CONTENTS OF LAST ISSUE

Amendments to double taxation conventions. Old games, new rules

Nowadays we all live in a state of constant uncertainty, which is why it is more important than ever to separate rumors from facts, panic attacks from strategic planning, and treat everything we hear and see with a critical eye. Each time faced with a new bit of news one should ask oneself simple questions:

- What has happened/what has changed?

- How will this affect me/my business?

- When will changes take place?

- What has to be done before changes take effect?

Thus, what happened at the end of March in the field of international taxation?

On March 25, 2020, the President of the Russian Federation gave instructions to the Government of the Russian Federation to make a list of countries and consequently of double taxation conventions (DTC), and to ensure making amendments providing for the withholding tax at the rate of 15% on dividends and interest paid to tax non-residents of the Russian Federation. If no convention is reached with the contracting jurisdiction, the current convention shall be terminated.

On March 26, 2020, the Government gave instructions to the Ministry of Finance to review conventions within one month. On the same day, the Ministry of Finance issued an information notice specifying that amendments shall only affect transit jurisdictions, particularly Cyprus.

Currently, letters on amendments to conventions have been sent to the following jurisdictions:

- Cyprus

- Luxembourg

- Malta

It is also highly likely that the said instruction will affect the following jurisdictions:

- the Netherlands

- Switzerland

- Ireland

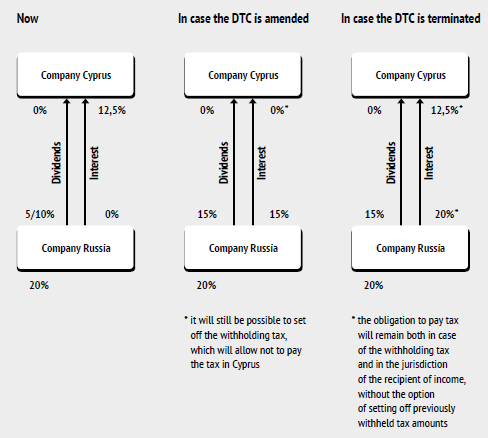

The diagrams below present compared effects:

As is seen from the diagrams above, in jurisdictions where dividends are exempt from taxation the difference in the tax burden for dividends is not significant. However, in terms of interest income the difference is much more significant, especially in case of the DTC termination.

Despite the fact that no amendments are planned to be made to the DTC terms regarding royalties, there is still a possibility of the DTC termination, and in this case instead of the reduced rate at the source of payment and the set-off option, the taxpayer will have to pay the withholding tax at the rate of 20% with no set-off option.

Moreover, one of the consequences of the DTC termination will be the absence of necessity to confirm an actual recipient of income.

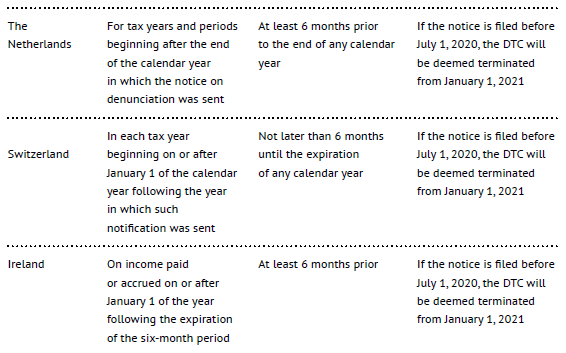

The next logical question is when the agreement may be terminated.

Therefore, if a written notice of the DTC termination with the Russian Federation is filed, changes will affect taxpayers on or after January 1, 2021. And in case of most jurisdictions, the Russian Federation should send such notifications by July 1, 2020, otherwise the conventions will be considered terminated only from January 1, 2022.

In view of the above, businesses have time until the end of the year to maneuver. However, while maneuvering in this transition period one should stay reasonable and consistent, because for example a sharp increase in interest on loans, especially retrospectively, is sure to attract the attention of the tax authorities that will require an economic justification for changing the terms of the loan agreement. In case of dividends, it should be noted that dividends may only be paid from the company’s profit, i.e. losses make the payment of dividends unreasonable.

At the same time, each case of restructuring is individual and there is no one multi-purpose solution, since both the structure of the holding and the goals pursued and their priority viewed by the owners are different.

With that in mind, before fleeing to other jurisdictions that have not yet come to the attention of the Ministry of Finance, it is necessary to pay more attention to the current situation, to assess not only risks and costs, but also the potential and growth points that may still have remained unnoticed in already familiar jurisdictions.

Other Articles on Topics