CONTENTS OF LAST ISSUE

Amendments to double taxation conventions. Process is set in motion

Not so long ago, changing terms of international taxation became a priority. The main objective is to prevent income siphoning to low-tax or tax-free jurisdictions by increasing the withholding tax rate in the Russian Federation.

If a party to the double taxation convention (hereinafter, DTC) accepts the terms proposed by the Russian Federation, the withholding tax rate at the source of dividends and interest income will increase up to 15%, otherwise the convention will be terminated, which will result in the inability to offset tax paid in one jurisdiction by another jurisdiction, and will lead to double taxation of international income.

Despite the fact that for DTC terms regarding royalties no amendments are planned, there is still a possibility of DTC termination, and in this case, instead of the reduced rate at the source and the possibility of setoff, a taxpayer will have to pay the withholding tax at the rate of 20% without a possibility to offset the tax amount.

Moreover, one of the consequences of DTC termination will be the absence of necessity to confirm the actual income recipient.

Currently, amendment letters have been sent to the following jurisdictions:

- Cyprus

- Luxembourg

- Malta

It is also highly likely that the said instruction will affect the following jurisdictions:

- the Netherlands

- Switzerland

- Ireland

If a written notice of termination of the Russian DTC is sent, changes will affect taxpayers no earlier than January 1, 2021. And in case of most jurisdictions, the Russian Federation should have sent such a notice by July 1, 2020, otherwise treaties will be deemed terminated only from January 1, 2022.

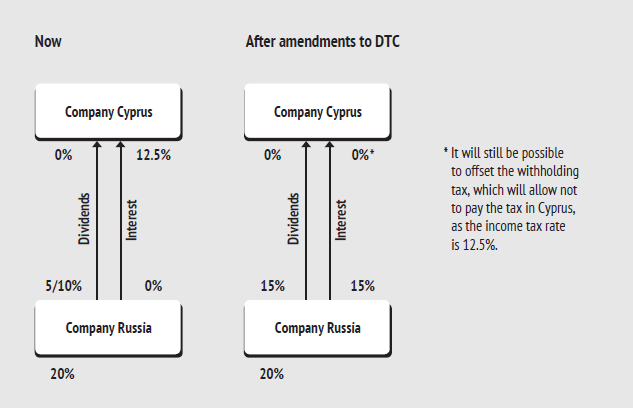

The parties were able to reach agreement on the DTC between the Russian Federation and the Republic of Cyprus, and they started the process of amending the convention.

Diagrams below show the consequences:

The following are options for consideration in this situation:

- Leave as is

This option is worth considering if a Cyprus company was created for purposes other than tax saving and/or tax saving is not a priority. Such a company could be created to protect assets, exploit peculiarities of the local legal system (e.g. the trust institution), and advantages that facilitate the process of attracting investors and/or making capital transactions. In such companies, the cash flow from assets in Russia is often minimal.

- Apply a “pass-through” approach

This option suggests that the company ceases to recognize itself as an actual income recipient and, consequently, a tax agent at the source of income no longer applies the terms of the DTC with Cyprus, but rather the terms with an actual income recipient. One of the advantages of this option is cost reduction of creating and/or maintaining an actual income recipient status for a Cyprus company.

- Terminate payment settlements

In case there are pending settlements between a Russian company and a Cyprus company in the current year, namely accrued interest, retained earnings, and accrued royalties.

- Move to another place

Other jurisdictions may be worth considering. Currently, jurisdictions that provide comparable benefits (taking into account DTC and national legislation) are Luxembourg, Malta, and the Netherlands. However, when choosing a jurisdiction, one should keep in mind that the Ministry of Finance of the Russian Federation has already sent letters with a proposal to amend the DTC to Luxembourg and Malta. It is also highly likely that changes will affect the DTCs with the Netherlands, Switzerland, and Ireland. In addition to DTC provisions, one should consider such factors as the absence of the withholding tax and low tax burden on passive income when choosing a jurisdiction. In this situation, it is worth considering a comprehensive approach, particularly, moving to a jurisdiction with the territorial principle of taxation (e.g. Hong Kong or Singapore) and applying a “pass-through” approach.

In addition, given the fact that the use of tax incentives becomes more and more complicated not only in Russia, but also worldwide, it seems reasonable to evaluate other benefits of jurisdictions not directly related to tax planning when moving to a different place, for example:

- Quality of the company administration;

- Cost of creating (moving) and maintenance of the company;

- Mechanisms for protecting rights of shareholders (e.g. obligatory registration of the transfer of ownership to shares in the state register);

- Possibility of obtaining tax residence, residence permit or passport through an investment in such a company;

- Reputation of the jurisdiction for AML regulatory and compliance purposes.

During such a transition period, it is recommended to take an inventory of the existing structure, evaluate all advantages and risks, benefits and costs, take into account non-monetary factors that may be significant, and perform one of the actions above, namely:

- Make payments that are able to be made;

- Evaluate the possibility of applying a “pass-through” approach to taxation;

- Evaluate the possibility of replacing a foreign company taking into account the indicated tendency to the DTC termination/amendment;

- Leave everything as is, if the DTC termination/amendment has no significant effect on the tax burden or obtaining tax savings is not the main purpose of creating a foreign structure.

At the same time, it is important to understand and remember that in this situation there is no common and multi-purpose solution. Despite the fact that all are now caught in the same storm, everyone keeps sailing their own boat, and the resolution to restructure will only be right if it takes into account specific goals and objectives of the beneficiary of the structure.

Other Articles on Topics