CONTENTS OF LAST ISSUE

DAC 6 Directive: sixth step of the european evolution of information disclosure

EU Council Directive 2018/822 amending Directive 2011/16/EU as regards mandatory automatic exchange of information in the field of taxation in relation to reportable cross-border arrangements was published on May 25, 2018. This Directive is also commonly referred to as DAC6 – Directive on Administrative Cooperation in (direct) taxation in EU, volume 6. This Directive is the sixth in a series of directives developed to encourage cross-border exchange of tax information in EU, and makes a part of step 12 in the BEPS Project (OECD base erosion and profit shifting project).

DAC 6 Directive provides for the obligation to disclose cross-border arrangements bearing hallmarks of aggressive tax planning to the tax authorities. According to EU aggressive tax planning means reduction of tax obligations by taxpayers via arrangements that may be technically legal, but their substance contradicts the letter of the law. Aggressive tax planning is also reflected in the use of loopholes in the tax system and inconsistencies between tax systems, which may lead, for example, to double tax evasion.

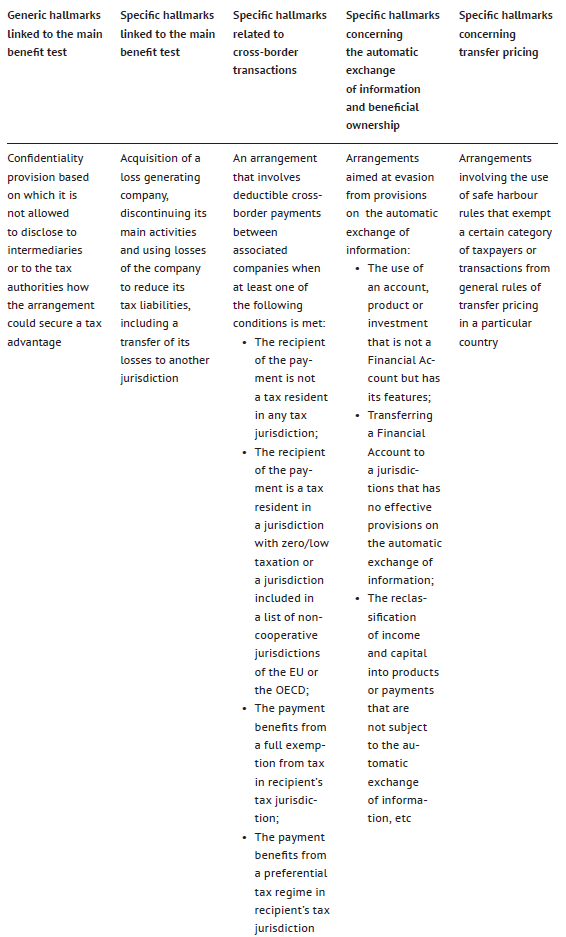

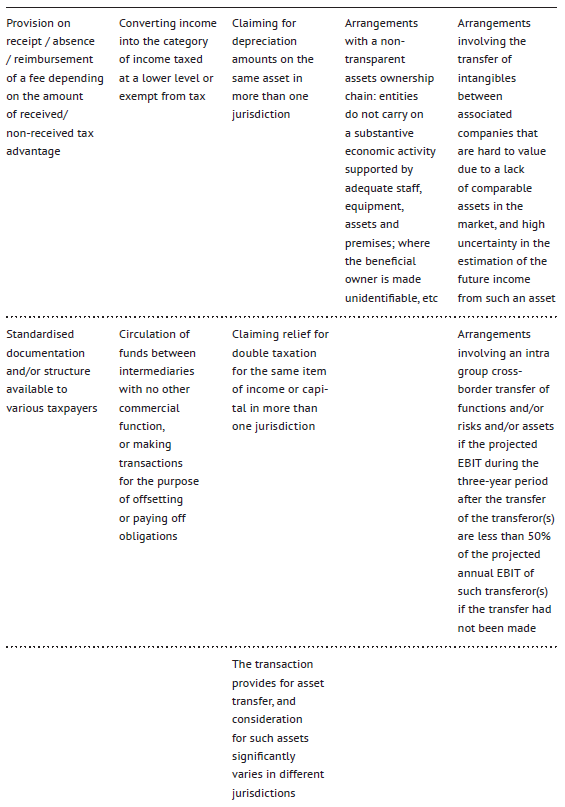

As mentioned above, in accordance with DAC 6 information on cross-border arrangements implemented by companies located in EU and bearing hallmarks of aggressive tax planning shall be disclosed. Such hallmarks are listed in Annex IV to DAC 6 and are divided into the following categories:

