CONTENTS OF LAST ISSUE

Well-Being Comes Through Action, Not Through Prayer

Lately in the pages of Korpus Prava.Analytics we have frequently addressed inheritance-related topics. It is not a mere coincidence. Inheritance matters, or as they say in modern language – inheritance transfer, are currently very important for business community. It happens for a reason. Our Russian entrepreneur who started his way in the 90s at the age of 20-30 has achieved everything by now: he survived 1991, 1998, 2008, 2014 and according to the common saying planted a tree, built a house, raised a son… This entrepreneur is now over 50, his son is at least 25, so it’s time to pass his business to this “son”.

Once becoming very important, the matter of inheritance transfer to one’s successors has immediately turned into a problem. First of all, it happened due to the fact that assets are either ill-structured or unstructured at all. Cases when a person wishing to appoint a successor is not able to legally confirm his rights to an asset are quite frequent. The case becomes particularly complicated if this person has already passed away. Sometimes it’s impossible for a “son” to get assets from a nominee who had non-binding obligations to his “father”. Moreover, while wishing to transfer his assets to a particular heir in his lifetime or give them under the will after death, a person faces certain legal restrictions, such as statutory share and joint ownership of spouses. Finally, one shouldn’t forget that in case of inheritance transfer after employer’s death, unless such transfer has been prepared beforehand, assets get frozen for at least 6 months. In such cases problems with real asset disposal tend to arise and corporate governance of legal entities may be paralyzed. Sometimes it becomes impossible to get through to providers of corporate services that manage foreign companies. In other cases heirs have no idea of asset composition; they don’t know anything about the companies, their location and maintenance or how to work with contacts. It turned out that life leads one to think about inheritance transfer beforehand, before it’s too late.

Typical risks

What should a person who has decided to structure his “estate” consider?

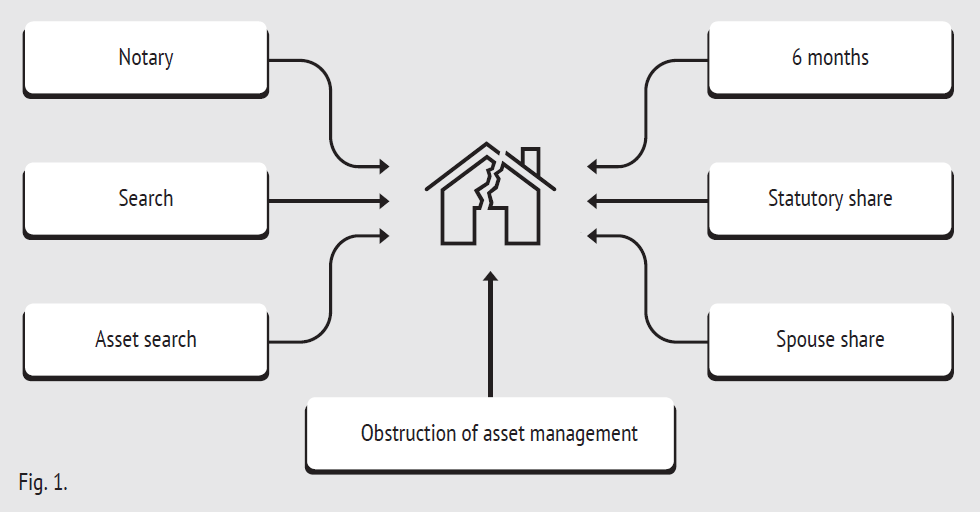

First of all, he should consider matters that heirs will face in case everything takes its course (Fig.1).

- 6-month period for accession to heirship. This period starts from the death of a testator. It’s impossible to register one’s heirship before the abovementioned period. Therefore, for half a year a heir will not be able to control real estate or broker’s securities, or stakes and shares of Russian and foreign companies. The most unfortunate scenario may happen, when a testator is the sole shareholder (member) and director of a legal entity. Activities of such company will be frozen for 6 months, as the change of the director may be performed only after registration of heirship for shares (stakes).

- “Unplanned” heirs. 6-month period is given in accordance with the legislation for all potential heirs to make their claim for heirship. During this period some people may appear that haven’t been taken into account either by a testator or by other heirs. If they prove their heirship, they will not only have to be shared with, but probably also given access to asset management.

