CONTENTS OF LAST ISSUE

What the Past Year Left: Tax Legislation Amendments

When there are disasters around such as law on controlled foreign companies, it is difficult to get distracted and to pay attention to anything else relating to taxes. However, the Tax Code sheds its editions like leaves and, whether we like it or not, we shall follow this process in order to not be trapped. The past year was rich in innovations: in this article we will try to outline the most important of them.

- From 1 January 2015 the list of cases when the tax authority may demand documents from the taxpayer in the course of the desk audit is extended. Now the inspectorate has the right to check invoices, primary and other documents relating to transactions reflected in the VAT return, if it found:

- Differences in the data on transactions contained in the VAT return;

- Inconsistencies between the data on transactions contained in the VAT return submitted by the taxpayer and the data on the same transactions submitted by another taxpayer;

- Inconsistencies between the data on transactions contained in the VAT return submitted by the taxpayer and the data on the same transactions reflected in the ledger of invoices received and issued.

The demand of invoices and primary documents is legal provided the identified differences evidence understatement of the amount of VAT payable or overstatement of the amount of tax recoverable.

Inspection of areas, rooms of the taxpayer that previously could be made as part of the field tax audit only, now is possible in the course of the desk audit as well. The grounds for the inspection can be:

- The above differences in the VAT return, which evidence understatement of the amount of VAT payable or overstatement of the amount of tax recoverable;

- The VAT return with the tax amount stated as recoverable.

Thus, if you state VAT as recoverable in 2015, wait for uninvited guests.

- Since the beginning of the new year the VAT return to be submitted electronically, but was submitted on paper, is not deemed submitted1. I.e. even if the terms of submission of returns are met, but the requirement related to its form is not complied with, the taxpayer may be held accountable for failing to submit tax returns. The new rules also apply to the specified tax returns submitted from 1 January 2015 for the past periods.

VAT payers are no more obliged to maintain ledgers of invoices received and issued2. This innovation is designed to reduce excessive paperwork, since the information specified in ledgers is duplicated in the purchase ledger and sales ledger. As a consequence, the copy of the ledger of invoices received and issued is excluded from the list of documents confirming the right to be released from the obligations of VAT payer3.

In 2014, the ledger of invoices received and issued had to be maintained by entities that were not VAT payers, in the case of issue or receipt by them of invoices in carrying out activity for the benefit of another entity on the basis of engagement agreements, commission agreements or agency agreements4. From 1 January 2015, this obligation applies to entities receiving or issuing invoices as part of implementation of freight forwarding agreements or while performing the function of builder. This rule now applies both to taxpayers that are exempt from the obligation to pay VAT and to entities that are not VAT payers.

- From the beginning of the new year, the interests on the debt obligations of any kind are recognized income (expense) from the profits tax based on the actual rate5. For transactions recognized controlled ones, one of the parties in which is the bank, the new edition of the Tax Code established a limit on the amount of interests that can be taken into account for the calculation of tax. For example, as for the debt obligation in rubles the limits of interest rates ranges from 75 to 180% of the refinancing rate of the Bank of Russia (for the period from 1 January to 31 December 2015), from 75 to 125% (from 1 January 2016). If these requirements are not met, the income (expense) is recognized the interest calculated based on the actual rate taking into account the transfer pricing rules.

- From 1 January 2015 the concept of sum difference and the special procedure of its accounting are excluded. Now the fluctuation in the value of claims denominated in foreign currency, but payable in rubles due to change in foreign currency exchange is recognized difference in exchange rate6. The sum differences arising in transactions entered into before 1 January 2015 are accounted for tax purposes in the same order. The new accounting rules apply to the sum differences that arise in transactions concluded since the beginning of the new year. These rules apply if the additional evaluation or the devaluation of property is made in connection with one of the following events:

- Change in the official exchange rate established by the Bank of Russia;

- Change in the foreign currency exchange rate against the ruble established by law or by agreement of the parties, provided that the value of the claims (liabilities) denominated in this currency that are payable in rubles is determined according to the rate established by law or by agreement of the parties, respectively.

The procedure for recognition of foreign exchange differences income and expenses remained virtually unchanged. However, now the claims (liabilities), the value of which is denominated in foreign currency, are translated into rubles according to the official exchange rate established by the Bank of Russia, for the last day of the current month, and not for the last day of the reporting (tax) period, as previously7. The exchange rate differences in the previous edition of the Tax Code were recognized income and expenses for the last day of the current month as well8. In this regard the tax accounting rules have become uniform.

