CONTENTS OF LAST ISSUE

IFRS 9 — new approach to classification and impairment of financial assets

In preparation of financial statements in accordance with IFRS (International Financial Reporting Standards) for 2018, all companies faced with a new financial instrument accounting standard IFRS 9.

Financial instruments have traditionally raised the greatest number of questions and presented many challenges.

IFRS 9 mandatory for use since January 01, 2018, was intended to eliminate the shortcomings of then applicable IAS 39, simplify the logic of classification of financial instruments, increase the reliability of information about impairment of financial assets. However, it has raised even more questions.

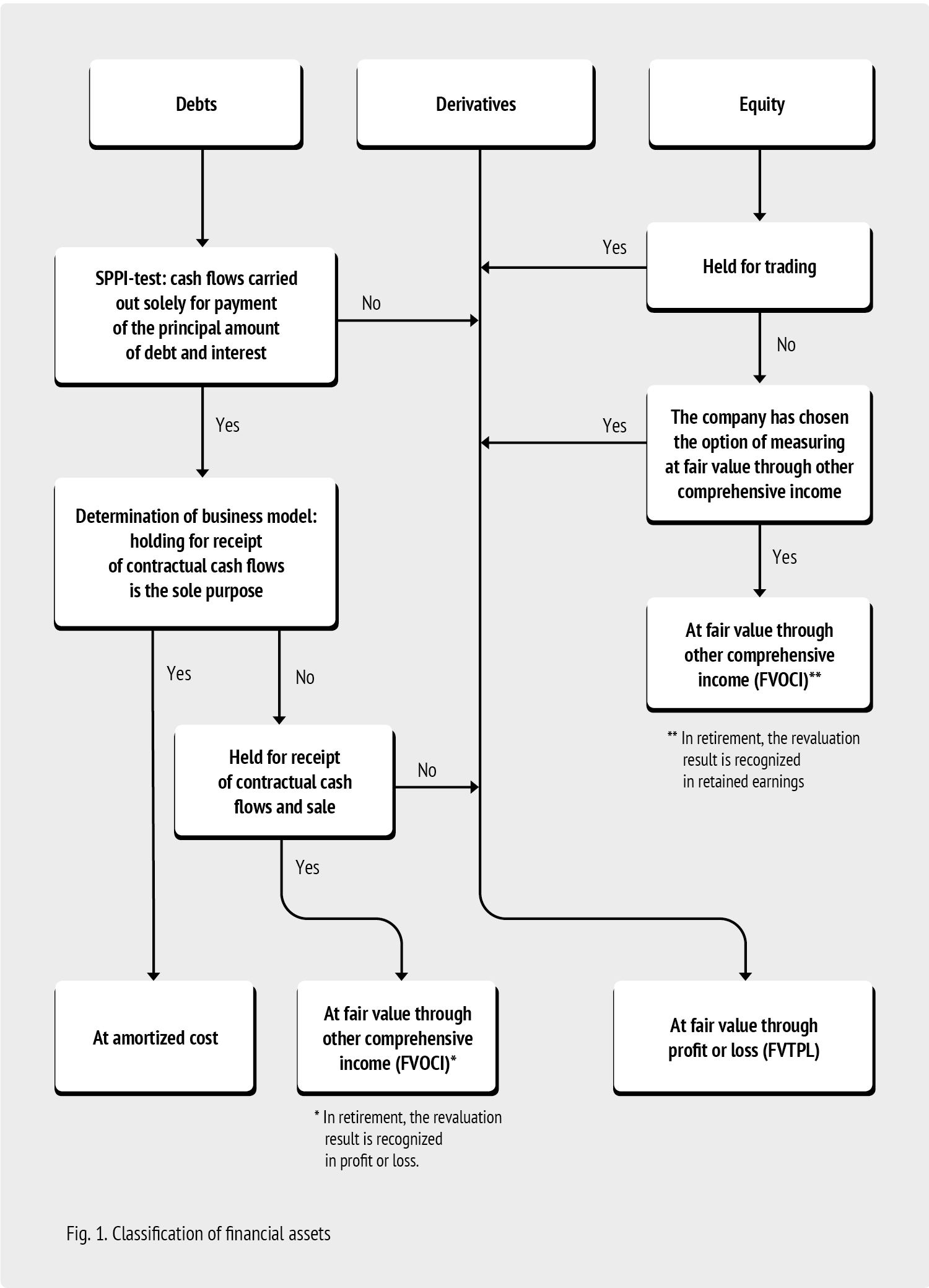

Key changes have occurred in the classification and measurement of financial assets and even more, significant changes concern asset impairment.