- Asset search. In cases when inheritance transfer hasn’t been registered beforehand, asset search (particularly for foreign assets) may turn into a “crusade”. This search is not complicated for real estate and legal entities located in Russia. However, in order to find a foreign company, knowing just a country of registration is not enough. One should know not only registration data, but also contact details of the corporate administrator of this company. Moreover, ideally one should be an authorised representative in order to contact this administrator, otherwise communication may be hindered.

- Spouse share. This restriction implies that unless otherwise stated in the prenuptial agreement, the spouse of a deceased has a right to 50% of marital property. It means that even with a will for “all property” in favour of a particular heir, this heir will actually get only 50% of all property that belonged to a deceased. It won’t be considered a problem for a happy family. However, if to quote L.N. Tolstoy “Happy families are all alike; every unhappy family is unhappy in its own way”, one may expect various unpredictable disputes to arise. For example, spouses may live apart and don’t consider themselves spouses, but legally stay married. In this situation spouse share rights will be valid. One more example is when a spouse bought an asset before marriage, accepted it as a gift or inherited it. This asset is obviously the property of this spouse. However, all the money from disposal of this asset during marriage, especially a new asset bought with this money, is joint property of both spouses and will be covered by provisions of matrimonial regime.

- Statutory share. The requirement of statutory share in the estate implies that testator’s dependents (primarily minor children, disabled adult dependents), who even with a will have a right to 50% of the share they would have obtained in case of hereditary succession without a will.

In order to avoid the abovementioned complications, one should consider structuring of assets beforehand and perform certain actions that will eventually lead to a smooth and easy inheritance transfer to a successor and will allow a testator:

- Firstly, to be certain that asset management will get into the hands of the heir he counts on;

- Secondly, not to worry about asset management being obstructed.

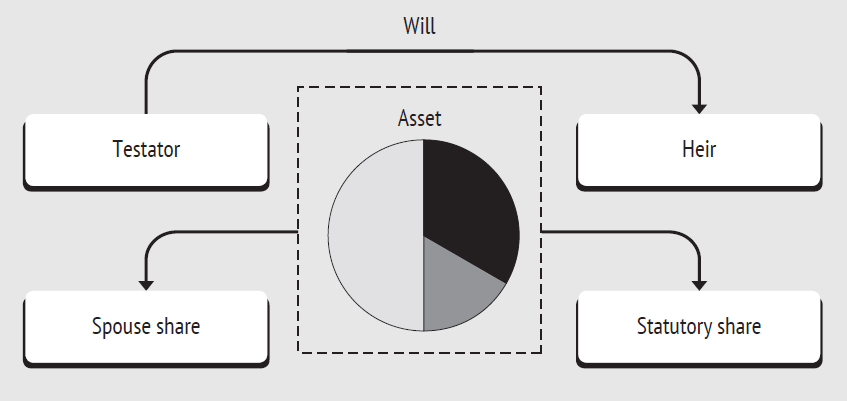

Will

We will start with a simple instrument that is very obvious. One may dispose of property on occasion of death by drawing up a will. A testator is entitled at his own discretion to leave his property to any persons, assign heir shares in any manner he deems fit, disinherit one, any or all heirs at law with no reason given. The size of the estate is limited only by spouse share, which may be avoided by signing a prenuptial agreement beforehand. Discretion of the will is restricted only by regulations on statutory share, which are obligatory.

However, a testator is not able to predict all possible future changes in his will. Such changes include appearance of new heirs, marriage of children, remarriage of the surviving spouse, misdeeds of heirs, etc. Moreover, even with a prenuptial agreement, absence of minor heirs and existing will containing detailed information on the assets, a heir will have to wait for 6 months for accession to heirship.

