CONTENTS OF LAST ISSUE

Supporting measures for accountants in lockdown

At the beginning of April, a lot was changed to support businesses during difficult times.

This article covers the most significant changes related to those economic areas that are not recognized as particularly affected, as well as some measures to support small and medium-sized businesses operating in the affected economic areas.

Accountants may take a break

Due to introduction of non-working days in April and early May for all organizations, dates for submission of reports and payment of taxes, fees and insurance premiums were postponed1.

Reports that in accordance with the Tax Code of the Russian Federation are to be submitted in March–May 2020, now may be submitted 3 months later. This applies to:

- Tax returns (excluding value added tax returns);

- Tax calculations of the amounts of income paid to foreign organizations and withheld taxes;

- Calculations of the personal income tax charged and withheld by tax agents;

- Calculations of advance payments;

- Accounting (financial) statements.

The VAT return and Calculation of insurance premiums for the 1st quarter of 2020 shall be submitted to the tax authority by May 15, 2020.

On 7 April, the Ministry of Finance and the Federal Tax Service issued explanations2 stating that accounting statements for 2019 (if such accounting statements are not regulated by special provisions, e.g. on state secrets) shall be submitted to the tax authority on the first business day after the date set by the Tax Code of the Russian Federation, i.e. May 6, 2020. However, after the statement of the President of the Russian Federation and the announcement of May 6-8, 2020 as non-working days, dates for submission are automatically postponed to May 12, 2020.

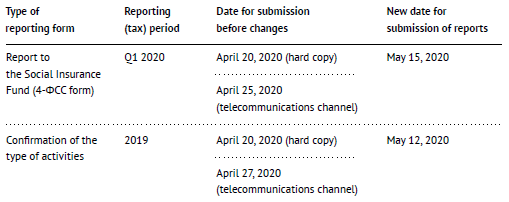

For convenience, a comparative table is made covering principal forms of accounting and tax statements.

Dates for submission of reports to the Social Insurance Fund have also been changed:

Postponement of dates for submission of reports entails no extension of tax payment deadlines (advance payments on taxes), including in cases when in accordance with the Tax Code of the Russian Federation the deadline for the tax payment (advance payment on tax) is set no later than the date of submission of the tax return (calculations).The Pension Fund turned out to be the least favorably disposed to payers of insurance premiums and did not postpone the dates for submission after the announcement of April as a non-working month. The Pension Fund requires to submit the СЗВ-М and СЗВ-ТД reports monthly no later than on the 15th day of the month following the reporting one. If the specified period is violated, the payer of insurance premiums and the manager shall be fined.

Therefore, the following logical conflict arises: one is allowed to submit reports later, but most organizations still have to pay tax in due time. Fines for late payments will not be charged and accounts will not be blocked, but the accrual of penalties for late payments is not cancelled.

Contributions to the Pension Fund have become smaller, but not for everyone

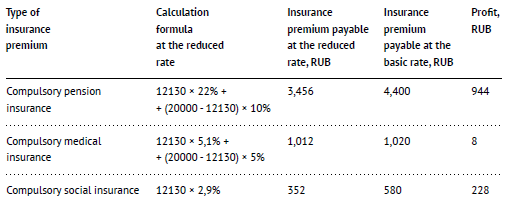

From April 1, 2020 to December 31, 2020, payers of insurance premiums recognized as small and medium-sized businesses apply the following rates of insurance premiums for the labour remuneration of their employees (for the part of remuneration that exceeds the minimum wage amount)3:

For clarity, here is an example demonstrating the calculation of insurance premiums for April (due in May 2020).Moreover, the Tax Code of the Russian Federation has been amended to extend these rates for 2021 and the following years4, i.e. such rates shall be effective until their further amendment.

Example.

The employee’s wages for April 2020 amounted to 20,000 rubles. The minimum wage amount set by the federal law5 is 12,130 rubles.

Such measures are aimed at achieving two objectives at once:In other words, the profit really amounts to 15%, but reduced rates are applied to the employee’s wages that exceed the minimum wage amount, and not to the whole amount. However, the reduction is significant (twofold), especially for those employers who pay high wages to their employees.