From now on, financial assets are divided into three groups, depending on the method of their measurement and accounting:

- FVTPL: fair value through profit and loss;

- FVOCI: fair value through other comprehensive income;

- AMC: amortized cost.

The principles that the company applies when referring an asset to a particular group are shown in figure 1.

Already after the first year of application, an amendment to IFRS 9 appeared which became effective on January 01, 2019. According to this amendment, loans and borrowings with the early repayment option in the agreement cannot be classified at amortized cost, that is, they should be measured at fair value.

However, companies face the biggest difficulty in applying new rules of impairment of financial assets.

First, impairment applies to virtually all companies, even those that do not include securities, equity or derivative financial instruments in their financial statements. After all, the receivables of a trading company are also a financial instrument.

Provision for impairment should be created for all financial assets, except for those carried at fair value through profit or loss as changes in their fair value reflect their impairment. The provision is created as of each reporting date and is a cumulative value. An increase or decrease in the provision is recognized in profit or loss. And the provision itself reduces the amount of financial assets in the statements.

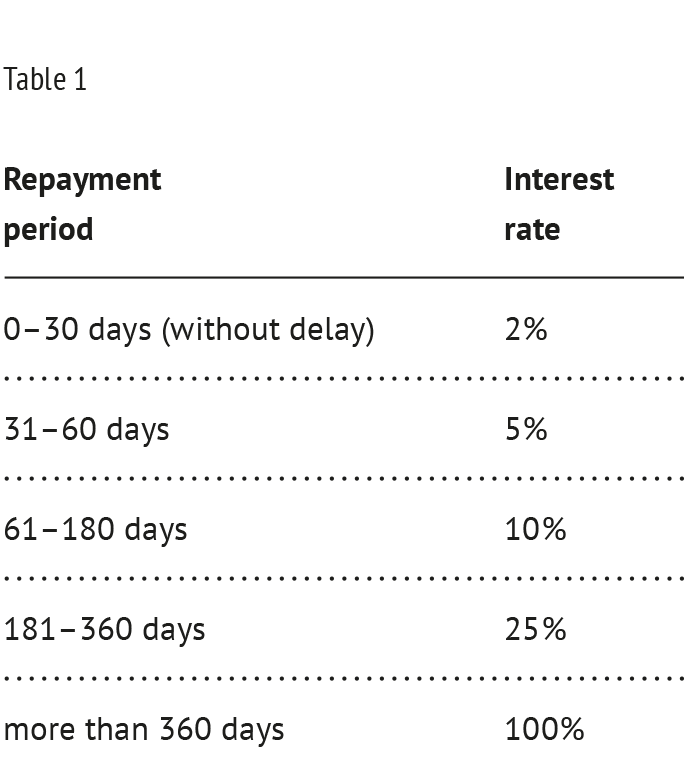

Second, the model of losses incurred has been replaced by the ECL model: expected credit loss. What does this mean in practice?

Previously: receivables were generally grouped by maturity, and interest was applied to them which depended on the period of delay in debt repayment (the longer the period of delay, the bigger the interest) based largely on historical information. Or the provision was not created at all. Example (table 1).

Currently: impairment of financial assets should be recognized in the amount of expected credit loss (ECL). Now companies must take into account not only historical information but also perspective information.

Credit loss is the value of cash flows for a financial instrument, that will not be received, which was discounted at the reporting date. IFRS 9 stipulates two approaches to determination of ECL: general and simplified (see figure 2).

![]()

According to the general approach, the impairment loss is recognized depending on the stage at which the financial asset currently is. It is important to note that income is accrued on a financial asset (for example, loan interest) to its full value, excluding the provision for financial assets with regular credit risk or assets showing signs of a significant increase in credit risk. Income on a defaulted financial asset is accrued to its cost in view of the provision.

The text of the standard contains refutable assumptions that:

- Credit risk on a financial asset has significantly increased if the payments stipulated by the agreement are in arrears for more than 30 days (clause 5.5.11); and

- Default occurs on or before the date when the financial asset is in arrears for 90 days unless the organization has reasonable information to apply larger arrears in the payment (clause В5.5.37).

