CONTENTS OF LAST ISSUE

Taxation in Cyprus. Update

He that is warned afore is noght bygiled

We have already written about the expected changes in the tax field of Cyprus. This article is the update on the expected changes as of October 26, 2022. You may use the updated information to plan your next steps.

Changes in the tax field of Cyprus that have ALREADY took effect (after June 21, 2022 when our previous article was written)

NOW

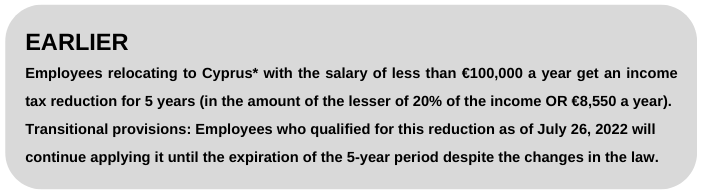

Employees relocating to Cyprus* with the salary of less than €55,000 a year can get an income tax reduction in the amount of 20% of the income (or €8,550 a year, whichever is the lesser) for 7 years.

IMPORTANT TO

International companies / their employees who will choose Cyprus for relocation.

_______________________________________________________________________________________

NOW

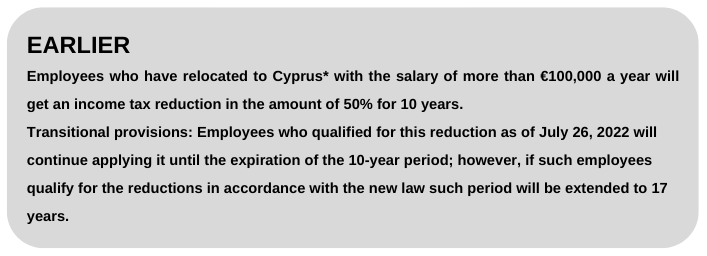

Employees relocating to Cyprus* with the salary of €55,000 a year will get an income tax reduction in the amount of 50% of the income for 17 years.

Certain reductions will be available for employees* who relocated after 2015 and who had the annual income of more than €55,000 but less than €100,000 (i.e. who did not meet the reduction criteria before).

IMPORTANT TO

International companies / their employees who will choose Cyprus for relocation.

_______________________________________________________________________________________

NOW

Requirements for transfer pricing (TP) documentation to be maintained depending on the scope of activities with related parties have been defined**:

- Up to €750,000 – it is NOT required to prepare the Local File

- More than €750,000 – the Local File should be prepared

- More than €750,000,000 – the Master File should be prepared

Companies should prepare and submit Summary Information Table (SIT) with the information regarding transactions with related parties.

TP documentation should be prepared within 15 months.

Penalties for violations – from €500 to €20,000.

IMPORTANT TO

Cypriot companies handling transactions with related parties.

Notes

* – in case certain past employment requirements are met.

** – relatedness criterion: ownership / control / income right interest is 25%. Also, parties will be considered related if they have a common related party that meets this criterion.

Changes in the law field of Cyprus that will take effect on December 31, 2022

CHANGES STARTING FROM DECEMBER 31, 2022

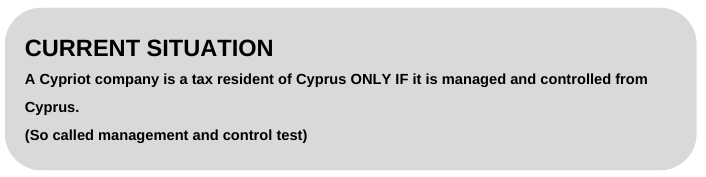

A Cypriot company will ALWAYS be a tax resident of Cyprus EXCEPT FOR cases when it is a tax resident of another country.

Management and control test will still be applied for foreign companies.

IMPORTANT TO

Cypriot companies that were not registered as taxpayers in any country (so called stateless companies).

_______________________________________________________________________________________

CHANGES STARTING FROM DECEMBER 31, 2022

Cyprus will withhold WHT on interest, dividends and royalty in case their recipient is a company that is a taxpayer in the jurisdiction blacklisted by the European Union[1] or a company that is NOT a taxpayer in any country and is registered in the above mentioned jurisdiction.

Withholding tax rates:

- 17% for dividends (except for dividends payable by the listed Cypriot companies)

- 30% for interest (except for interest on exchange-traded securities)

- 10% for royalty

IMPORTANT TO

Cypriot companies that pay dividends, interest or foreign counterparties from the EU blacklisted jurisdictions.

Remote changes in the tax field of Cyprus

PROBABLE CHANGES

It is expected that the withholding tax on dividends, interest and royalty paid to low-tax jurisdictions will be introduced by December 31, 2024[2]

IMPORTANT TO

Cypriot companies having counterparties or shareholders from low-tax jurisdictions.

It is important to understand that the data in this table is preliminary and indicative. The actual situation may differ significantly.

[1] At the time of this article, the EU blacklisted jurisdictions include the following countries: American Samoa, Anguilla, Bahamas, Fiji, Guam, Palau, Panama, Samoa, Trinidad and Tobago, Turks and Caicos Islands, US Virgin Islands, Vanuatu. The updated list may be found here: https://www.consilium.europa.eu/en/policies/eu-list-of-non-cooperative-jurisdictions/

[2] In accordance with the Cyprus’ National Recovery and Resilience Plan.

Other Articles on Topics