CONTENTS OF LAST ISSUE

Income tax: once in writing, it is time to put it into practice

In November 2018, the Ministry of Finance of the Russian Federation amended Accounting Regulations “Accounting for Corporate Income Tax” PBU 18/02 (hereinafter, PBU 18/02), which are mandatory for accounting statements for 2020, i.e. for accounting from January 1, 2020. It became possible to apply the revised version on a voluntary basis from January 1, 2019.

We shall begin by covering the most significant changes made to PBU 18/02. We shall omit formalities and rules introduced for consolidated groups of taxpayers.

New terms – old substance

It should be noted that two terms were replaced throughout PBU 18/02:

Permanent became temporary

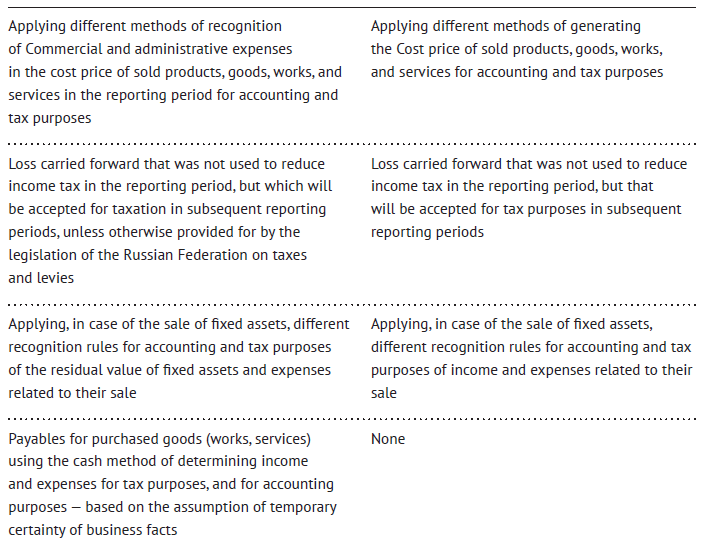

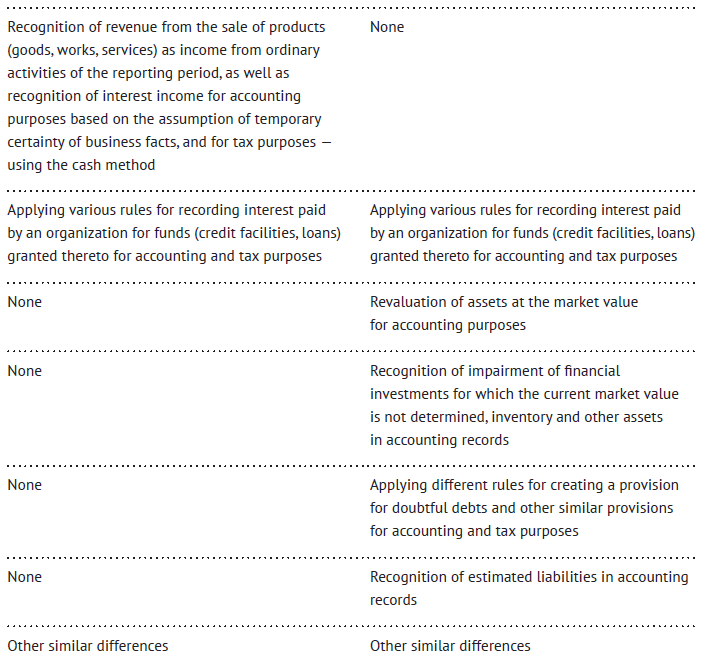

Below is the comparison between reasons for temporary differences in the previous and revised versions.

The table above shows that the revised version of PBU 18/02 expressly refers to the following business facts as temporary differences:

- Revaluation of assets for accounting purposes;

- Impairment of financial investments for accounting purposes;

- Differences between the rules for creating a provision for doubtful debts;

- Recognition of estimated liabilities.

Before the changes came into force, due to the lack of clear legal instructions an accountant had a choice regarding the classification of the said facts as temporary and permanent.

For example, in practice, differences in creating a provision for doubtful debts, provision for vacation payments, and provision for impairment of inventory for accounting purposes only were classified as permanent differences to simplify accounting. Now an accountant has no such option.