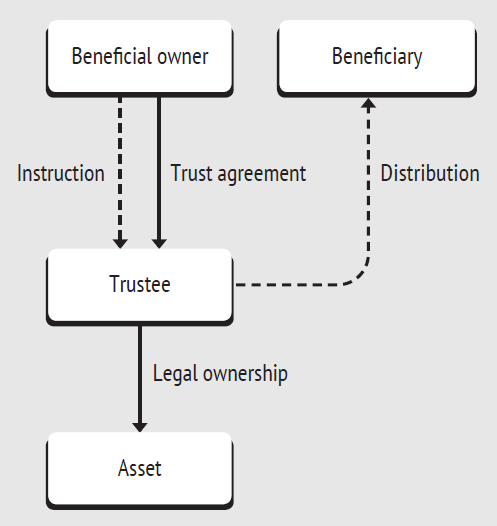

Trust

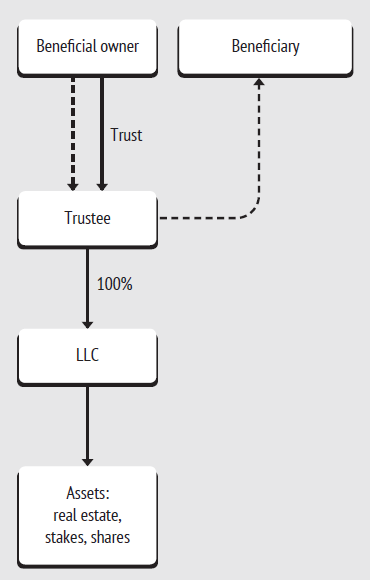

In order to avoid 6 month asset freeze, one may use such an instrument as trust. A typical trust structure is illustrated in the figure below.

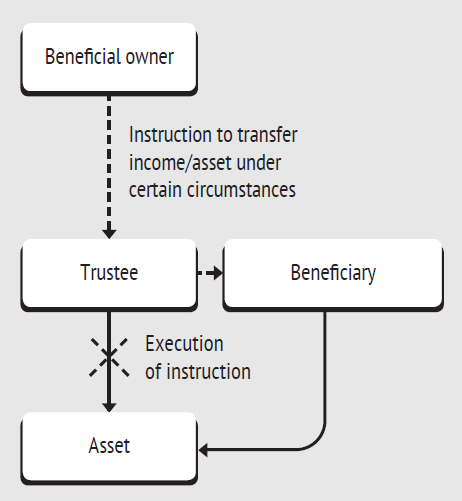

However, this typical trust structure is used only in Commonwealth countries with trust law. In order to assign an asset to a trust located in Russia or other continental law countries, one will have to transfer it to a legal entity registered in a trust law country. The trust structure for such assets is shown in figure below.

Due to the fact that upon property transfer the ownership title will be registered in the name of a trustee, this property will not be included into the estate and all disputes between “heirs at law” are limited only to those types of property that weren’t assigned to a trust and remain registered under testator’s name. Thus, structuring of assets via trust will allow a testator to avoid 6-month period for accession to heirship, as well as regulations on statutory and spouse shares. Pursuant to a trust agreement a settlor may give any instructions. Thus, one may determine cases when the property is distributed in fixed shares between heirs, or an appointed beneficiary will continue to receive income from management of assets assigned to a trust after the death of a settlor, if a relevant instruction is given. Alternatively, a settlor may give instructions on trust termination and transfer of an asset to a specific beneficiary under certain circumstances, including settlor’s death.

