CONTENTS OF LAST ISSUE

Cyprus – an ideal jurisdiction for the establishment of Intellectual Property rights

Intellectual Property rights (IP) are like any other property right which allow creators, or owners, of patents, trademarks or copyrighted works to benefit from their own work or investment in a creation. These rights are outlined in Article 27 of the Universal Declaration of Human Rights, which provides for the right to benefit from the protection of moral and material interests resulting from authorship of scientific, literary or artistic productions.

Article 2 of the World Intellectual Property Convention of 1968 defines IP as including:

- Literary, artistic and scientific works;

- Performances of performing artists, phonograms, and broadcasts;

- Inventions in all fields of human endeavor;

- Scientific discoveries;

- Industrial designs;

- Trademarks, service marks, and commercial names and designations;

- Protection against unfair competition;

all other rights resulting from intellectual activity in the industrial, scientific, literary or artistic fields.

Cyprus IP legislation has been widely developed in the past 20 years following the emerging needs for the establishment of solid protection of IP rights both on domestic and international level.

Related with IP, Cyprus is a signatory to the following international conventions:

- EC Regulation on the Community Trademark (CTMR);

- WIPO Beijing Treaty on Audiovisual Performances;

- WIPO Performance and Phonograms Treaty (WPPT);

- Berne Convention for the Protection of Literary and Artistic Works;

- Convention Establishing the World Intellectual Property Organization (WIPO);

- The Madrid Agreement Concerning the International Registration of Marks (Madrid Agreement, MMA) and Protocol to the Madrid Agreement;

- The Patent Cooperation Treaty (PCT);

- Paris Convention for the Protection of Industrial Property;

- Geneva Convention for the Protection of Producers of Phonograms Against Unauthorized Duplication of their Phonograms

- Rome Convention for the Protection of Performers, Producers of Phonograms and Broadcasting Organizations;

- Trademark Law Treaty.

Main Categories of IP rights

Trade Marks

A trademark is a distinctive sign that identifies certain goods or services produced or provided by an individual or a company. Its origin dates back to ancient times when craftsmen reproduced their signatures, or “marks”, on their artistic works or products of a functional or practical nature. Over the years, these marks have evolved into today’s system of trademark registration and protection.

The registration and protection of marks in relation to goods and services is governed by the Trade Marks Law, Cap 268, as amended by Laws 63/62, 69/71, 206/90 and 176(I)/2000 and by the Regulations of 1951-1992 as amended.

Copyright and Related Rights

Copyright laws grant authors, artists and other creators protection for their literary and artistic creations, generally referred to as “works”. A closely associated field is “related rights” or rights related to copyright that encompass rights similar or identical to those of copyright, although sometimes more limited and of shorter duration. The beneficiaries of related rights are:

- Performers (such as actors and musicians) in their performances;

- Producers of phonograms (for example, compact discs) in their sound recordings;

- Broadcasting organizations in their radio and television programs.

Works covered by copyright include, but are not limited to: novels, poems, plays, reference works, newspapers, advertisements, computer programs, databases, films, musical compositions, choreography, paintings, drawings, photographs, sculpture, architecture, maps and technical drawings.

The applicable legislation in Cyprus regarding copyright is the Copyright and Neighboring Rights Law of 1976 (Cap 59), as amended by Laws 63/77, 18 (I)/1993, 54 (I)/1999, 12 (I)/2001, 128(I)/2002 and 128(I)/2004.

Rights are recognized for every protected object whose beneficiary is at the time of the creation of the right, or if it is a broadcast, the time of the transmission of the broadcast, a qualifying person, namely:

- A person who is a citizen of the Republic of Cyprus or who habitually resides in the Republic;

- A legal person, established in accordance with the laws of the Republic;

- Or a citizen of another member state of the European Union.

Patents

A patent is an exclusive right granted for an invention – a product or process that provides a new way of doing something, or that offers a new technical solution to a problem.

In Cyprus, the registration and protection of patents is regulated by the Patents Law 16(I)/98, as amended by Laws 21(I)/99, 153(I)/2000 and 163(I)/2002 and by the relevant Patent Regulations of 1999 and 2000.

