CONTENTS OF LAST ISSUE

Bitcoin: revolution of currency system or new way to take money from people

Development of information technology in recent years has attained such speeds, that human possibilities will not be able to keep up with it soon. Frankly speaking, this situation has already been witnessed in some spheres of public life. For example, newly formed Internet community has gone beyond the limits of formal legal regulation of its activity. So, there is extraterritoriality formation outside certain state borders, which establish its laws, its history, culture and religion and which introduced its own currency.

Now virtual currency, circulating in the Internet space, constitutes software package, which is called “Bitcoin”, originating from combination of English words “bit” – unit of information, and “coin”). As there is no analogue of this system, launched in 2009, in the online space, for the purpose of the context, the word “Bitcoin”, “cryptocurrency” and “virtual currency” will be used as synonyms, although it is the same. Frankly speaking, the relationship between such concepts is similar to the relationship between concepts “currency”, “bank-note” and “dollar” in the real world.

Cryptocurrency exists in cyberspace as a secure decentralized system, which is based on a single network protocol and use of distributed computations. In other words, there is no single issuer of Bitcoin. The activity is performed by users depending on their computation capacity.

If we imagine the operation of bitcoin system, then the most striking example will be the game that was popular among children in the last decades of the twentieth century – sotkas or dibs. At that time, paper or plastic circles were sold in stores, called sotkas, or dibs. Child bought those dibs and went into the yard, where he joined a simple game, placing his stakes on dibs belonging to him. The winner took won dibs. As a result, the child was able to increase the number of dibs by winning, spending or losing them. Dibs were used not only directly for the game purposes, but also as a means of payment. For example, fifteen dibs could be exchanged for throwing stick, and if you had thirty dibs, you could make a more serious offer.

Although the aforesaid children’s game seems primitive, it clearly explains the essence of Bitcoin. As well as manufacturer of dibs, person, acting in the Internet space, announces the issuance of equivalent of money or securities (actually – issues its own quasi-currency). Seller sells dibs, and the market represented by playing children, establishes the principle of the formation of its price. The user gets pseudo-currency paying therefor with official currency. Besides, user gets a chance to use it for performing any operation at his risk. In particular, such currency enables the user to make payment for goods, works and services, to accumulate it, purchase and sell it at online currency exchanges, the largest of which until March 2014 included «BTC-E» and «Mt.Gox» (the detailed analysis will be provided below).

Bitcoin exchange rate is determined by fluctuations of demand and offer with regard to cryptocurrency. Its independence from dollar, euro or any other real currency – is one of the basic principles of formation of exchange rate.

In addition, one of the ways to maintain and regulate the Bitcoin exchange rate is strict restriction of its issuance. The right to issue Bitcoin may be exercised by interested persons, and by any user of Internet having necessary computing capacity. The number of Bitcoins produced by each user and the period during which the issuance should be carried out is strictly limited. Restriction of issuance of bitcoins is the only administrative regulator of cryptocurrency exchange rate.

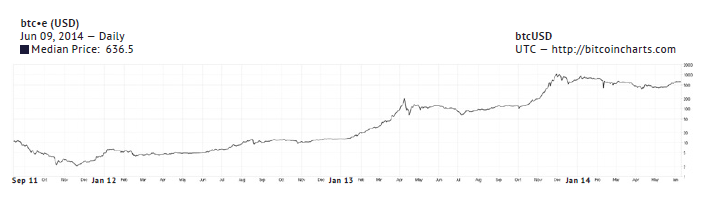

Initially Bitcoin was officially released on 25.04.2010. At that time the declared value of cryptocurrency was 0.3 U.S. dollars per 1 Bitcoin. One of the main indicators of cryptocurrency exchange rate fluctuations was the largest electronic stock exchange «Mt.Gox». By June 2011 Bitcoin exchange rate reached 29.57 U.S. dollars, however, on 19.06.2011 «Mt.Gox» stated that security system had been hacked, that, in turn, resulted in sharp drop in cryptocurrency exchange rate. Further, after some series of ups and downs, by the end of 2013 Bitcoin exchange rate reached a historic maximum of over 1,000 U.S. dollars per 1 Bitcoin. 21.02.2014 «Mt.Gox» again was hacked, and in March filed for bankruptcy. This circumstance had the most negative impact on exchange rate of bitcoin, which propped below U.S. $ 100.

The chart contains bitcoin exchange rate fluctuations pursuant to data of current exchange «BTC-E» for the period of its operation1:

Unlike conventional units, which allow to purchase services or goods on websites (for example, “coins” in network computer games or “votes” and “Oks” in social networks), Bitcoin as quasi-currency is universally recognized currency of Internet space. Its principles of the issuance and exchange rate fluctuations are strictly regulated. It is universal means of payment, the only condition for application of which is the consent of both parties – the payer and the payee – to making payment using cryptocurrency.

