СОДЕРЖАНИЕ ПОСЛЕДНЕГО ВЫПУСКА

Является ли Гонконг благоприятным местом для открытия бизнеса в Азии?

В настоящее время Гонконгу удалось достичь невероятных результатов в экономической и социальной сфере благодаря высокой конкурентоспособности рабочей силы, удобному географическому расположению и, что более важно, свободной экономике.

Гонконг, который в начале XIX века представлял собой рыбацкую деревню, расположенную на незаселенной территории, со временем превратился в один из наиболее важных мировых финансовых центров с населением 7 млн. человек. Но прежде Гонконгу пришлось пройти несколько этапов становления.

История Гонконга (1842-1949 гг.)

Часть Гонконга, именуемая остров Гонконг, с общим населением 8 тыс. человек была передана англичанам на основании Нанкинского договора в 1842 г. В 1898 г. весь Гонконг перешел в руки англичанам сроком на 99 лет.

Впоследствии Гонконг пострадал от трагических событий, имевших место в ходе войны на территории Китая. Свержение династической китайской системы в 1911 г., Великая депрессия и колебания цен на серебро оказали сильнейшее негативное влияние на стабильность внутри страны, равно как и на отношения Китая с внешним миром. Начиная с 1937 г. Китай был вовлечен в Японо-китайскую и гражданскую войну, что вызвало дальнейшее падение китайской экономики.

В течение указанного периода состоятельные предприниматели и предприятия переключили внимание с Китая на Гонконг вследствие неопределенного будущего Китая, что вызвало быстрое развитие коммерческих предприятий и рост капиталовложений в Гонконг. Так как на тот момент Гонконг являлся британской колонией, для приезжих он представлял собой относительно более благоприятное место с точки зрения безопасности и стабильности.

Индустриализация Гонконга (1949-1978 гг.)

После создания Китайской Народной Республики (КНР) в 1949 г. государство начало процесс изоляции от глобальной экономики по идеологическим причинам, сформулированным находящимся у власти лидером – Председателем Мао Цзэдуном, а также по причине введения ООН эмбарго в 1951 г. В течение указанного периода экономика Гонконга стремительно развивалась благодаря содействию состоятельных предпринимателей, притоку рабочей силы и капитала с севера страны. В 1950х гг. производство текстильных изделий было ведущей отраслью промышленности Гонконга; с течением времени в 1960х гг., на его базе сформировались другие отрасли, например, производство радиоэлектронной аппаратуры, одежды, изделий из пластмассы и иных трудоемких товаров для дальнейшего экспорта.

Правительство не вмешивалось в рыночную ситуацию и поддерживало развитие в рамках свободного рынка, так как было сосредоточено на проектах застройки и строительной инфраструктуре, пытаясь справиться со стремительным ростом населения. Гонконг по сравнению с иными развитыми азиатскими государствами, такими как Япония, Тайвань, Южная Корея или Сингапур, отличается уникальными результатами в сфере экономического развития. Низкие налоги, размытое трудовое законодательство, отсутствие государственного долга и возможность свободной торговли явились столпами экономического развития Гонконга.

Хотя за свою историю Гонконгу пришлось пережить некоторые потрясения, как, например, мировой нефтяной кризис и Культурную революцию в Китае, имевшие место в конце 1960-х и 1970-х гг., ему удалось сохранить положительные темпы роста ВВП в среднем на уровне 6,5% в год.

Политика открытых дверей в Китае 1978 г.: мировая фабрика

В 1978 г. китайский политический лидер Дэн Сяопин объявил начало реализации Политики открытых дверей. Главной целью являлось привлечение в Китай иностранных инвестиций. Китай создал Особые экономические зоны в дельте реки Чжуцзян (Жемчужная), в пределах которых иностранные предприятия могли строить свои заводы. Такая инициатива была с энтузиазмом одобрена предпринимателями по всему миру, так как Китай мог предложить дешевую рабочую силу и низкий уровень иных издержек.

В результате такой политики заводы, находившиеся на территории Гонконга, были переведены обратно в Китай в целях снижения затрат. Данный момент стал поворотным с точки зрения экономического статуса Гонконга, которому пришлось уйти от промышленной экономики для того, чтобы выжить. После объявления Китая о начале реализации Политики открытых дверей Гонконг пережил резкий рост спроса на коммерческие и финансовые услуги.

