CONTENTS OF LAST ISSUE

Business relocation to Cyprus. Overview of taxes and payroll contributions

Recent changes to double tax treaties (DTTs) and a number of new sanctions imposed on Russia in 2022 have limited the ability to run and develop business internationally. In this regard, the number of entrepreneurs who want to relocate their business and staff to another country has increased dramatically. In this article, we will use practical examples to review and calculate taxes and payroll contributions of an employee employed in a Cyprus company, taking into account and analyzing the latest changes in legislation and concessions.

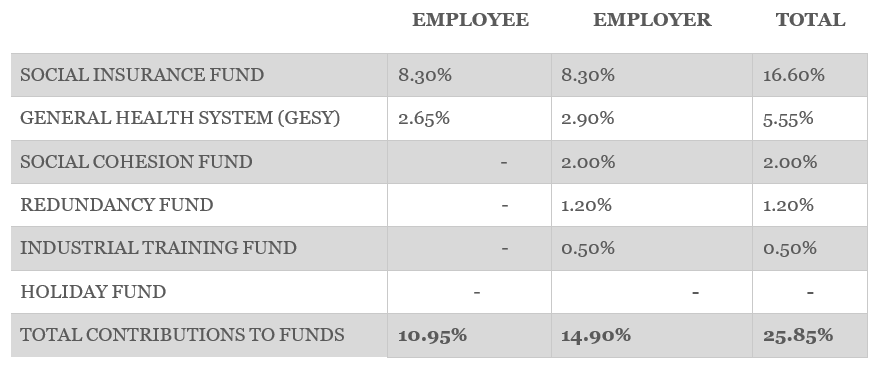

1. SOCIAL INSURANCE AND OTHER CONTRIBUTIONS

Contributions to funds are a requirement for both the employee and the business. The calculation of social insurance and other payroll contributions is based on the total amount of the employee’s labor remuneration. The table below shows the distribution of burden between the employer and the employee.

- Social Insurance Fund – every employee in Cyprus should be insured under the social security system. The limit of labour remuneration for contributions to the social insurance fund is EUR 58,080 per year or EUR 4,840 per month.

- General Health System (GESY) – obligations to pay contributions apply regardless of whether the individual resides in Cyprus. Individuals who are not tax resident in Cyprus are required to pay contributions at the applicable rates on income received from sources in Cyprus. Deductions should be made from the amount of total income not exceeding EUR 180,000 per year. Cyprus tax residents are also required to pay to GESY on income other than labour remuneration, such as dividends or rental income.

- Social Cohesion Fund – contributions to the Social Cohesion Fund are calculated on the entire amount of labour remuneration and have no maximum limit.

- Redundancy Fund – the amount of contributions is limited by the maximum level of labour remuneration, as is the case with social insurance contributions

- Industrial Training Fund

- Holiday Fund – the employer needs not pay contributions to the holiday fund if an exemption is obtained. The application for exemption in the YKA 1-005 Application of the Employer for Exemption from the Obligation of Payment of Contributions shall be submitted by the employer

