CONTENTS OF LAST ISSUE

Automatic exchange of financial information in 2022

In 2016, the Russian Federation signed the Multilateral Agreement on the Automatic Exchange of Financial Information, based on which Russian and foreign government authorities exercising control and supervision in the area of taxes and duties automatically, i.e. in a predetermined format and mode, shall exchange information on residents and their transactions, accounts and deposits in foreign banks and financial market organizations, as well as on the amount of funds and the value of property concentrated abroad with each other.

The convention has provided a comprehensive tool that makes it possible to establish interaction between government authorities of different countries and ensure greater transparency in finance and, particularly, taxation. It was the exchange between the countries that ensured the effective implementation of policies to combat money laundering and evasion of income taxation at the global level.

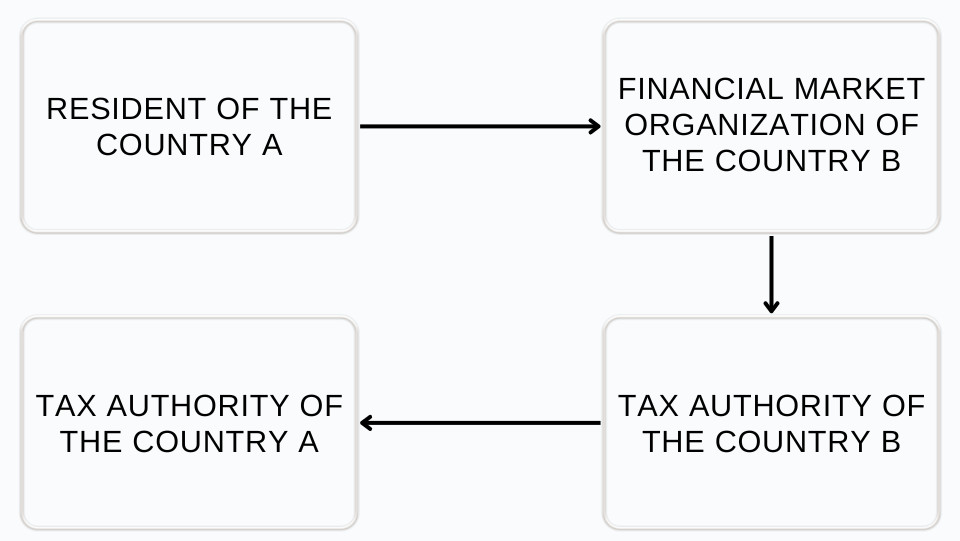

At its core, the process of the automatic exchange is linear in structure. The initial link in the information exchange chain is a country resident who accumulates funds on accounts (deposits) in a financial market organization located in another country. When undergoing the Compliance procedure at the bank, the resident provides their information that makes it possible to identify them as a taxpayer of the relevant country. After collecting and analyzing the information received, the bank or other financial market organization sends it to the national tax authority at its location. Having received the necessary information, the tax authorities of the country in which the funds are accumulated and the tax authorities of the country of which the relevant person is a resident share the accumulated data for a certain period, which is usually a calendar year, with each other through internal communication channels.

This process of information movement may be depicted using the following diagram:

It should be noted that strictly defined information about taxpayers is subject to exchange, and the exchange of information itself is not a “crude” method of disclosing confidential information but a tool to ensure financial stability and counteract evasion of taxation using foreign structures.

Speaking about information, it is necessary to pay attention to the fact that only specific, few and truncated data are subject to collection and exchange in the first place. They include the following:

- full name, taxpayer identification number in the country of residence of the client or beneficiary;

- information on transactions, accounts and deposits of clients;

- information on the amount of the insurer’s obligations to customers or beneficiaries;

- information on the amount of funds and the value of property of clients and beneficiaries available for the financial market organization;

- information on the value of property of clients and beneficiaries accounted for by the financial market organization carrying out depositary activities;

- information on pension accounts of clients and beneficiaries;

- information on central counterparties to clients and beneficiaries;

- information on payments and transactions made in connection with accounts (deposits) and agreements with financial market organizations under which they accept funds or other financial assets for safekeeping, management, investment and other transactions for the benefit of the client or directly or indirectly at the expense of client.

However, it is important to understand that not all countries participate in the automatic exchange yet and some no longer participate in it. The current lists of countries with which the Russian Federation automatically exchanges financial information are recorded in the form of Decrees of the Federal Tax Service of Russia. Decree of the Federal Tax Service of Russia No. ЕД-7-17/450@ dated 27.05.2022 is currently in force.

Nevertheless, there is now a threat of disruption of the harmonious functioning of the exchange system due to the desire of a number of countries to stop cooperation in taxation. Thus, some European countries are considering terminating the exchange and curtailing the double taxation avoidance regime: Germany and Austria. The exchange has already been terminated with some countries, e.g. with Switzerland.

Termination of the automatic exchange could have a direct negative impact on taxpayers.

First, low awareness of national authorities of transactions taking place abroad may lead to an increase in illegal transactions and resumption of the use of criminal schemes for taxation evasion.

Second, without proper information, government authorities will be less successful in defending the interests of their citizens abroad.

Third, taxpayers will be forced to fulfill additional obligations that the automatic exchange relieved them from. For instance, the fact that a person opened an account with a bank of the country participating in the automatic exchange was one of the general set of conditions under which the taxpayer was not required to report on foreign accounts to the tax authorities of the Russian Federation.

In other words, this means that if a person opens an account with a foreign bank, and the country no longer exchanges information, the taxpayer will have to provide an annual statement of the account activity. Failure to submit the statement will result in a fine and increased control by the tax authorities, since the taxpayer will be considered a violator of the currency legislation of the Russian Federation. Moreover, there is a risk that transactions on an account that has not been reported will be deemed to be illegal foreign exchange transactions, for which a substantial fine is also stipulated.

Thus, the automatic exchange of financial information is not much of a complicated, if not a simple, process of data exchange between the competent authorities of different countries. The exchange has obvious benefits for both countries themselves and taxpayers, and its termination may have long-term negative consequences.

Other Articles on Topics