Permanent differences are now created only if income and/or expenses recognized for accounting purposes are never recognized for tax purposes and vice versa.

In other words, in accounting creating temporary differences is a feature, while creating permanent differences is an exception.

New calculation of differences

Prior to 2020, the practice of corporate income tax accounting meant determining permanent and temporary differences for income and expenses. The revised version introduces the balance method, which implies determination of temporary differences based on the difference between the book value of an asset (liability) and its value accepted for tax purposes.

This method provides for an option to refuse from the detailed recognition of permanent and temporary differences for each operation, although it does not prohibit their recognition in accounting.

Accounting options and accounting policy

A method of determining current income tax is fixed in the accounting policy of an organization. An organization may use the following methods to determine current income tax:

- Based on accounting data;

- Based on the income tax return.

In both cases, the amount of current income tax should correspond to the amount of the calculated income tax reflected in the corporate income tax return.

The method of determining current income tax based on accounting data (cost method) is a customary method used before the changes became effective.

The method of determining current income tax based on the income tax return (balance method) became widespread only after the changes considered herein became effective.

Therefore, given that the method of determining current corporate income tax based on accounting data remained in PBU 18/02, an organization may keep the customary method of determining current income tax, if it secures such a method in its accounting policy. However, this method is only applicable if the result corresponds to the calculation under the balance method. The cost method is based on the analysis of income and expenses, which makes it inconvenient as during each reporting period an accountant will have to conduct an audit calculating differences using the balance method. Accountants will have to develop their own methodology and will most likely need to maintain additional tables to account for arising differences.

Therefore, despite the frightening uncertainty of the new balance method, it is still worth changing the accounting method for corporate income tax from cost to balance one.

Retrospective restatement of balances

In accordance with the provisions of PBU 1/2008 “Accounting Policies of Organizations” changes in the accounting policy that significantly affect indicators of accounting statements should be reflected in the accounting statements retrospectively.

Retrospective recognition of consequences of changes in the accounting policy is adjusting the incoming balance under the item “Retained Earnings (Retained Loss)” and/or other balance sheet items as of the earliest date presented in the accounting (financial) statements, as well as values of related accounting items disclosed for each period presented in the accounting statements, as if the new accounting policy was applied from the moment of occurrence of the business facts of this type.

In other words, if the method of determining current corporate income tax is changed, an accountant will have to calculate the impact of changes on accounting statements and if such changes are significant will have to restate comparable data in the accounting statements for 2020.

Software and features of transaction

1C Program (section “Accounting Policy”) currently provides for three accounting methods for corporate income tax:

- Balance method;

- Balance method with recognition of permanent and temporary differences;

- Bost method.

As mentioned above, it is not advisable to use the cost method. Moreover, it is prohibited for use by organizations with separate divisions that apply different corporate income tax rates.

The balance method has two options: with and without recognition of permanent and temporary differences. The difference between them is that when using the balance method no “familiar” permanent differences and temporary differences will be formed.

If an accountant wants to keep them, then he/she will have to opt for the balance method with recognition of permanent and temporary differences.

When switching from the cost method to the balance method, provided that accounting and tax records are correctly formed, the program should automatically recalculate balances of accounts 09 “Deferred Tax Asset” and 77 “Deferred Tax Liability” in correspondence with account 84 “Retained Earnings (Retained Loss)” at the beginning of the period.

Practice of the balance method

Based solely on the text of PBU 18/02, it is not clear how to apply the new rules in practice. There are no official interpretations for the revised version of PBU 18/02, so it is possible to apply Recommendation P-102/2019-КпР “Procedure for Income Tax Accounting”, which was issued in April 2019 by Foundation “National Non-Governmental Accounting Regulator “Accounting Methodological Center” (hereinafter, the Recommendation). The said Recommendation was approved by the Committee on Recommendations. The text is published on the official website of the Foundation.

