СОДЕРЖАНИЕ ПОСЛЕДНЕГО ВЫПУСКА

Проблемы регулирования криптовалют в России

10 лет назад Сатоси Никамото разместил статью «Биткоин: система одноранговых электронных денег». Теперь криптовалюты считаются одной из самых перспективных технологий. К сожалению, операции с криптовалютами в России до сих пор нормативно не урегулированы и более того – почти не изучены.

Частные деньги всегда были распространены, особенно их порождают войны, стихийные бедствия, экономические кризисы, борьба регионов за автономию (например, чеченский нахар и уральский франк в РФ).

В настоящем технологическом веке частные деньги получили «новую жизнь» благодаря системам онлайн-платежей (таким как PayPal, WebMoney, Яндекс.Деньги). Технологии позволили упростить эмиссию частных денег и расширить их оборот. Примерно в то же время стали появляться программы лояльности, которые предполагают эмиссию ограниченных в применении платежных средств: для авиаперевозок – мили, для платежных карт – баллы, также появился оборот игровых валют, которые могут конвертироваться в реальные деньги.

Распространение электронных денег вызвало опасения у правоохранительных органов, связанные со статусом площадок, которые осуществляют выпуск денег, с отсутствием контроля за объемами эмиссии частных денег. Стоит обратить внимание и на предрасположенность электронных денег к сбоям, а также на возможность снижения спроса к государственным деньгам.

В связи с этим начали предпринимать меры по сокращению вышеперечисленных рисков путем приравнивания электронных денег к платежным системам или банкам с идентификацией клиента, что привело к ограничению анонимных платежей, ограничению доступа юридических лиц к пользованию площадками электронных денег с целью избежать «утечки» частных денег в расчетную систему, ограничению полномочий площадок по управлению счетами пользователей.

Приравняв площадки частных денег к платежным системам, государство нивелировало бóльшее количество преимуществ частных денег. Например, платежная система, работающая в сети Интернет, может находиться в офшоре, но попытки создания такой независимой платежной системы были «прикрыты» действиями правоохранителей и финансовых регуляторов.

К 2000-м годам развитие Интернета позволило перейти к децентрализованным структурам, которые пришлись как нельзя кстати в условиях постоянного давления на Интернет извне. Децентрализованные сети дали развитие децентрализованным файлообменникам, анонимному даркнету. Так, применение децентрализованных сетей в финансовой сфере стало лишь вопросом времени. Децентрализованная платежная система оказалась эффективной, поскольку переводы через такую систему не нуждаются в посредниках, а значит, не могут быть ими отменены или изменены. Технология блокчейн (blockchain) решила проблему подделки информации о транзакциях – и это еще одно его преимущество.

Технологию блокчейн можно описать несколькими тезисами:

- децентрализованная база данных;

- управляется действиями участников, на нее почти невозможно оказать влияние извне;

- открыта и анонимна;

- нельзя подделать информацию, нельзя провести транзакцию за кого-то из участников;

- активные участники сети (майнеры) вознаграждаются комиссией за поддержание работоспособности сети.

Все эти преимущества обеспечили платформе огромный успех, а первой реализацией технологии стала криптовалюта биткоин (Bitcoin – от bit «бит» и coin «монета»). Впоследствии стали появляться альтернативные биткоину криптовалюты (альткоины), а вместе с ними новые децентрализованные платформы на базе блокчейна, такие как, например, Etherium.

Реакция государства на появление блокчейн-технологии и криптовалют в разные этапы развития технологии была разной:

- Отсутствие какой-либо реакции вначале, 2012-2013гг.

- Высказанные предостережения в сторону BitcoinFoundation после первого пика биткоина в 2013 году.

- Дискуссии о полном запрете в 2014-2016гг.

- Принято решение о легализации криптовалют, 2017г.