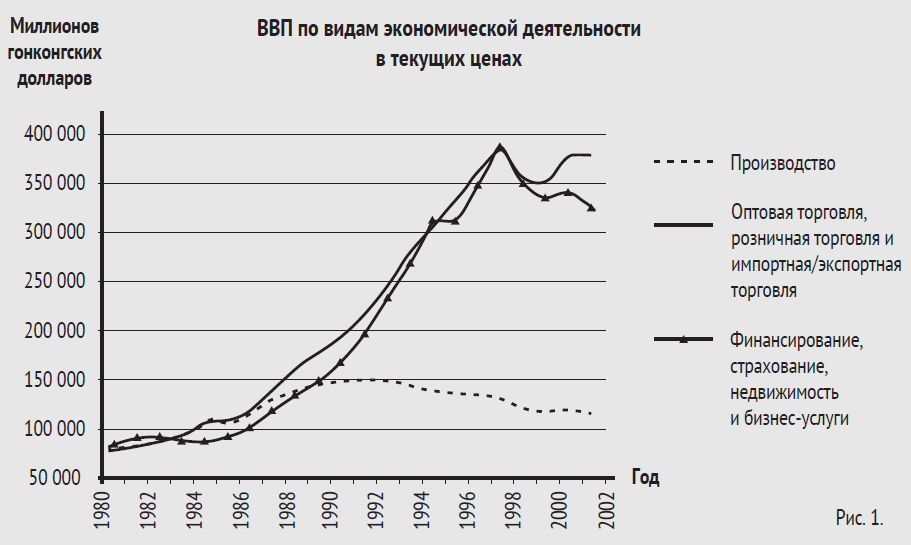

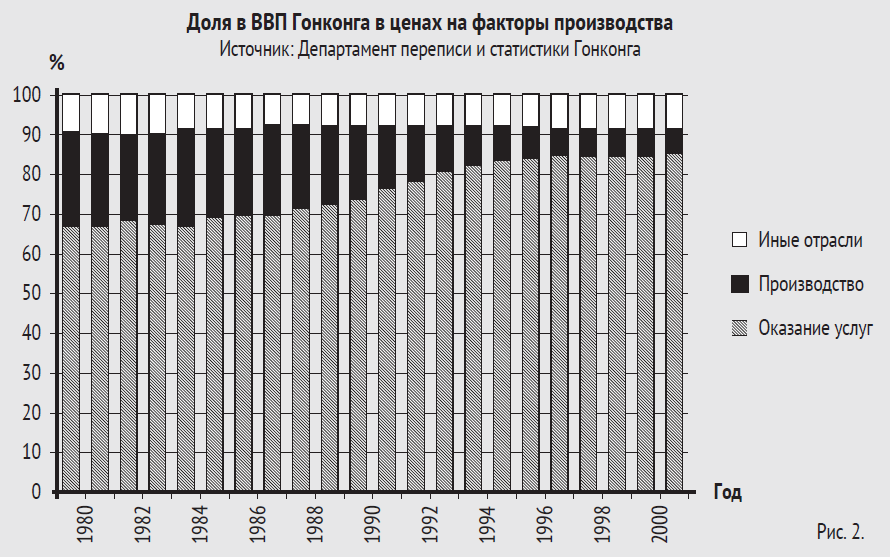

Как видно на Рис. 1 промышленность переживала устойчивый спад, в то время как финансовый сектор и сектор обслуживания процветали. Экономика Гонконга трансформировалась в экономику с развитым сектором услуг.

Согласно исследованию, проведенному Департаментом переписи и статистики Гонконга, доля сектора оказания услуг в ВВП Гонконга составила более 90%.

Передача Гонконга – история с 1997 г. до наших дней

1 июля 1997 г. Великобритания передала Гонконг Китаю. Гонконг получил право разработать собственное законодательство и политический курс, находясь под надзором Китая. С тех пор действует политика «Одно государство – две системы». Преимущество данной политики заключается в том, что Гонконгу удалось сохранить колониальное размытое трудовое законодательство, низкие налоги и возможность свободной торговли, но в то же время остаться своеобразным плацдармом для достижения целей Китая.

Вследствие растущего значения Гонконга в качестве экономики, основанной на оказании профессиональных услуг, многие иностранные компании приняли решение открыть офисы в Гонконге, а не в Китае, в связи с существующими рисками, уровнем квалификации рабочей силы и простой системой налогообложения Гонконга. Кроме того, Гонконг является портом свободной торговли, облагающим налогами только табачные изделия, жидкие нефтепродукты, алкогольные напитки и метиловый спирт. За исключением вышеперечисленного, все товары, ввозимые в Гонконг или вывозимые из него, не облагаются налогом. Налог на прибыль в Гонконге составляет 16,5%. Однако, если компания, зарегистрированная в Гонконге, получает прибыль исключительно от операций за пределами Гонконга, налог составляет 0%.