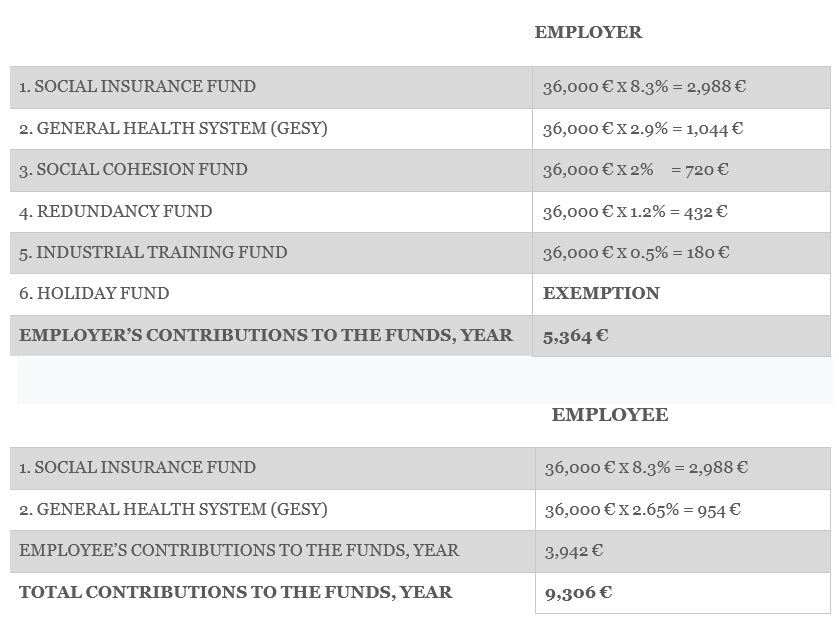

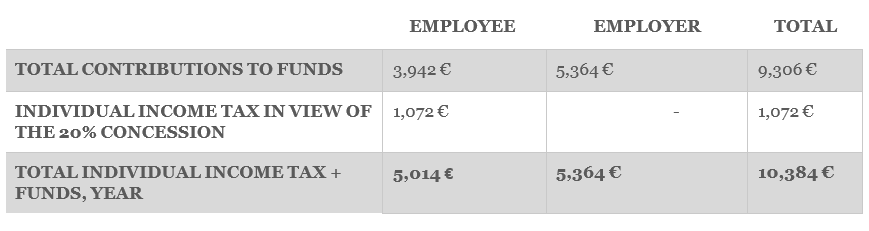

Let us calculate the amounts of contributions to social insurance funds using the example of an employee hired under an employment contract in a Cyprus company with a gross salary of EUR 3,000 per month (EUR 36,000 per year).

The calculation shows that the total amount of contributions to all funds for an employee with a salary of EUR 3,000 per month (EUR 36,000 per year) will be EUR 776 per month (or EUR 9,306 per year). From this amount, EUR 329 per month (EUR 3,942 per year) will be deducted from the employee’s salary and EUR 447 (EUR 5,364 per year) per month will be paid by the employer.

The employer shall pay contributions to the funds for the company and for the employee before the end of the month following the reporting month.

From 13 September 2021, when hiring an employee, the employer is required to submit a notice of employment electronically through the ERGANI information system in addition to registering with the social insurance funds.

If a company hires a foreign employee, the following requirements are imposed on them: a minimum gross salary of EUR 2,500 per month, a diploma of higher education or professional experience in similar positions for at least 2 years, an employment contract for a period of 2 years.

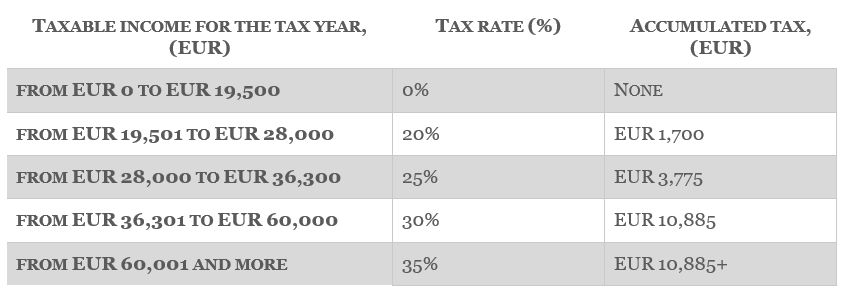

2. INDIVIDUAL INCOME TAX

Income of individuals in Cyprus is subject to progressive taxation:

Tax base for calculating individual income tax = salary under an employment contract – contributions to funds (only the employee’s share, i.e. 10.95%).

Let us calculate individual income tax using the same example. Gross salary of the employee: EUR 3,000 per month or EUR 36,000 per year.

Tax base: 36,000 – 2,988 (Social Insurance) – 954 (GESY) = EUR 32,058 per year,

Calculating individual income tax: 19,500 x 0% + 8,500 x 20% + 4,058 x 25% = EUR 2,715 per year

The employer shall pay individual income tax for the employee in equal monthly installments during the year (in our example, EUR 226 per month) until the end of the month following the reporting month.

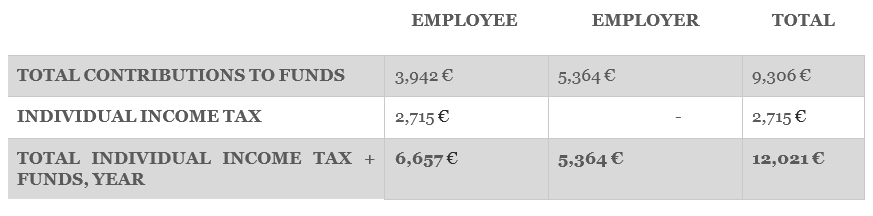

Let us review the results in the table below (the calculation does not include concessions, which will be discussed in the next chapter). The tax burden on individual income tax and contributions to funds is:

Thus, the employee will receive 36,000 – 3,942 – 2,715 = EUR 29,343 per year or EUR 2,445 per month (excluding concessions).

