CONTENTS OF LAST ISSUE

Complicated Issues in Simple Terms

Often we do not fully understand the whole complexity of tax and accounting legislation until we face it in practice.

One of such examples is the creation of reserves for vacation pay for tax purposes. Creation of reserves is already known to accounting, but the actual creation of such reserves in tax accounting causes certain difficulties.

Reserves for Vacation Pay

Provisions of the Tax Code regarding the creation of reserves for future vacation pay seem logical and clear. One shall develop an estimate for calculating the percentage of contributions to the reserve, set a reserve limit for the tax period and draw up an inventory following the tax period.

Furthermore, the procedure for the creation of the reserve for vacation pay (or at least an indication that the reserve for vacation pay is created in tax accounting pursuant to the tax legislation) shall be set in the Accounting Policy for tax purposes.

However, when it comes to the actual creation of the reserve, nothing is as simple as it seemed at first glance.

Basic data for calculation of monthly contributions and limit amount

The percentage of contributions to the reserve is determined as the ratio of the estimated amount of annual vacation pay to the estimated amount of annual labour costs.

Since the estimated amount of vacation pay is calculated, it may include not only a basic vacation, but also an additional one. If an organization plans staff expansion or indexation of wages, such factors should be considered when estimating the cost of vacation pay and labour costs.

When making estimates, it is recommended to specify the actual amount of costs for the previous year, planned increase in wages (staff expansion) and calculation of planned vacation pay in order to justify the increase in the estimated amount of labor costs and vacation pay.

Nota bene. When calculating the estimated amount of labour costs, one shall remember that labour costs include payments to freelance workers for the performance of works under civil contracts. At the same time, such persons are not entitled to any vacation, because the labour legislation does not apply to them. Therefore, when planning the amount of labour costs, there is no need to include any amounts you plan to pay to freelance workers.

The formula for percentage calculation is as follows:

The reserve limit for the tax period is usually set at the estimated amount of vacation pay or slightly higher.

Exceeding of the reserve limit

There may be situations where an actually created reserve at some point exceeds the set reserve limit for the tax period. In this case the organization stops creation of the reserve in tax accounting and recognizes actual expenses on vacation pay instead of a reserve in tax accounting.

Reserve inventory

On the last day of the tax period (December 31), the organization should draw up a reserve inventory for future vacation pay. Such inventory should include the following:

- The number of vacation days employees are entitled to as of December 31 (separately for each employee);

- Average earnings for each employee;

- Insurance premiums for each employee (based on average earnings);

The reserve amount which covers the organization’s obligations of vacation pay as of December 31 is calculated based on such data.

Unused reserve amounts as of the last day of the current tax period shall be included in the tax base of the current period. Such balance shall be included in income, in case the taxpayer considers it unreasonable to create a reserve for the next tax period.

Unused reserve amount for vacation pay as of the last day of the current tax period is the difference between reserve amounts for vacation pay accrued in the reporting period and the amount of actual expenses on payments for vacations used in the tax period (including insurance premiums) and on future payments for statutory vacations not used in the reporting year (including insurance premiums).

In other words, if after the inventory of the reserve for vacation pay as of December 31 of the reporting year it turns out that the reserve amount created exceeds the amount of vacation pay “earned” by employees as of the inventory date, the excess amount shall be recovered and recognized as taxable income.

Nota bene. If the taxpayer decides not to create a reserve for future vacation pay in the next tax period, the balance of the unused reserve shall be recovered in full on December 31 of the current tax period.

In case of insufficient funds of the actually accrued reserve confirmed by the inventory as of the last day of the tax period, the taxpayer shall include the amount of actual vacation pay in expenses as of December 31 of the year in which the reserve was accrued and, accordingly, the amount of insurance premiums for which no specified reserve has been created earlier.

Thus, if the inventory reveals that the organization’s obligations for vacation pay as of December 31 (including insurance premiums) exceed the created reserve, the organization shall create additional reserves up to the required amount.

Classification of expenses

Creation of the reserve for future vacation pay shall be recognized as expenses related to production and sales.

Creation of additional reserves following the inventory shall be reflected in expenses associated with production and sales.

Recovery of an excess reserve shall be recognized as non-operating income.