Fund

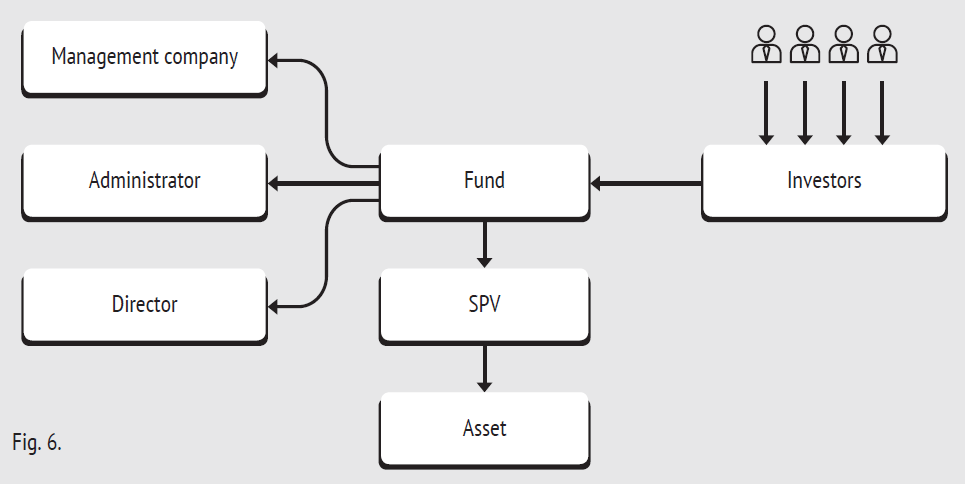

In case a potential testator doesn’t contemplate transfer of ownership to a trustee due to various reasons, such instrument as a fund serves as an alternative to a trust.

As an asset management instrument fund has as figure 6.

Unlike trusts where one avoids all restrictions of inheritance law by changing of the asset owner and leaving specific instructions in relation to an appointed beneficiary, with funds one transfers assets to the ownership of a fund, a potential testator becomes fund’s investor managing these assets, and the abovementioned aims are gained due to an increased level of non-disclosure of information on fund’s investors.

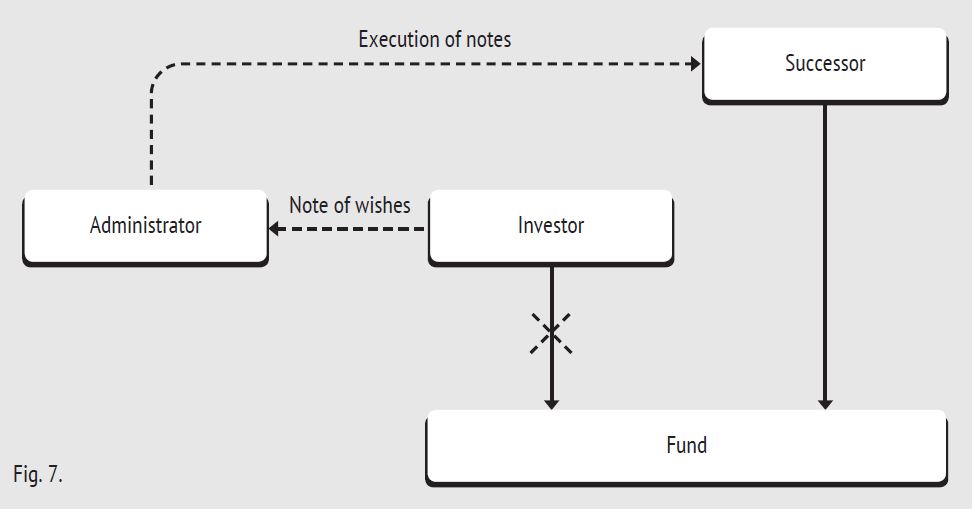

Non-disclosure implies that information on fund’s investors is not disclosed to third persons, as well as during information exchange sessions. As a rule, such participation doesn’t lead to participation in controlled foreign companies for the purposes of the Tax Code of the Russian Federation. Thus, during asset search such property as fund shares will be impossible to find, which will allow to exclude them from the estate and the list of marital property. A heir will be notified by a testator on asset transfer to a fund beforehand and will be able to gain fund investor’s rights by using a note of wishes, executed and delivered to a fund administrator by a testator at reasonable time (Fig.7).

Option

Less attractive and secure but in some cases an efficient instrument is asset registration in the name of a third party with simultaneous signing of an option agreement with a potential heir. Pursuant to the option agreement, in accordance with the terms therein one of the parties is entitled to claim the fulfilment of obligations thereof by the other party within the fixed period of time (including payments, transfer or acceptance of property). In a given case signing an option agreement with a potential heir by the third party will give this heir the right to acquire an asset under certain circumstances. This method of asset structuring is not systematic, it is difficult to multiply and it is 100% dependant on whether there is a trusted third person among people known to a testator. However, under certain circumstances considering personal characteristics of some testators this option may seem the only one.

Thus, any of the abovementioned instruments of asset structuring for inheritance transfer is valid. It’s possible to use different instruments for different assets, which will allow diversifying risks. No matter what the state of his assets is or how young their owner feels at the moment, he must consider how the ship will sail when the captain comes ashore.

Other Articles on Topics