Simplifications have been developed for certain types of receivables. The simplified approach is stipulated for:

- Trade receivables without a significant financing component (that is, payment deadlines do not grant significant benefit from financing the transfer of goods or services for the buyer);

- Lease receivables;

- Assets under contracts without a significant financing component (the company’s right to receive compensation for goods/services that have already been transferred/rendered to the buyer but payment for them depends on the occurrence of a certain event that is not associated with time).

To understand what companies are now dealing with, we will consider fundamental steps of calculating the estimated provision for credit loss using the simplified approach.

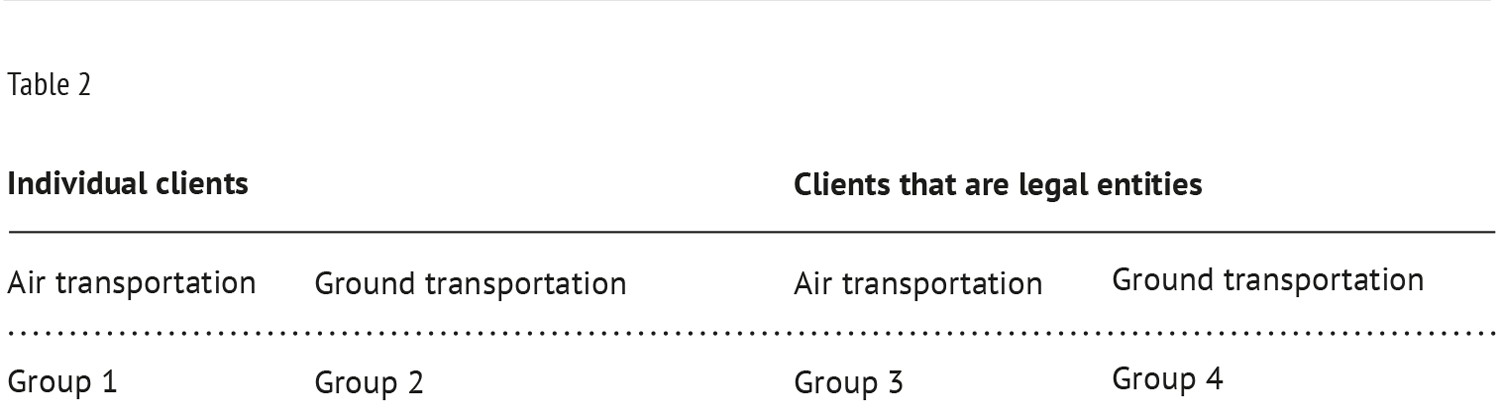

Example: Company 1 which principal activities are cargo transportation. The company’s policy grants a delay of 30 days for its customers to repay their receivables and according to it, the debt is deemed defaulted if it is not repaid within 360 days. As of December 31, 2018, the company has total receivables for air transportation of goods from individuals in the amount of 7,500,000 Rubles. Let us calculate the provision that the company should accrue on this debt by 31.12.2018.

Grouping of receivables with similar credit risk features

The standard does not contain clear instructions as to how to group receivables. Companies themselves should determine the most important criteria which affect credit risk. For a transport company, those may be the geographical region of customers, type of customers (individuals or legal entities), type of cargo transportation (domestic or international, air or rail…), type of goods transported, whether the transportation is carried out by the company itself or through contractors, etc.

As to Company 1, it was resolved to divide the debt into 4 groups (there may be more groups) (table 2):

To determine the expected credit loss by the total amount of the debt, the company should determine them for each group separately and sum them up. But for clarity, let us consider Group 1 only.

Determination of credit loss ratios for the prior period

The prior period should be reasonable and most appropriate, not too short or too long. In practice, it is usually not less than a year and not more than five years.