Compensation for unused vacation

In accordance with the tax legislation, expenses in the form of average earnings retained by employees for the period of vacation and compensation for unused vacation are different types of labour costs, which is confirmed by the opinion of the Ministry of Finance of the Russian Federation 1.

Having regard to the above, amounts of compensation for unused vacation paid to employees upon resignation are recognized directly as part of labour costs and do not reduce the reserve amount for future vacation pay.

Bonus Programs

Bonus programs are very common in retail. However, despite their widespread application, many people have questions about the recognition of bonuses (points) accrued to purchasers under certain conditions in tax accounting and their use.

There are different points of view, including a very controversial one, which states that bonuses (points) accrued to the purchaser are deemed taxpayer’s debt to the purchaser, which is to be recognized in accounting records. Moreover, such debt is recognized as the purchaser’s advance payment and is subject to VAT.

Such point of view is beneficial for the budget, but is incorrect in terms of accounting and logic.

There is no debt to the purchaser upon the accrual of bonuses (points), since the purchaser may only purchase goods by partially paying for them with bonuses (points), i.e. to get a discount; but the purchaser is not entitled to cash out such bonuses (points).

Having regard to the above, bonuses (points) are not reflected in tax accounting upon their accrual. Accounting of accrued bonuses is performed separately (beyond bookkeeping and tax accounting). When bonuses are used to pay for services, they are recognized in tax accounting as a discount, i.e. they reduce the sales cost.

Nota bene. The situation when 100% of the cost of goods is paid by bonuses is risky for the taxpayer. Such situation bears a high risk of gratuitous sale and, accordingly, additional VAT. In order to minimize the risk, it is recommended not to allow full payment of goods with bonuses, but to limit the size of the “bonus discount”.

Sales of Gift Certificates

Just like bonus programs, sale of gift certificates is widespread in retail. However, the word “sale” is just nominal, since a certificate is not a commodity. In addition, contrary to the popular belief, a gift certificate is not an accountable form.

An accountable form is a primary accounting document equated to a cash receipt generated in electronic form and (or) printed out using the automated system for accountable forms at the time of payment settlements between the user and the client for the services rendered, which contains data on payment settlements, confirms the fact thereof and complies with the legislation of the Russian Federation on the application of cash register equipment.

Having regard to the above, a gift certificate is not an accountable form and does not exempt the seller from issuing a receipt or an accountable form upon the receipt of payment from an individual.

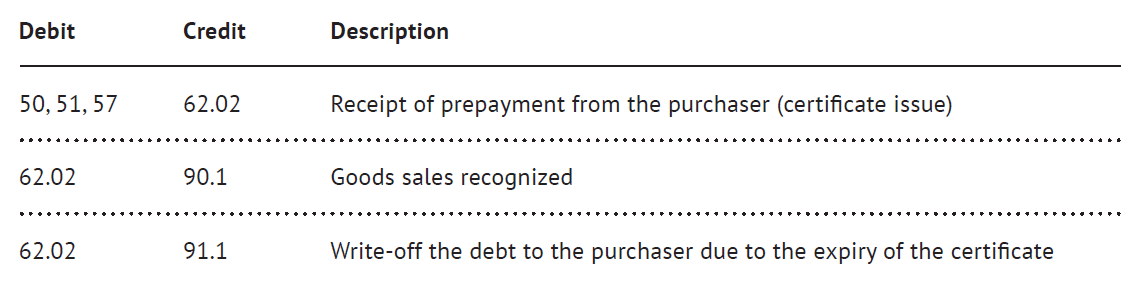

In accounting, acquisition of a certificate is recorded as a prepayment. Revenue in accounting is recognized when goods are sold.

Since the “sale” of certificates is recognized as the purchaser’s prepayment, the seller shall calculate and pay VAT on the advance to the budget.

As a rule, gift certificates have a certain validity period. In this case, when a gift certificate expires, the seller shall write off the debt and recognize non-operating income.

The following is the accounting procedure for operations with gift certificates.

- Letters of the Russian Ministry of Finance No. 03-03-06/4/29 dated 03.05.2012, Directorate of the Russian Federal Tax Service for the City of Moscow No. 16-15/054509 dated 04.06.2014.

Other Articles on Topics