Почему следует размещать бизнес в Гонконге, а не в Китае?

У вас может возникнуть вопрос: почему бы не разместить свою компанию непосредственно на территории Китая, а не вблизи него?

Согласно Докладу о мировых инвестициях, опубликованному в 2009 г. Конференцией ООН по торговле и развитию (ЮНКТАД), Гонконг является основным направлением прямых иностранных инвестиций (ПИИ). В 2008 г. сумма иностранных капиталовложений в Гонконг составила 68 млрд. долларов США. Гонконг сохраняет за собой статус крупнейшего получателя ПИИ, занимая второе место среди азиатских государств и седьмое место в мире.

На протяжении более чем десяти лет Гонконг удерживал звание территории с «самой свободной экономикой в мире», согласно данным Фонда «Наследие» (Hertitage Foundation), «Wall Street Journal» и Института Фрейзера (Fraser Institute). Неудивительно, что многие международные компании выбирают Гонконг в качестве места расположения своих региональных штаб-квартир в Азии. Отсутствие торговых ограничений, низкий уровень вмешательства со стороны государства, а также расширение и стимулирование развития сектора оказания услуг укрепили позиции Гонконга.

Структура налогообложения Гонконга относительно проста – государство взимает налог на прибыль на территориальной основе. Это значит, что обычно в Гонконге налог взимается только с прибыли, полученной в его государственных границах. Существует три основных вида налога: налог на прибыль, налог на заработную плату и налог на недвижимое имущество. Любая иная прибыль налогом не облагается. На территории Гонконга не взимаются налог с фонда оплаты труда, налог с оборота, налог с продаж, НДС, налог на дивиденды, налог у источника выплат и налог на доход от прироста капитала.

Рост привлекательности Гонконга основан на политической стабильности, управлении, ориентированном на интересы деловых кругов, верховенстве права и независимой от Китая правовой системе, свободном обмене информацией. Английский и китайский языки являются основными языками общения в деловых кругах.

Гонконг представляет собой естественные ворота в Китай вследствие своего географического расположения и наличия благоприятной деловой, финансовой и правовой системы. Потому неудивительно, что компания, учрежденная в Гонконге, является наиболее распространенным типом юридического лица, существующего в качестве материнской компании для предприятий, входящих на китайский рынок.

Торговля с компанией, учрежденной в Гонконге

Сотрудничество с гонконгской компанией открывает возможность прямой работы из Гонконга с клиентами по всему миру без необходимости открывать штаб-квартиры на местах и хранить товары на складах. В результате Азия предлагает более низкие цены на условиях франко-борт. Кроме того, отсутствует необходимость оформления банковского кредита, так как клиенты могут оформить переводной аккредитив. Такие условия освобождают капитал и стимулируют движение потоков денежных средств. И что более важно – можно вести коммерческую деятельность с минимальными затратами.

Требования к бухгалтерскому учету и налоговым декларациям

Гонконгская компания обязана ежегодно подавать аудиторские отчеты и налоговые декларации, вследствие чего рекомендуется вести бухгалтерский учет в соответствии со стандартами Гонконга. Стандартная ставка налога на прибыль – 16,5%. Однако если компания ведет деятельность исключительно за пределами Гонконга и может доказать это Налоговому управлению Гонконга, она вправе запросить разрешение платить налог по ставке 0%. Для подтверждения статуса компании, осуществляющей деятельность за пределами Гонконга, компания должна соответствовать следующим требованиям:

- не иметь сотрудников на территории Гонконга;

- не выставлять счета другим гонконгским компаниям и не получать от них счета;

- поставки должны осуществляться за пределами Гонконга.

Срок одобрения налоговой льготы зависит от прибыли, полученной компанией в течение соответствующего налогового года; часто переговоры по данному вопросу затягиваются на длительный период.

В целях сокращения финансовых и административных издержек поставщики услуг, такие как компания «Корпус Права», разработали для организаций экономически эффективные решения по привлечению сторонних ресурсов. Вам не нужно арендовать офис в Гонконге или нанимать персонал. Вы можете начать предпринимательскую деятельность, учредив компанию с ограниченной ответственностью в Гонконге и открыв банковский счет. Обладая развитой экономикой, конкурентоспособными сотрудниками, говорящими на английском и китайском языках, пользуясь преимуществом минимального вмешательства со стороны государства, Гонконг, без сомнений, является наиболее выгодной территорией для открытия бизнеса.

Другие статьи по темам