- Reduction of the tax burden on small and medium-sized businesses;

- Additional incentive to “increase” wages of employees.

Part of wages from the budget funds

The Government of the Russian Federation has approved rules6 on granting subsidies for partial compensation of expenses, including for the remuneration of their employees in April and May 2020, to organizations that carry out activities recognized as particularly affected by the spread of the new virus.

The amount of a subsidy is the minimum wage amount as of January 1, 2020, or 12,130 rubles.

A subsidy is granted to those organizations and entrepreneurs that as of March 1, 2020 carried out their principal activities in the affected economic areas. The tax authority draws up a register of organizations applying for subsidies. The following conditions should be met in order to be included in the registry:

- Organization or entrepreneur should be listed in the registry of SMEs as of March 1, 2020;

- The subsidy recipient should not be in the process of liquidation, no bankruptcy procedure should be initiated against it, no resolution on the future exclusion from the Unified Register of Legal Entities shall be adopted;

- As of March 1, 2020, there is no arrears on taxes and insurance premiums totaling more than 3000 rubles;

- The number of employees of the subsidy recipient in the month for which the subsidy is paid is at least 90% of the number of employees in March 2020.

To receive a subsidy, an organization should file an application to the tax authority via the telecommunications channel, their personal account, or by post.

To receive a subsidy for April 2020, an organization shall file an application to the tax authority during the period from May 1 to June 1, 2020, and to receive a subsidy for May 2020 – from June 1 to July 1, 2020.

If there are no grounds for refusal to grant a subsidy, the tax authority shall calculate the amount of the subsidy within 3 business days from the date of filing an application, but not earlier than the 18th day of the month following the month for which the subsidy is granted, draw up a register and send it to the Federal Treasury.

The Federal Treasury transfers the subsidy within 3 business days from the day following the day when the Federal Treasury receives the register.

There is always a fly in the ointment

After the President’s statement, amendments to the Tax Code of the Russian Federation included an amendment7 on the introduction of a new item taxable with the personal income tax.

From January 1, 2021, interest on all deposits (account balances) with banks in the Russian Federation is subject to personal income tax at the rate of 13%.

Therefore, now even very modest amounts of interest on deposits shall be taxed. However, there is no rush to withdraw funds from one’s accounts before the end of 2020, as:

- Interest income for 2020 is not subject to taxation;

- The tax base is defined as the excess of the income amount in the form of interest received by the taxpayer during the tax period on all deposits (account balances) with these banks over the amount of interest calculated as the product of one million rubles and the key rate of the Central Bank of the Russian Federation effective on the first day of the tax period;

- Income in the form of interest received on deposits (account balances) in rubles, the interest rate whereon during the entire tax period does not exceed 1 percent per annum, is not subject to taxation;

- Income on escrow accounts is not subject to taxation.

Therefore, if to take the current key rate (5.5%) as a basis, then under the general rule the amount of interest received by the taxpayer for the year less 55,000 rubles shall be subject to taxation.

If income on deposits is denominated in foreign currency, such income shall be converted into rubles at the official exchange rate of the Central Bank of the Russian Federation set on the date of the actual receipt of income (receipt of funds).

Individuals will not have to submit reports on the interest received. The tax shall be paid no later than December 1 of the year following the expired tax period (calendar year) on the basis of a tax notification sent by the tax authority on tax payment. Banks shall provide information about income of individuals (their clients).

- Clause 3 of Regulation of the Government of the Russian Federation No. 409 dated 02.04.2020.

- Letter of the Ministry of Finance and the Federal Tax Service No. 07-04-07/27289 dated 07.04.2020.

- Article 6 of Federal Law No. 102-ФЗ dated 01.04.2020.

- Sub-Clause 9 of Article 2 of Federal Law No. 102-ФЗ dated 01.04.2020.

- Federal Law No. 463-ФЗ dated 27.12.2019 “On making amendments to Article 1 of the Federal Law “On the minimum wage amount”.

- Resolution of the Government of the Russian Federation No. 576 dated 24.04.2020.

- Article 2 of Federal Law No. 102-ФЗ dated 01.04.2020.

Other Articles on Topics