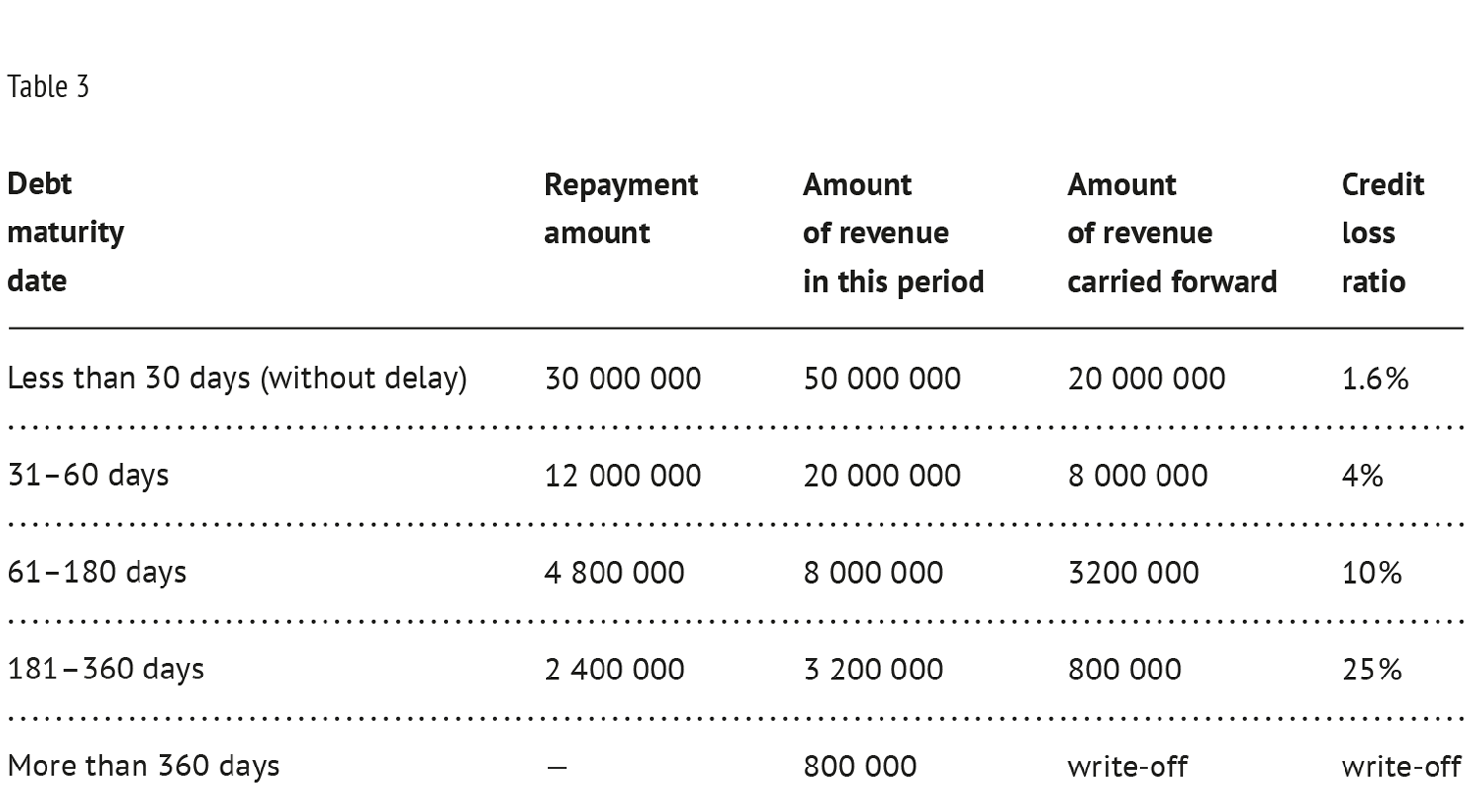

The ratios should be determined for each group separately. To do this, we break down the total receivables in accordance with the maturity dates and determine the amount in each period of delay.

Total sales in 2018 for Group 1 were 50,000,000 Rubles. Total credit loss for Group 1 was 800,000 Rubles. The debt was repaid as follows (table 3).

Credit loss ratios are calculated by dividing the total amount of credit losses of 800,000 Rubles by the amount of revenue (debt) in each period.

