CONTENTS OF LAST ISSUE

Foreign companies. What has changed?

Over the past two years, a lot of changes were made both to the legislation of jurisdictions popular for incorporation of foreign companies, and at the level of double taxation conventions. This article reviews the main changes in order to give a general idea of peculiarities of such jurisdictions.

Offshore

In offshore jurisdictions, provisions on economic substance were introduced back in 2019. Such jurisdictions include, inter alia, Belize, the Seychelles, Mauritius, the Cayman Islands, Bermuda, Jersey, Guernsey, and the Isle of Man.

The Economic Substance Act introduced requirements for economic presence for all companies and limited liability partnerships that are registered and are tax residents of such jurisdictions.

However, not all companies and partnerships are required to confirm their offshore tax residency status.

Companies that are subject to this requirement and are required to provide economic presence are companies that carry out “relevant activities” defined as:

- Financial companies (banking business, insurance business, stock exchanges);

- Shipping business (shipping companies);

- Holding business;

- Business in the field of intellectual property;

- Distribution and service business.

Entities that do not fall under the law are companies that declared themselves tax residents of another jurisdiction, or companies that carry out activities other than “relevant” ones.

Requirements for the economic presence of companies are relatively abstract; it is assumed that practice will show the numerical value of criteria. Requirements include the following:

- The number of employees corresponding to the scale of the company’s business, and the employees should have the education and experience necessary to perform their work duties that correspond to the declared main activity of the company;

- The office required to accommodate staff and carry out the company’s business (presumably, it is not just about office lease, but also about workplaces equipped with office equipment, telephone connection, Internet connection);

- Maintaining accounting records and preparing financial statements on a regular basis (it is obvious that an appropriately qualified person responsible for this function should be appointed);

- Expenses incurred by the company should be adequate to the activities carried out by the company, both in volume and in substance. Presumably, this means that expenses should be allocated to making a profit and correspond to the declared main activity of the company.

In practice, now this is executed only as filling out questionnaires with appropriate fields being ticked, while additional supporting documents are not requested. Whether this procedure will last long is yet unclear, so it seems consistent to record the real status and keep the documents confirming the information reflected in the questionnaires ready.

Double taxation conventions

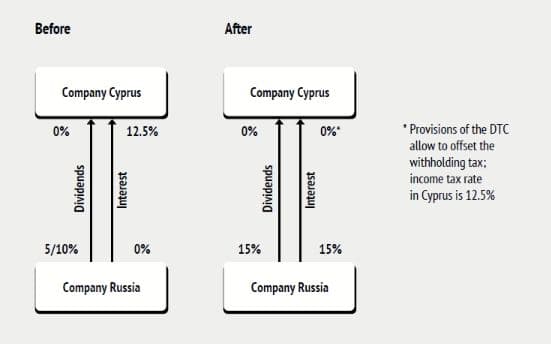

Provisions of double taxation conventions (hereinafter, the DTC) concluded by the Russian Federation with Cyprus, Malta, and Luxembourg were revised, while the agreement with the Netherlands was not reached, so the convention will be terminated.

Consequences of amendments made to the DTC are shown in the diagram below, using the DTC with Cyprus as an example.

Consequences of the termination of the DTC with the Netherlands are shown in the scheme below.

Therefore, changes to the legislation of offshore jurisdictions will affect the cost of administration of companies due to the need to submit additional reports, and companies that conduct certain types of activities will have to comply with special legal requirements.

Changes and termination of DTC entail an increase in the tax burden and raises the issue of whether it is appropriate to use a foreign company as an actual income recipient. On the one hand, foreign companies are often used as part of the tax planning mechanism, but this is not the only reason for structuring, for example, capital using a foreign company. Given the above, it seems reasonable to determine the goals that are being pursued and to critically evaluate the structure based on them.

Other Articles on Topics