CONTENTS OF LAST ISSUE

Struggle for Cyprus: How Authorities Save the Island’s Goodwill

Let us start with a well-known fact: for many years Cyprus has been and still is an almost single-option jurisdiction for international tax planning for Russian business. There are many reasons for this, starting with highly favorable tax system and ending with affordable prices for the establishment and maintenance of business of legal entities. Minor inconveniences often associated with a lack of understanding of the very form of relations with Cyprian companies or insufficiently open contacts with administrators of corporate services were compensated by the simplicity of establishing corporate structures and simply favorable climate conditions, which made it possible if not actually bring some of its staff to this country, at least to supervise independently the work of administrators with comfort by visiting their favorite resorts.

Many businessmen remember what a major breakthrough was the exclusion of Cyprus from the “black list” of offshore zones1, which made it possible to fully use the benefits of Double Taxation Avoidance Agreement executed between the governments of the Russian Federation and the Republic of Cyprus. Although for this to become possible, a number of amendments had to be introduced to the Agreement, and Cyprus in its turn had to ensure its participation in tax information exchange. Anyway, the result was beyond any expectations: Cyprus officially lost its offshore zone status in Russia, which means, from the goodwill point of view, that it received an advantage over its potential competitors.

Even introduction of pricing rules in transactions between related parties into the Russian tax legislation could not overshadow these achievements, though precisely these transactions have become a forerunner of a crackdown and combating disinvestment.

The Cyprian success did not last long – perhaps hardly anybody forgot the consequences of the banking crisis that affected the island in 2013. They included not only mass outcome of Russian clients from banks, but also prompt restructuring of holdings. Clients sought to fully exclude or limit their presence within unreliable jurisdiction.

In fact, despite difficult financial situation, at the same time the Cyprian authorities started another campaign, which was intended not only to preserve and improve the investment attractiveness of Cyprus, but also to win the competition of full-fledged offshore jurisdictions. Let us discuss below the measures that the state has been taking over the past several years and how these measures can win the interest of the Russian business.

Double Taxation Avoidance Agreements

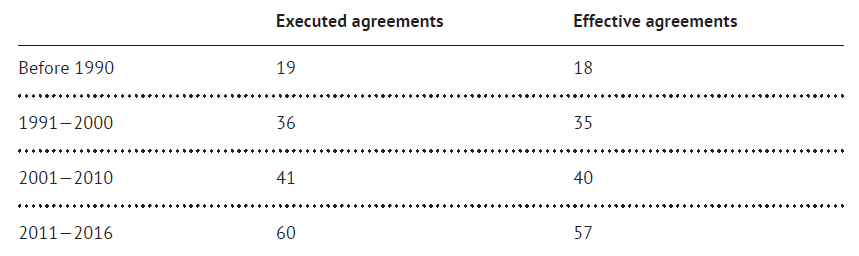

Cyprus has been actively expanding its diplomatic ties with governments of different countries concerning double taxation exemption. Provided that in Cyprus a wide range of income is already exempt from taxation (for instance, dividend and interest income, capital gains, and etc.), such agreements create a great base for international tax planning and structuring of holdings. There is no doubt that currently signed 60 (!) double taxation avoidance agreements make the island state a unique platform to work on holding companies. Below is dynamic of changes of signed and effective tax agreements over the last 30 years:

As can be seen in the diagram, over the past 6 years the number of executed double taxation avoidance agreements and effective agreements, a party to which Cyprus is, has increased by one-third. Today Cyprus has relevant agreements with such offshore territories as Mauritius, the Seychelles, San-Marino, Qatar, the United Arab Emirates, i.e. with those states, which companies can become tax-exempt profit aggregators. Of course, the recent structuring of holding companies with participation of such “profit centers” is complicated by the introduction of automatic tax information exchange systems, but this instrument remains effective, albeit in a much modified form. In its turn Cyprus has its own interest in what is going on by getting additional bonuses in the form of companies, which now must not only be opened in its territory, but also confirm its real activities – real substance – this approach helps the island to benefit again.

Preferential Tax Regimes

Another way to interest business in remaining within Cyprian jurisdiction was created at the level of internal tax policy. In this respect in Cyprus there are two similar tax regimes designed for different types of income:

Notional Interest Deduction (NID) is the deduction of notional interest in the amount corresponding to the amount of new investments made in the Cyprian company. How does it work? Beginning from the 2015 tax period Cyprian companies and permanent representative offices of foreign companies operating in Cyprus in calculation of income tax can use the deduction of notional interest equal to the product of new investments to the authorized (added) capital and notional interest rate. New investments in the capital mean the authorized (added) capital paid after January 01, 2015 (both in cash and in kind). The notional interest rate is an interest rate on a 10-year government bond of the country, where new investments have actually been implemented, increased by 3%. In this regard the minimum amount of deduction is calculated based on yield on the 10-year Cyprian government bond increased by 3%.

Use of such deduction is not allowed, if it exceeds 80% of the taxable profits of the company, accordingly, this deduction cannot form losses. Moreover, the law contains provisions that prevent tax evasion using this deduction, namely:

- Notional interest cannot be calculated in respect of new investments in the capital, the source of which are reserves existing as of December 31, 2014; authorized capital existing as of December 31, 2014; revaluation of assets of the company.