Despite all advantages of making payments using Bitcoin, such as high-speed of operations, absence of specified payment intervals (banking day), account management cost efficiency and absence of service fees (in most case the fees are not charged at all), Bitcoin users incur significant risks. First, it is connected with cryptocurrency price formation. If we talk about the fact that its price is determined solely on the basis of offer and demand as opposed to any objective economic factors, there is every indication of the structure similar to infamous financial pyramids, such as «The Securities and Exchange Company» created in pre-war America by Charles Ponzi and «Madoff Investment Securities» created by Bernard Madoff, which collapsed in 2008 and landmark companies “Vlastilina” and “MMM” of post-Soviet Russia.

The fact, that characteristics of Bitcoin are close to those of financial pyramids, is not denied by its developers. The only but very significant difference is that due to decentralization of cryptocurrency system there is no formation of “pyramid” as well as formation of group of users who receive most part of profit. Chances of receiving abnormal profit and risks incurred by users are equal irrespective of time of logging into system2.

Second, and even more important taking into account that operations using bitcoins are characterized by high risk – cryptocurrency market is not regulated by provisions of positive law. For example, in China settlements using Bitcoin are officially banned.

In Russia cryptocurrency market is actually “not regulated by the law”. So far there hasn’t been enacted any regulation that somehow determines legal nature of this tool. Official position regarding virtual currencies was expressed only by the Bank of Russia on 01.27.2014. It issued an information letter “On use of “virtual currency”, in particular, Bitcoin when executing transactions”. The letter expresses concern over unsecured status of virtual currencies and legally bound entities, whereas operations involving Bitcoins are speculative and bear high risk of loss of value. In addition, the Central Bank noted that the laws of the Russian Federation prohibit the issuance in the territory of the Russian Federation of such cash equivalents3.

The Bank of Russia shall be praised for addressing the emergence of Bitcoin. At the same time the recommendation relating to prohibition of issuance of pseudo-currency is based on a broad interpretation of the law, in other words its application to legal relationship arising outside the territory of Russia. Cryptocurrency nature does not allow to determine the location or place of business of issuer thereof (as you remember, Bitcoin is a peer to peer network, that is completely decentralized, and for maintenance of its performance network computing method is used), and therefore it is impossible to conclude which jurisdiction shall apply for legal regulation of its issuance.

The only instrument of payment on the territory of Russian Federation is ruble4. As far as settlements using cryptocurrency between Russian entities are concerned, such settlements shall not be treated as violating the law. However, in such case, the problem is to identify the fact of the offense: the legislation sets forth prohibition with regard to currency transaction performed by residents of the Russian Federation, but the concept of currency transaction covers only those operations that are performed through Russian and foreign currencies, as well as domestic and foreign securities5. Cryptocurrency, in turn, can not be attributed to any of the aforesaid currency transactions tools. Therefore, Bitcoin transactions can not be treated as currency transactions; therefore, execution thereof may not be deemed violation of currency regulations. Other possibilities for qualifying cryptocurrency transactions are not available. In other words, Bitcoin may not be treated as means of payment (both lawful and unlawful), while cryptocurrency may not be regarded as fraudulent purpose transaction.

So now we have faced a situation where there is a currency system, the use of which is not regulated and can not be regulated by the laws of any jurisdiction. And bridging legal gap by prohibiting settlements using Bitcoin, as it was made in China at the end of the last year, seems irrational, since the appearance of Bitcoin is a consequence of natural development of Internet technologies and network community. So far we can only guess which path Russian legislator will take, but it is obvious that disregard of existence of virtual currency will soon become impossible. At the moment we envisage several developments of scenarios:

- Simple legislative prohibition of cryptocurrency stipulated by national laws. We have already discussed that option, and explained why it seems the least appropriate.

- Introduction of concept of virtual currency into the laws of the Russian Federation relating to currency regulation and currency control as a type of currency valuables or as independent object of currency regulation. So far it seems doubtful, as there is no official issuer of cryptocurrency, that is generally contrary to universally accepted understanding of the currency in general. It is possible that this option would be the most simple and appropriate for implementation, and its execution will not require full audit of laws for the Russian laws.

- Discussion and development of principles of legal regulation of relationship connected with issuance and settlements using virtual currency on international level, for example through influential international organization, such as, for example, the Organization for Economic Cooperation and Development (OECD). In future such principles would be able to integrate into their legal systems any jurisdictions which are already members of OECD or support its ideas.

Between first issue of cryptocurrency and reaction thereto of Russian authorities almost 4 years have passed. The options described above will remain our assumptions, and in addressing the question whether it is reasonable to facilitate settlements using Bitcoin, whether to save own money in such currency and whether to try to make some gains thereof with the help of virtual exchanges, each user can only rely on his own experience and intuition. It is impossible to imagine when this situation will change and when Russian legislator will either completely prohibit high-risk transactions with bitcoins, or will provide adequate legal regulation of their enforcement.

- Pursuant to the data of the website bitcoincharts.com / charts / btceUSD # tgMzm1g10zm2g25zl.

- More information you can find on website bitcoin.org/ru/.

- The Bank of Russia makes reference to article 27 of the Federal Law №86-FZ as of 10.07.2002 “On Central Bank of of the Russian Federation (Bank of Russia)”.

- Article 140 of Civil Code of the Russian Federation.

- Articles 1, 9 of Federal Law № 173-FZ as of 10.12.2003 “On Currency Regulation and Currency Control”.

Other Articles on Topics