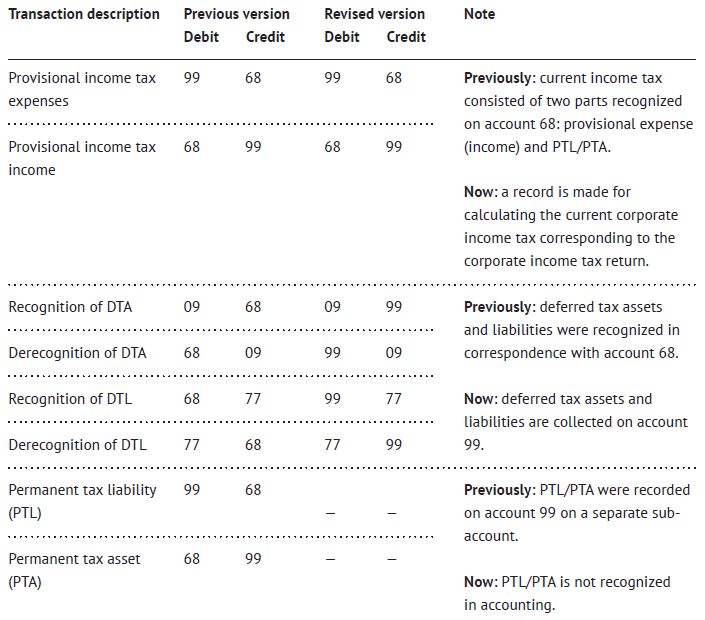

Thus, in accordance with this Recommendation the amount of income tax expense is formed on the debit of account 99 “Profit and Loss” (in case of tax income – on the credit). The specified amount includes two components: current income tax and deferred income tax. It is recommended to account for each of the components on a separate sub-account to account 99.

The amount of current income tax is recognized on the debit of account 99 “Profit and Loss” (sub-account “Current Income Tax”) in correspondence with the credit of account 68 “Calculations of Taxes and Fees” (sub-account “Calculations of Corporate Income Tax”). The specified amount is determined in accordance with requirements of the tax legislation as the amount of tax payable to the budget for the tax period corresponding to the reporting period. Such amount (in the absence of specific circumstances) corresponds to the amount of tax specified by an organization in its income tax return for the corresponding period.

The amount of deferred income tax is recognized on the debit or credit of account 99 “Profit and Loss” (sub-account “Deferred Income Tax”) in correspondence with the credit or debit of accounts 09 “Deferred Tax Assets” or 77 “Deferred Tax Liabilities” respectively.

If temporary differences change due to retrospective changes in the accounting policy or retrospective corrections of errors, the resulting changes in deferred tax assets or liabilities are recognized on the debit or credit of accounts 09 “Deferred Tax Assets” or 77 “Deferred Tax Liabilities” in correspondence with the credit or debit of account 84 “Retained Earnings (Retained Loss)” respectively.

Therefore, after the revised version of PBU 18/02 becomes effective, all corporate income tax transactions shall be collected on account 99 “Profit and Loss” for accounting purposes. Previously, deferred tax assets and liabilities were recognized in correspondence with account 68 “Calculations of Taxes and Fees”, and in order to prepare the statement of financial results amounts had to be collected from several accounts (at least for verification). Now the entire calculation of income tax is recognized on one account.

Below is the comparison of accounting records according to previous and revised rules:

The table above shows that now recognition of corporate income tax in accounting is based not on accounting data, but on data in corporate income tax returns. If previously the main account for corporate income tax accounting was account 68 “Calculations of Taxes and Fees”, now it is account 99 “Profit and Loss”. Account 68.04.2 “Calculation of Income Tax” is not used in the balance method (without recognition of permanent and temporary differences).

Summary

Therefore, starting from 2020 organizations, with the exception of those not covered by PBU 18/02 or those applying simplified accounting and reporting methods, are required to apply the new accounting rules for corporate income tax calculations.

Temporary differences now prevail in accounting, while permanent differences occur in exceptional cases.

With the new balance method accounting should become clearer, more transparent, and less tedious. However, when applying this method an accountant will have to calculate the effect on the indicators of accounting statements and, if necessary, retrospectively recalculate comparable data in the accounting statements for 2020.

Despite the obligation to apply the amendments, the revised version of PBU 18/02 does not prohibit the use of the customary cost method. The only note is that the use of the cost method is possible if the calculation of income tax using the cost method does not differ or insignificantly differs from the amount of income tax calculated using the balance method.

Correct tax accounting is a prerequisite for automatic calculation of temporary differences. Otherwise, an accountant will have to manually keep registers for calculating temporary differences.

Other Articles on Topics