- From 24 June 2014 the Tax Code provides binds the depositary, trustee and Russian organizations to withhold tax on profit on dividends payable not only to foreign, but to Russian companies as well9. At first glance, it seems strange that the law establishing new obligations for taxpayer (tax agent), entered into force in the middle of the tax period10. This measure was taken due to the uncertainty appeared since the beginning of 2014 regarding the functions of the aforementioned persons as tax agents. Under the previous edition of the Tax Code, they were recognized tax agents only upon payment of dividends to a foreign organization. Since, in accordance with the amendments to the Federal Law “On the Securities Market”, which entered into force on 1 January 2014, the depositary is not obliged to disclose to the issuer the information on shareholders, the issuer has no information about what is the recipient of income in the form of dividends on the shares – a Russian or a foreign organization. Consequently, the issuer can not be recognized a source of income in the form of dividends for a Russian organization. In its Letter the Russian Ministry of Finance pointed out that from 1 January 2014 the depositary, where custody accounts of holders – Russian organizations are opened, is a source of income for such organizations and, therefore, is recognized a tax agent in such payments11.

In the first half of the year 2014 the depositary’s obligations to withhold tax on dividends payable to foreign organizations were provided for only by the said by-law. The old version of the Tax Code was applicable. Therefore, the organizations, which failed to perform the obligations of tax agent in the payment of dividends to Russian organizations in 2014, are exempt from the liability by the Federal Law that brought the appropriate amendments12. The Russian organizations that actually received in 2014 income in the form of dividends on shares on which the tax agent did not withhold the tax, are obliged to independently calculate and pay the profits tax prior to 28 March 201513.

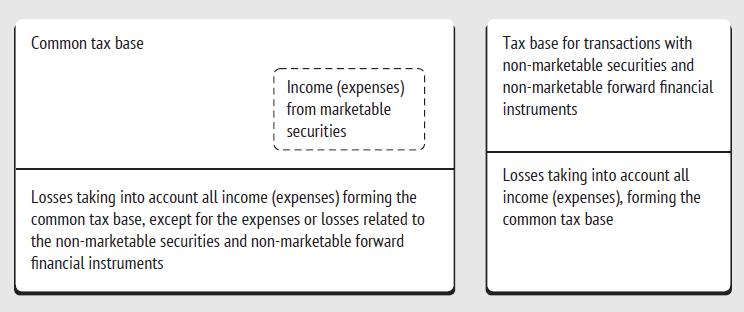

- From 1 January 2014 the provisions of the Federal Law of 28 December 2013 No. 420-FZ, under which the income (expenses) from transactions with marketable securities shall be accounted under the common procedure in the common tax base came into force. The common tax base means the tax base for the profit taxable at the rate of 20%14. According to such tax base no procedure for accounting of profit and losses different from the common procedure is provided for – previously taxpayers, except for professional participants of the securities market, had to determine it individually. Apart from the common tax base, the tax base is determined given the total transactions with non-marketable securities and non-marketable forward financial instruments15.

Previously, according to the legislation the taxpayer had to define individually in its accounting policy the types of securities (marketable or non-marketable securities on an organized market) in transactions with which, upon the formation of the tax base the income and expenses include other income and expenses in transactions with securities16. I.e. the tax base for such transactions could be reduced only by the related expenses, such as broker fees. Now the losses, calculated taking into account all income (expenses) of the taxpayer, may be aimed at reducing the tax base (profit) for transactions with non-marketable securities and non-marketable forward financial instruments17. However, the losses from transactions with non-marketable securities and non-marketable forward financial instruments can not reduce the income from transactions with marketable securities18. Thus, the mechanism for determination of the tax base for transactions with securities from 1 January 2015 is as follows:

The losses on completed transactions arisen prior to 31 December 2014 inclusive, and previously not taken into account in the determination of the tax base, reduce the common tax base of the tax periods since 1 January 2015, but not more than 20% of the original amount of such losses as of 31 December 2014 annually until 1 January 202519. A similar rule is established in respect of the losses from the transactions with non-marketable securities and non-marketable forward financial instruments.

- According to the common rule the organizations applying the simplified taxation system are exempt from property tax20. From 1 January 2015 this exemption does not cover the real estate, in respect of which the corporate property tax base is defined as cadastral value. Such real estate includes:

- administrative and business centers, shopping centers and facilities in them;

- non-residential facilities, the purpose of which is accommodation of offices, retail facilities, catering facilities and household services (or which actually are used for these purposes);

- real estate of foreign organizations that do not operate in the Russian Federation through a permanent establishment21.

In 2014, the tax base for the corporate property tax was already determined as cadastral value of the real estate applicable to the taxpayers operating under the common taxation system in those regions of the RF where the relevant law was adopted. Now this rule applies to the simplified taxation system as well.

The organizations paying the uniform tax on imputed income (hereinafter – the UTII), previously were also exempt from property tax in respect of those real estate that is used in the activity subject to UTII22. In April 2014 the Federal Law that changed this rule was published: now this exemption does not apply to real estate, in respect of which the corporate property tax base is defined as cadastral value23. The UTII amount for 2014 shall be calculated for the period from 1 July 2014 till 31 December 2014 as ½ of the cadastral value of the real estate as of 1 January 2014, multiplied by the appropriate tax rate net of the calculated amount of the advance payment for 9 months of 201424. The amount of the advance payment is calculated as ¼ of the cadastral value of the real estate as of 1 January 2014, multiplied by the appropriate tax rate.