- Generic hallmarks linked to the main benefit test;

- Specific hallmarks linked to the main benefit test;

- Specific hallmarks related to cross-border transactions;

- Specific hallmarks concerning the automatic exchange of information and beneficial ownership;

- Specific hallmarks concerning transfer pricing.

A non-exhaustive list of hallmarks is given in the table:

An arrangement is recognized as cross-border if its participants are located in more than one Member State or in a Member State and a third country, and it meets at least one of the following criteria:

- Not all participants are tax resident in the same jurisdiction;

- At least one participant is a dual tax resident;

- At least one participant carries on a business in another jurisdiction through a permanent establishment situated in that jurisdiction and the arrangement forms part or the whole of the business of that permanent establishment;

- At least one participant carries on activities in another jurisdiction without being resident or creating a permanent establishment situated in that jurisdiction;

- The arrangement has a significant impact on the automatic exchange of information or the identification of beneficial ownership.

The information on arrangements which should be disclosed in accordance with DAC 6 includes:

- Identification data of intermediaries and taxpayers, including their names, date and place of birth (for individuals), details of tax residency, taxpayer identification number, and, if applicable, details of companies associated with taxpayers;

- Details of hallmarks listed in Annex IV to DAC 6 and mentioned above;

- General details of the cross-border arrangement without disclosure of commercial, industrial or professional secrets or trade process, and information that would contradict the public order;

- Date of the first step of the arrangement implementation;

- Value (amount) of the arrangement;

- National provisions forming the basis of the arrangement;

- Details of the Member States involved in the arrangement;

- Details of any other person in Member States likely to be affected by the arrangement.

The obligation of information disclosure is vested upon intermediaries, and in case there are no intermediaries or DAC 6 provisions do not apply to intermediaries for any reason, upon taxpayers themselves. Who are intermediaries? In DAC 6 an intermediary is defined as any person that designs, markets, organises or makes available for implementation or manages the implementation of a reportable cross-border arrangement. An intermediary should either:

- Be a resident in a Member State;

- Have a permanent establishment in a Member State through which the services in respect of the arrangement are provided;

- Be incorporated in or governed by the laws of a Member State;

- Be registered with a professional association related to legal, tax or consultancy services in a Member State.

The Directive provides a fairly broad definition of an intermediary, which may apply to almost any person accompanying a transaction. This definition may include lawyers, consultants, accountants, banks, insurance companies, financial consultants, corporate administrators, and other service providers.

It should be noted that DAC 6 is a general directive which Member States are required to implement in their national legislation. It is also expected that Member States will issue guidelines with detailed information about who exactly and how will disclose information as an intermediary, what will be the methodology for recognizing a reportable transaction.

Member States were required to implement DAC 6 in their national legislation by 31.12.2019, and to start applying the new legislation from 01.07.2020; the first reporting on cross-border transactions was to be submitted no later than 30.07.2020, the first reporting on cross-border transactions made between 25.06.2018 and 01.07.2020 was to be submitted no later than 31.08.2020, and the first exchange of information was to take place no later than 31.10.2020. However, 2020 has brought a lot of surprises and the above-mentioned periods were partially shifted to 2021.

To date, the new legislation has been published in most Member States (Austria, Belgium, the Netherlands, France and others), certain states have not yet adopted the legislation which is currently in the draft stage (Cyprus), and certain states have issued guidelines, while a vast majority of Member States has taken advantage of the extension of reporting deadlines.

DAC 6 is a new stage in the evolution of information disclosure, the practical part of which is not yet developed. In order to determine whether a person is an intermediary or not, to develop a clear understanding of the hallmarks of aggressive tax planning and disclosure methods, to assess risks and consequences of the automatic exchange, it is necessary to review the national legislation and methodological recommendations of a particular Member State.

Other Articles on Topics