers and citizens working under contracts.

Goals and objectives of the project are:

- Guarantee of full and timely payment of benefits;

- Ensured transparency in the assessment and payment of benefits;

- No diversion of the employer’s working capital;

- Improvement of the social security of individuals, if the employer has financial problems or terminated its activities;

- Development of electronic document exchange between project participants.

From January 1, 2021, the employer shall not pay temporary disability benefits at the expense of the Social Insurance Fund (hereinafter, the Fund), but shall only submit documents to the Fund. The employee shall receive payments directly from the Fund.

Since payments are not made by the employer, the “credit” system ceases to exist. Now charged contributions to compulsory social insurance will not be reduced by the amount of employee benefits.

NB: calculation of benefits payable to employees shall remain the employer’s responsibility. The calculation procedure shall remain unchanged.

The new rules apply to the following types of benefits:

- Temporary disability benefit (including in connection with job-related accidents and occupational diseases);

- Maternity benefit;

- One-time benefit for women registered in medical institutions for early pregnancy;

- One-time child birth benefit;

- Monthly child care benefit;

- Paid leave for a person injured at work (in addition to the annual paid leave).

Now actions of the employer when receiving documents from the employee confirming the right to receive benefits are as follows:

- Receipt and verification of employee’s documents;

- Preparation of an Application for payment (recalculation) of benefits (payment of leave) in the form approved by Order of the Social Insurance Fund of the Russian Federation No. 578 dated 24.11.2017;

- Calculation of the benefit payable to the employee;

- Payment of the benefit to the employee for the first three days of temporary disability;

- Within 5 calendar days, filling in and submitting the register of information to the Fund in the form approved by Order of the Social Insurance Fund of the Russian Federation No. 579 dated 24.11.2017;

The Fund shall do the rest: check the data and pay the benefit to the insured person.

NB: pregnant women and citizens who have been exposed to radiation will have to apply for and receive the MIR card.

The following types of benefits may only be transferred to the MIR card:

- Maternity benefit;

- One-time benefit for women registered in medical organizations for early pregnancy;

- One-time child birth benefit;

- Monthly child care benefit;

- Payments to citizens exposed to radiation as a result of the Chernobyl disaster, the accident at the Mayak Production Association and discharges of radioactive waste into the Techa river, and following nuclear tests at the Semipalatinsk test site.

When filling out the Calculation of insurance premiums, the following issues should be taken into account:

- Code 1 (Direct Payments) should be indicated in field 001 of Appendix 2 to section 1;

- In Appendix 2 to section 1, lines 070 “Expenses for Payment of Insurance Coverage” and 080 “Expenses for Payment of Insurance Coverage Reimbursed by the Social Insurance Fund” should not be filled in;

- Appendices 3 and 4 to section 1 should not be filled in.

Calculation of accrued and paid insurance premiums for mandatory social insurance against job-related accidents and occupational diseases, as well as expenses for the payment of insurance coverage (form 4 – Social Insurance Fund of the Russian Federation):

- There is no need to fill in the data on benefits, since participants of the pilot project do not reduce insurance premiums by these amounts;

- Line 15 of table 2 should be filled in with a dash;

- There is no need to fill in table 3 and include it in the calculation.

This information is available on the official websites of the Federal Tax Service and the Social Insurance Fund.

Happy New Accounting!

This year, accountants will have a lot of work to do studying new standards and changes in accounting policies.

However, the changes introduced by the federal accounting standards will increase reliability of accounting and accounting statements.

Upon completion of the reforms, organizations that annually (or more often) transform Russian financial statements into IFRS will be able to at least reduce the number of transformation operations, and at most not to make a transformation at all, but to present Russian financial statements that meet international standards to the parent organization. This is what the reformers strive for.

A Russian accountant has always lived, lives and will live “keeping his finger on the pulse”, and this is a sign of professionalism. Happy New Accounting, colleagues!

Small business without audit

Starting from January 1, 2021, amendments to the law “On Auditing” became effective and increased the criteria for a mandatory audit of revenue and assets.

In the previous revision, an organization was required to conduct an audit of its accounting statements for 2020 if in the year preceding the reporting year its revenue exceeded 400 million rubles, or the value of assets exceeded 60 million rubles.

The new revision sets the criteria for a mandatory audit at the level of INCOME (not revenue) in the amount exceeding 800 million rubles per year, and the value of assets exceeding 400 million rubles.

Such amendments apply to the audit of accounting statements for 2020 (since statements are prepared and audited in 2021), except for cases where the organization was required to conduct a mandatory audit according to the criteria effective before the amendments were made and the auditor began the performance of the agreement at the time the amendments to the law on auditing became effective.

In other words, if a mandatory audit of accounting statements is carried out in several stages (intermediate stages in 2020), despite the increase in the criteria, it will remain mandatory. Starting from statements for 2021, an obligation to conduct an audit shall be discontinued if the mandatory audit criteria are not met.

Therefore, small businesses are exempt from the mandatory audit, which reduces business costs, but opens the door to bad faith entrepreneurs operating in the small business field.

Other Articles on Topics