The new Intellectual Property tax regime in Cyprus

Amendments made to the Income Tax Law (Article 9 (e) – Law 102 (I) 2012) in May 2012 have turned Cyprus into one of the favorable jurisdictions for royalty and holding structures.

Below are the main points of the new IP regime:

1. Notional deduction of 80% from the profit arising from IP owned by Cyprus resident companies.

Profit = Income from IP – Direct IP Expenses

Income from IP:

- Royalties

- Gains from the disposal of an IP

- Compensation received for an illegal use of an IP

Direct IP expenses:

- Finance cost to acquire/develop IP

- Exchange differences related to IP acquisition/development

- Tax amortization

- Other direct expenses (training, commissions etc.)

2. Five year amortization period. The cost of acquisition or development of an IP right may be capitalized and amortized on a straight line basis over five years, giving an annual writing down allowance of 20%.

3. All the above exemptions are also available for IP acquired or developed before 1st January 2012.

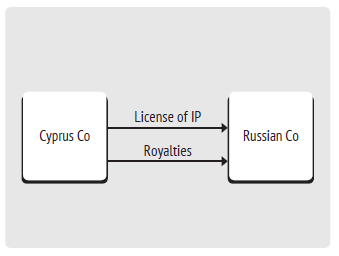

Example 1

Taxation of Royalty Income

A Cyprus tax resident company derives royalty income amounting to €100.000 from a Russian company and incurs direct IP expenses of €60.000. Under the Cyprus IP tax regime the royalty income will be taxed as follows:

Tax computation:

Income from royalties: 100.000

Direct Expenses: (60.000)

Net Income: 40.000

80% notional deduction (40.000*80%)(32.000)

Taxable Income: 8.000

Income tax: (8.000*12.5%) 1.000

VAT

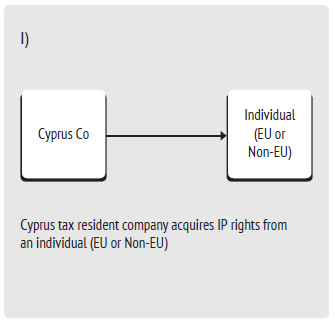

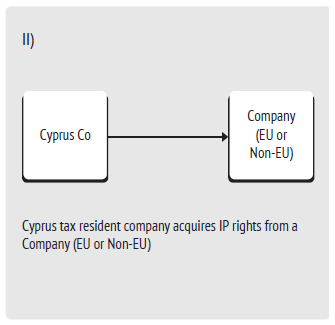

Acquisition of IP rights

In both cases I and II the acquisition of IP rights by the Cyprus Company is treated as a service that is rendered to the Company which will create an obligation for it to be registered for VAT (applying the reverse charge principle).

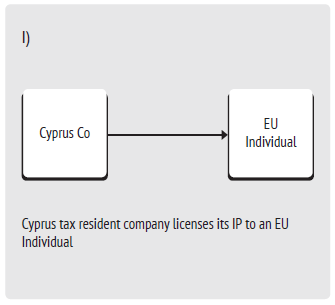

License of IP rights

The Cyprus Company has to be registered for VAT and charge Cyprus VAT on its invoices issued to the EU Individual.

Such supply of services is outside the scope of VAT in Cyprus (the EU Company must be registered with the VAT authorities in any other Member State). Although, the Cyprus Company has to get registered with the VAT authorities in Cyprus and submit the VIES (VAT Information Exchange System) statement on a monthly basis.

In both cases III and IV the licensing by Cyprus Company of its IP outside the EU countries does not fall within the scope of VAT purposes in Cyprus. In such a case, the Cyprus Company does not have any obligation to be registered with the VAT authorities or to charge VAT in Cyprus.

In the past two decades Cyprus has been and is still promoted as a leading Intellectual Property (IP) holding jurisdiction following the introduction of a favorable tax regime in relation to income generated from any type of IP. The new IP scheme provides a very attractive legal and financial framework for the appropriate exploitation of IP assets.

The aforesaid in additional to a high standard professional services, to the favorable double tax treaties (e.g. Double tax treaty with Russia: 0% withholding tax on royalties) and to its geographical position have transformed the jurisdiction of Cyprus into an ideal location to establish an IP structure.

Other Articles on Topics