3. TAX CONCESSIONS

Let us consider tax concessions applicable to the labor activities of individuals who are employed for the first time in a Cyprus company (who moved to Cyprus or work remotely under an employment contract). To attract highly qualified professionals to their country, the Ministry of Finance of Cyprus provides incentives in the form of exempting part of the income from individual income tax; the following concessions do not apply to other taxes and duties.

The following is not subject to individual income tax:

a) 20% of labour remuneration (up to a maximum of EUR 8,550 per year) of an individual who was not a tax resident in Cyprus before the start of their labour activities. For those employed, from 26 July 2022, the tax concession will be available for 7 years (previously, the exemption was granted for a period of 5 years). This concession may be applied starting from the tax year following the year of employment.

Let us calculate the tax using the 20% concession (the concession is applied to the gross salary amount):

Tax base: (36,000 – 20% (concession on individual income tax)) – 2,988 – 954 = EUR 24,858 per year

Calculating individual income tax: 19,500 х 0% + 5,358 х 20% = EUR 1,072 per year (or EUR 89 per month)

The employee saves 2,715 -1,072 = EUR 1,643 per year or EUR 137 per month on individual income tax. After applying the concessions, the employee receives 36,000 – 3,942 – 1,072 = EUR 30,986 per year or EUR 2,582 per month.

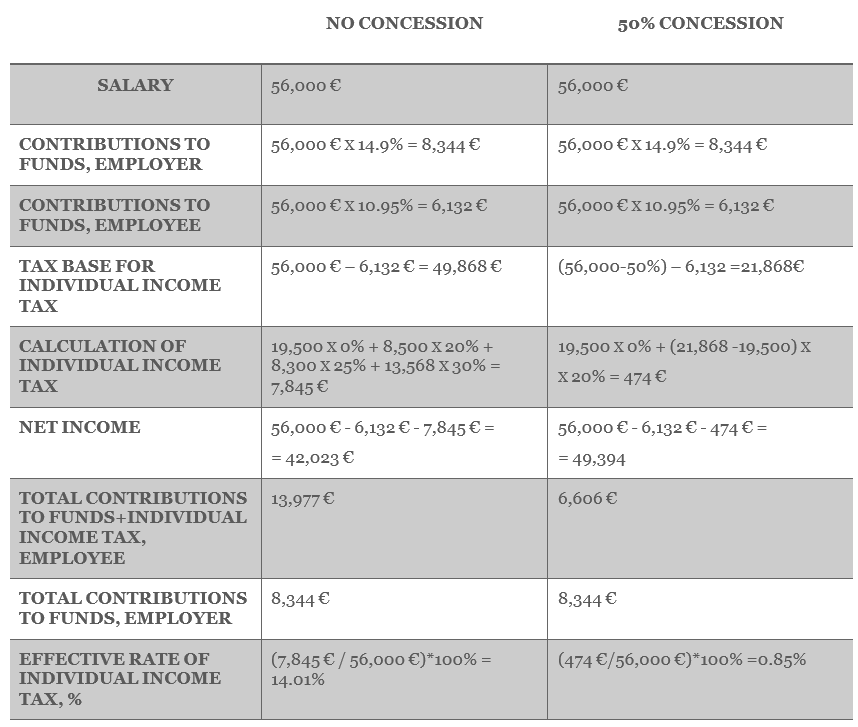

b) 50% of the employee’s labour remuneration whose first work in Cyprus began on 1 January 2022 is exempt from income tax for 17 years, provided that the annual remuneration before all taxes exceeds EUR 55,000, and the employees have not been residents of the country for 10 years immediately prior to starting work in Cyprus. Persons whose employment began before 1 January 2022 can also apply for a new 50% exemption as early as this year if the annual remuneration exceeds EUR 55,000.

The 20% and 50% concessions are mutually exclusive, only one of them can be applied by a specific taxpayer. If one already enjoys a 20% concession, they can upgrade to 50% if they meet all the criteria.

Let us calculate the savings on individual income tax from the salary of EUR 56,000 per year (EUR 4,667 per month) before and after applying the concession. Comparative analysis is presented in the table below.

As seen from the calculation above, the effective individual income tax rate with the application of the 50% concession on the salary of EUR 56,000 per year will be 0.85% (less than 1%!). By comparison, in Russia the individual income tax rate remained at 13% with the recent introduction of a progressive scale that increases it to 15%. And if your employees work remotely for a Russian company and are tax residents of other countries, the rate is 30%.

Other Articles on Topics