- To avoid double application of deduction in respect of the same investments in the capital, where the new investments of the company have been directly or indirectly received from the new investments of the other company, deduction of notional interest will be possible only for one of the companies.

- Deduction of notional interest of one company shall be subject to reduction by the amount of actual interest accepted as expenses by the other company, if the source of formation of new investments of the first company is the amount of debt financing of the latter company.

Thus, in order to apply deduction, precisely “new capital” shall be invested in the Cyprian company, i.e. funds that had not been in its possession until the beginning of 2015. In this regard the Tax Department of Cyprus explains that the capital in the form of released debt or an offset of creditor’s claim paid as the investment will be considered a proper basis for the deduction, if such release (offset) has been carried out since 2015, even if the creditor’s claims regarding the indebtedness arose before December 31, 2014 inclusively.

The advantage received by the Cyprian company may also be applied, if after the receipt thereof there was a change of shareholders in the company. It has also been confirmed by the official position of the Ministry of Finance of Cyprus.

Thus, the NID regime makes it possible to reduce the tax base on income tax paid by the Cyprian company by 80%. In this regard, unlike previous schemes stipulating “mirror” loans from offshore companies, investments in the company must be real, free of charge and increase the amounts of authorized or added capital of recipient of the investments.

Intellectual Property Tax Regime (IP Tax Regime) is a preferential tax regime existing in Cyprus since 2012, but it truly interested Russian business only when Russia began actively combating offshores. The essence of IP Tax Regime is that the Cyprian tax legislation exempts from taxation about 80% of profit of Cyprian companies, which receipt is associated with the use of intellectual property items. Such generosity is explained by the fact that regardless of the specific amount of investment in such items, the authorities have established the 80% rate as notional and requiring no documentary proof. To apply the exemption the company only needs to prove that it is entitled to use the intellectual property item. Moreover, the Cyprian company may be both the owner of the item or hold it by virtue of license. No matter where the intellectual property item was registered and its specific features (it can be a patent, trademark, franchise, computer program or any other item).

Attention should be drawn to the fact that conditions, which Cyprus offers regarding this tax regime, seem fantastic. By using it, the Cyprian company is not restricted in methods and amounts of payment of royalties, distribution of dividends and it is entitled to use all advantages of double taxation avoidance agreements executed by Cyprus and EU Directives exempting from a range of taxes. In Cyprus corporate tax is maintained at the rate of only 2.5% of the amount of all income received from the use of the intellectual property items.

However, not everything in the garden is rosy.

As known, there is an organization, one of the main objectives of which is to prevent illegal and unfounded use of preferential tax regimes and patterns of international tax planning, aimed solely at tax avoidance. This organization, famous OECD (Organization for Economic Co-operation and Development), carefully monitors and thwarts any attempts of its members to grant preferences to taxpayers, such as the abovementioned IP Tax Regime. The OECD reaction to introduction of such regime is unambiguous and leaves no reason for doubt that the international community will fight it by any available means.

Cyprus is not an OECD member; however the adherence to its principles remains an important item on the agenda of the economic policy of the island. As it was announced in the Statement of the Ministry of Finance of Cyprus dated December 30, 2015, taxpayers using IP Tax Regime need to decide and choose other taxation regime for themselves until July 01, 2016. As for IP Tax Regime, it will be abolished as not complying with the rules of the OECD. It was assumed that during the first half of 2016 actions of legislative bodies of Cyprus would be focused on changing the legal framework in respect of intellectual property pursuant to the recommendations of the international organization.

Nevertheless, until now there is no information about adoption of any amendments related to the use of IP Tax Regime. Today we can definitely say that the companies, that have been using this preferential regime before, can still use it this year. We will see what happens next. If the Cyprus authorities decide to follow the common path of the OECD, in the near future we will see a complete rejection of the IP Tax Regime or such revision thereof that will make it possible to apply deductions only in the amount of proven costs for acquisition or maintenance of the intellectual property item. It is entirely possible that IP Tax Regime may be applied only concerning items that have been registered with the Intellectual Property Office of Cyprus. Thus, everything will depend on what interests the island government pursues.

In this article we have considered only measures, which the authorities of Cyprus use to keep the business in Cyprus and attract additional investments in corporate institutions of the island. Measures related to keeping Cyprus attractive as a place of residence for individual taxpayers is a subject for a separate discussion.

Particular attention should be paid to an opposite topic concerning possible tightening of legislation of Cyprus primarily related to the need of the island to prove its openness and commitment to international principles of combating tax evasion and money laundering. These issues will be discussed when the legislative body or the Ministry of Finance of Cyprus will go for serious measures.

Anyway, when making a decision to enjoy any advantages of the Cyprian jurisdiction it is worth to refer to experts and get the most up-to-date information about possibilities the existing taxation conditions provide.

- This is referred to the List of Countries and Territories That Offer Preferential Tax Regime and (or) Not Stipulating Disclosure and Provision of Information in the Course of Financial Operations (Offshore Zones) approved by Decree of the Ministry of Finance of Russia No. 108н dated November 13, 2007, from which Cyprus has been excluded since January 01, 2013.

Other Articles on Topics