CONTENTS OF LAST ISSUE

CHALLENGES / OPPORTUNITIES changes in Hong Kong taxation

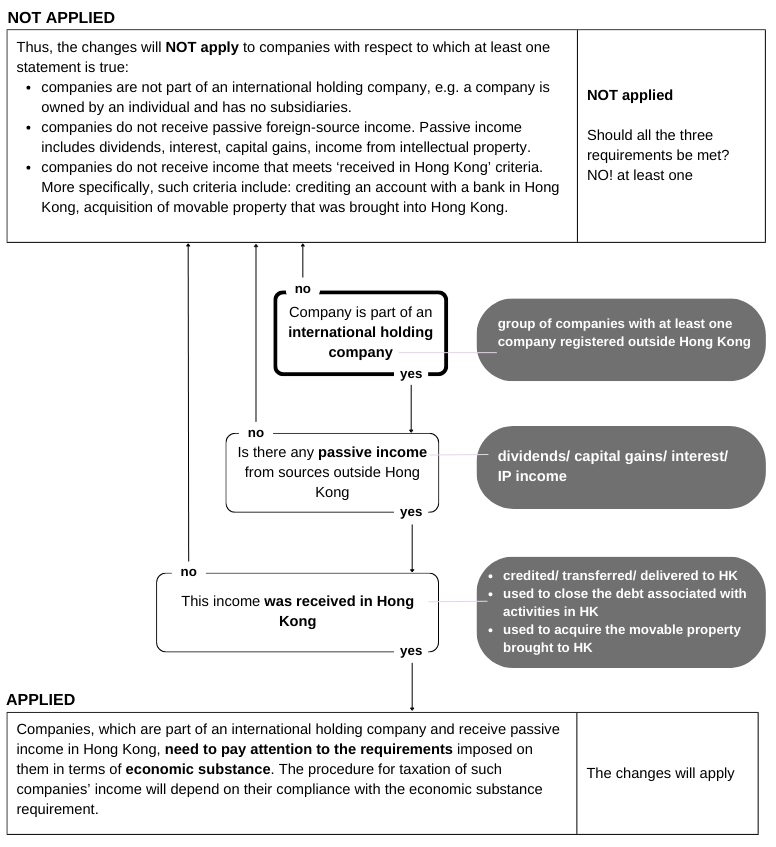

Hong Kong laws governing the taxation procedure for passive income from foreign sources were amended. Requirements for exemption from the corporate tax were supplemented by the economic substance requirement for the companies that meet the criteria specified in the law.

These changes will apply to companies receiving passive income that are part of an international group of companies.

EXTRA OBLIGATIONS OR EXTRA OPPORTUNITIES?

AS before

Offshore profit (meeting ALL of the following requirements) was NOT taxable in Hong Kong:

- place of contract execution – NOT Hong Kong;

- persons responsible for approval, signing and performance of a contract are non-residents of Hong Kong;

- search for counteragents is performed by non-residents of Hong Kong;

- revenue is NOT credited to the account with a bank outside Hong Kong.

The remaining profit was onshore and was subject to taxation.

WHAT HAS CHANGED

If a company is part of an international holding company and receives passive income in Hong Kong, then by complying with the economic substance requirement it may be exempted from taxation of such income.

Please, note that in the past, a company had to pay tax on income, which was transferred to Hong Kong, as on onshore income. Now, after compliance with the economic substance requirements, such income is exempt.

Other Articles on Topics