CONTENTS OF LAST ISSUE

Amendments to provisions governing liability for violations of the currency legislation of the Russian Federation

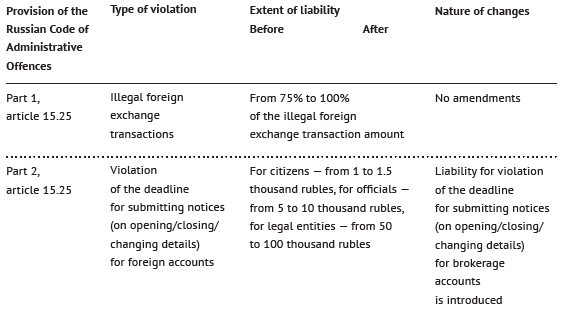

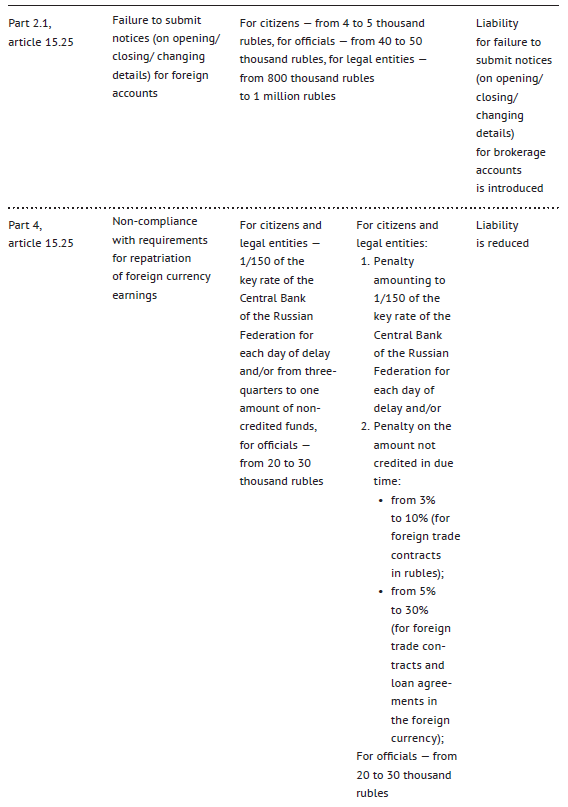

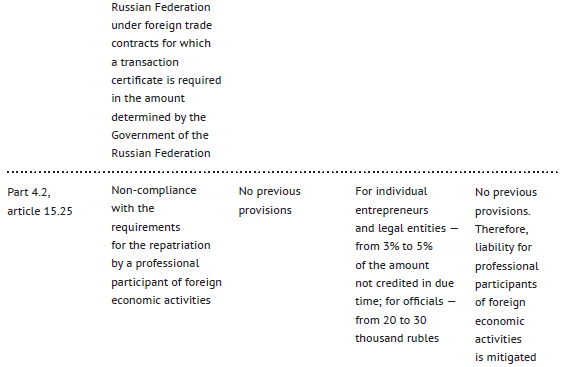

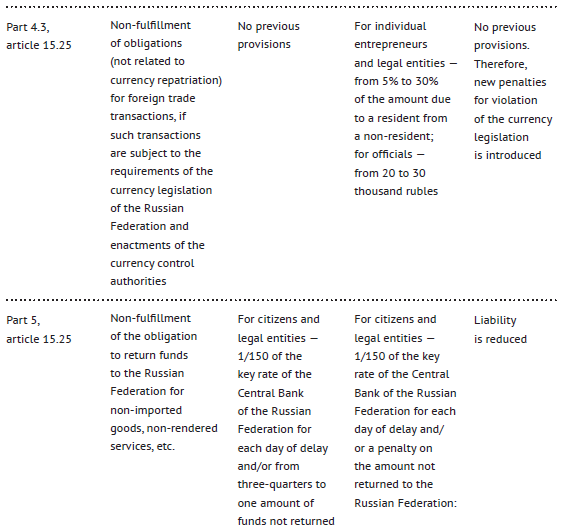

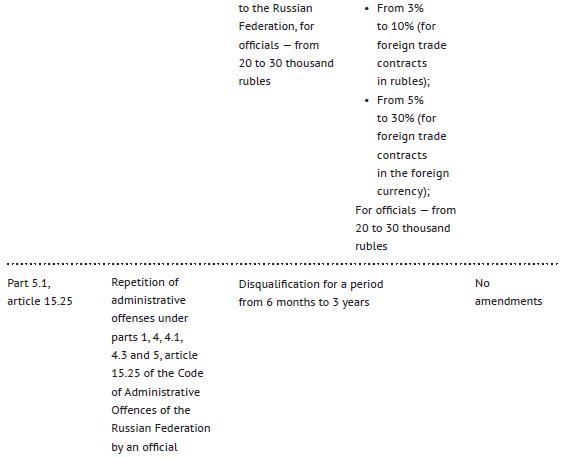

From July 31, 2020, Federal Law No. 218-ФЗ “On Amendments to Articles 3.5 and 15.25 of the Code of Administrative Offences of the Russian Federation” dated 20.07.2020 became effective and amended provisions governing liability for violations of the currency legislation.

In some cases, liability for violations of the currency legislation was mitigated (and even abolished), while in some cases additional grounds and penalties were introduced.

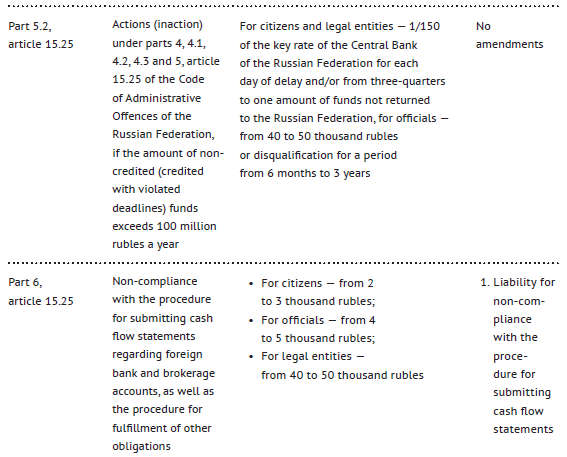

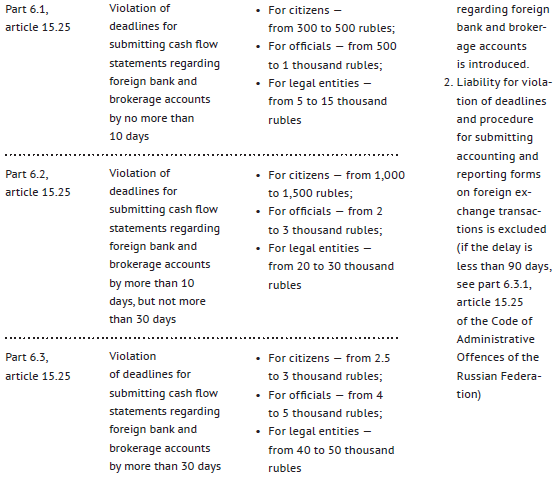

For greater clarity, the table below contains information on all types of liability set for violations of the legislation on currency regulation and currency control:

It is also worth noting that the new law includes the following grounds for exemption from liability for violations of the currency legislation:

- A resident may be released from administrative liability for illegal foreign exchange transactions with a foreign account (part 1, article 15.25 of the Code of Administrative Offences of the Russian Federation) and non-compliance with requirements for repatriation (part 4, article 15.25 of the Code of Administrative Offences of the Russian Federation) when funds are credited to a foreign account bypassing a Russian account, provided that if within 45 days from the date of crediting funds to a foreign account they are transferred to an account in the authorized bank.

- There is no administrative liability for non-compliance with requirements for repatriation (part 4, article 15.25 of the Code of Administrative Offences of the Russian Federation) if the amount of obligations does not exceed 200 thousand rubles.

- Administrative liability established by parts 4 – 4.3, 5, 5.2 and 5.3, article 15.25 of the Code of Administrative Offences of the Russian Federation applies only upon the expiration of forty-five days after the expiration of the term for fulfilment of the relevant obligation in case of its non-fulfilment within the specified period.

Therefore, such amendments may be generally evaluated as positive. But notwithstanding the above, the scope of liability for certain types of violations of the currency legislation remains relatively high (from 75% to 100% of the transaction amount). In this regard, foreign currency residents of the Russian Federation still need to be careful when performing foreign exchange transactions, using foreign accounts, and entering into legal relations with currency non-residents of the Russian Federation.

Other Articles on Topics