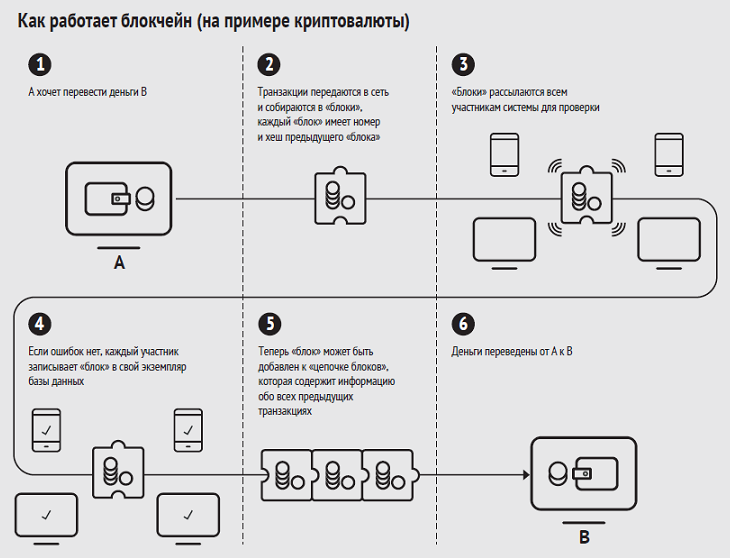

Ниже представлена таблица, наглядно демонстрирующая работу технологии блокчейн на примере криптовалюты:

На данный момент начались первые попытки легализовать технологию блокчейн в России. Так, один законопроект представил Минфин (над ним работал Анатолий Аксаков), он был внесен в Госдуму 20 марта 2018 года, первое чтение законопроекта еще не назначено. Законопроект предусматривает, что максимальную сумму вложения неквалифицированного инвестора в ICO будет определять ЦБ. На данный момент законопроект получил официальный положительный отзыв Правительства с уверенностью в том, что в 90% данный законопроект будет принят в первом чтении и именно он и станет отправной точкой в регулировании технологии блокчейн в России.

Второй законопроект представили тот же Анатолий Аксаков, Павел Крашенинников и Вячеслав Володин. Данный законопроект своей целью имеет внесение изменений в Гражданский кодекс РФ в части внесения терминов, связанных с блокчейном, а также определения токенов и криптовалют имуществом. Разработчики законопроекта детерминируют криптовалюту в качестве цифрового актива, который создается и учитывается в реестре в соответствии с алгоритмом. Обмен данных активов на валюту возможен, но пока порядок и условия таких сделок не определены. Предполагается, что их определит Правительство совместно с Центробанком.

Данный законопроект представляется также очень важным, поскольку поможет решить вопросы налогообложения криптовалюты, так как он предлагает рыночное регулирование криптовалют, в то время как проект Аксакова предлагает регулирование криптовалют под надзором Центробанка.

Оба законопроекта освещают только финансовую сторону, в то время как технология блокчейна способствует достижению максимальной прозрачности и точности в юридических сделках. Один из таких проектов на базе блокчейна тестирует Росреестр при регистрации сделок. Также блокчейн на данный момент тестируется в проекте «Активный гражданин» для учёта в ходе голосования жителей.

Одной из основных проблем регулирования криптовалют является налогообложение: предлагается как взимать с участников рынка процент, так и присваивать блокчейн-компаниям статус НКО. В том числе есть предложения по распространению патентной системы на майнеров. Однако, предлагаемое регулирование не соотносится с действующими законами. Если трактовать блокчейн в качестве информационной системы, то технология неизбежно подпадает под IT-законы, где регулирование довольно жесткое, следовательно, для развития технологии в РФ необходимо выводить понятие блокчейна из-под определения информационной системы.

Кроме того, существует проблема, связанная с ответственностью компаний и лиц за нарушения в сфере блокчейна, криптовалюты и незаконного предпринимательства. В законопроекте указано, что майнинг – это предпринимательская деятельность, ограниченная уровнем энергопотребления, но это не соответствует текущему Уголовному кодексу РФ. Таким образом, необходимо будет устранять данную проблему, иначе возникнет ситуация с введением нового вида предпринимательской деятельности, для которого не определены свои требования.

В Китае правительство проводит политику по регулированию блокчейна, по запрету криптовалют, поскольку по мнению китайского правительства криптовалюты служат средством по выводу денег из страны. Думается, что в случае полного запрета криптовалют в Китае китайские мощности перейдут в Россию, поскольку Россия является приоритетным регионом для китайских майнеров. Однако серьезным препятствием для перехода в Россию является правовая неопределенность относительно регулирования блокчейна и криптовалют. Стоит помнить, что перенос оборудования в РФ станет крупным инвестиционным вложением в экономику страны, но необходимо предоставить участникам комфортные условия налогообложения. Сейчас Китай в качестве альтернативного варианта рассматривает Канаду как страну с благоприятными условиями для майнеров. Складывается ситуация, аналогичная ситуации с офшорами, когда страны начинают борьбу за капитал, который может принести в страну криптовалюта. Для российской экономики, учитывая её упадок, крайне важно скорее ответить на вопрос – сможем ли мы принять участие в этой гонке, и если да, то успеем ли.

Другие статьи по темам