- From 1 January 2015 the law of the RF subject can establish the tax rate amounting to 0% for individual entrepreneurs, registered for the first time after the said date25. This benefit is provided for entrepreneurs operating under the simplified or patent tax system, and only for the types of entrepreneurial activity that will be determined by the law of the RF subject. Following the tax period, the share of income from the activities subject to the tax rate amounting to 0%, in the total income shall make up at least 70%. The tax benefit will be applicable continuously during 2 tax periods from the date of state registration. The “tax holidays” are established till 1 January 2021; after that date the benefits do not apply.

- Criminal proceedings on tax and duty evasion are now instituted under the common procedure. In 2011 the Criminal Procedure Code of the RF was amended so as the basis for institution of such proceedings could be only materials sent by the tax authorities to the investigative authorities to decide on institution of criminal proceedings26. In October 2014 this procedure was cancelled27.

The information on tax offences received from the investigative authority are sent by the investigator to the tax authority which is higher than the tax authority, where the taxpayer is registered, not later than 3 days from the receipt of the relevant information. The tax authority shall, not later than 15 days from the receipt of the communication, send to the investigator the appropriate opinion on the existence of violation of the legislation on taxes and obligations, or on the lack of information about such violation. Tax inspectors can also inform the investigator that the decision on the results of a tax audit is not yet made or has not entered into force.

After obtaining the opinion of the tax authority, but not later than 30 days from the receipt of the communication on the offence, following the results of review of this opinion the investigator shall make a procedural decision. If there are reasons and sufficient data evidencing the constituent elements of offence, the investigator can institute criminal proceedings before receiving from the tax authority such opinions or information as well.

In addition, now bodies of inquiry may carry out urgent investigative actions in criminal cases on tax offences28.

- Point 5 of article 174 of the Tax Code of the RF, edition from 29 December 2014.

- Point 3 of article 169 of the Tax Code of the RF, edition from 29 December 2014.

- Point 6 of article 145 of the Tax Code of the RF, edition from 29 December 2014.

- Point 3.1 of article 169 of the Tax Code of the RF from 24 December 2014.

- Point 1 of article 269 of the Tax Code of the RF from 29 December 2014.

- Point 11 of article 250 of the Tax Code of the RF from 29 December 2014.

- Point 8 of article 271, Point 10 of article 272 of the Tax Code of the RF from 21.07.2014.

- Sub-point 7 of point 4 of article 272; sub-point 6 of point 7 of article 272 of the Tax Code of the RF from 24 December 2014.

- Sub-points 1-4 of point 7 of article 275 of the Tax Code of the RF, edition from 21.07.2014.

- Point 1 of article 5 of the Tax Code of the RF.

- Letter of the Ministry of Finance of Russia from 14 May 2014 No. 03-08-13/22654

- Point 1 of article 3 of the Federal Law from 23 June 2014 No. 167-FZ “On amendments to chapters 23 and 25 of the Tax Code of the Russian Federation”.

- Point 2 of article 3 of the Federal Law from 23 June 2014 No. 167-FZ “On amendments to chapters 23 and 25 of the Tax Code of the Russian Federation”.

- Point 1 of article 280 of the Tax Code of the RF, edition from 29 December 2014.

- Point 22 of article 280 of the Tax Code of the RF, edition from 29 December 2014.

- Point 8 of article 280 of the Tax Code of the RF, edition from 21.07.2014

- Point 24 of article 280 of the Tax Code of the RF, edition from 29 December 2014.

- Point 21 of article 280 of the Tax Code of the RF, edition from 29 December 2014

- Point 3 of article 5 of the Federal Law from 28 December 2013 No. 420-FZ ”On amendments to article 27.5-3 of the Federal Law” On the securities market” and the first and second parts of the Tax Code of the Russian Federation”

- Point 2 of article 346.11 of the Tax Code of the RF.

- Point 1 of article 378.2 of the Tax Code of the RF.

- Point 4 of article 346.26 of the Tax Code of the RF.

- Point 4 of article 346.26 of the Tax Code of the RF, edition from 01 January 2015.

- Letter of the Ministry of Finance of Russia from 02 June 2014 No. 03-05-05-01/26195

- Article 1 of the Federal Law from 29 December 2014 No. 477-FZ “On amendments to Second Part of the Tax Code of the Russian Federation”.

- Point 1.1 of article 140 of the Criminal Procedure Code of the RF, edition from 06 August 2014

- Article 1 of the Federal Law from 22 October 2014 No. 308-FZ

- Article 1 of the Federal Law from 22 October 2014 No. 308-FZ

Other Articles on Topics