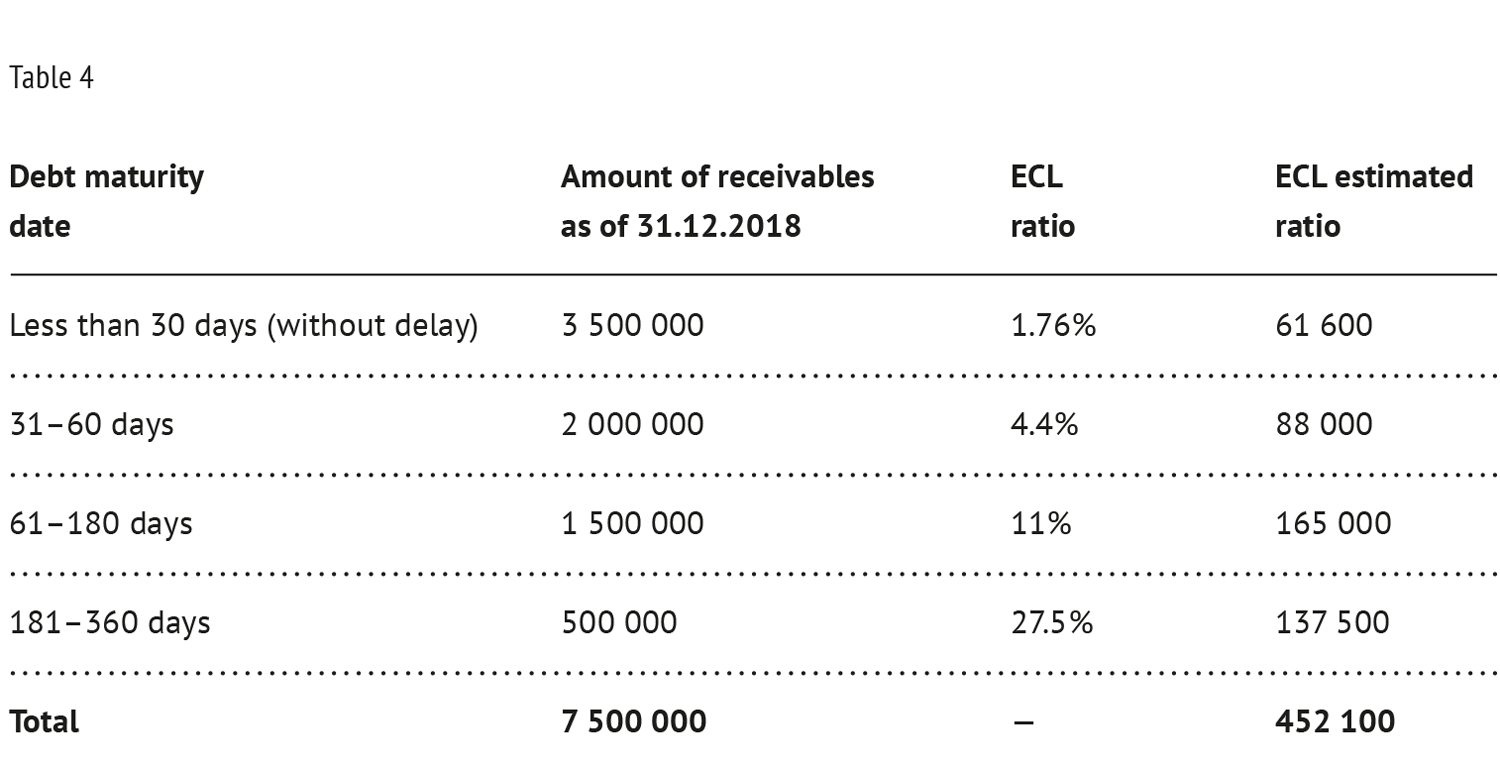

Determination of future expected credit loss ratios

The most difficult and contentious issue is the determination of the impact of future economic conditions on credit loss. These ratios are largely based on professional judgment and analysis.

Let us perform this step for illustration purposes only. And let us assume that Company 1 expects an increase in credit loss in the amount of 10% due to rising fuel prices. Each company individually determines which indicators affect credit risks (exchange rates, rising unemployment, inflation, etc.).

In this case, historical credit loss ratios calculated in the previous clause increase by 10%, and as of December 31, 2018, the provision is 452,100 Rubles (table 4).

The new approach to impairment of financial assets further bridges the gap between financial statements in accordance with IFRS and management statements. IFRS 9 largely makes it possible to use a specialist’s professional judgment. The need to rely on substantiated and verifiable information available without undue cost or effort is repeatedly stressed in the text of the standard.

But auditors acknowledge that in some cases, companies willingly agree to a reservation in auditor’s opinion since the calculation of the loss allowance on a financial instrument under the new rules is overly complicated. The auditors often have difficulties due to the inability to confirm professional judgments used to estimate expected credit losses.

In general, it is difficult to dispute the fact that the application of the IFRS 9 rules hurt companies noticeably. Calculation of impairment of financial assets sometimes simply goes beyond the capabilities of accountants, requires the involvement of specialists from other departments (financial managers, analysts), significant costs for modernization of the accounting system. Let alone the fact that it takes a lot of time and leads to an increase in losses for companies. This is especially important to understand for users of reporting and business owners.

Other Articles on Topics