СОДЕРЖАНИЕ ПОСЛЕДНЕГО ВЫПУСКА

Желтый пес на хвосте принес!

Наступивший год принес нам много нового, особенно в части налогообложения. Изменения затронули очень многие главы Налогового кодекса РФ: Налог на прибыль организаций, НДФЛ, Упрощенная система налогообложения, Страховые взносы, Налог на имущество и многие другие.

В этой статье будет уделено внимание тем поправкам, которые относятся к большинству юридических и физических лиц в Российской Федерации.

Возвращение налога на движимое имущество

Глава 30 Налогового Кодекса РФ пополнилась статьей 381.1, согласно которой льгота по налогу на имущество организаций, применяемая для движимого имущества, приобретенного после 1 января 2013 года, будет действовать в 2018 году только в том случае, если такое решение будет принято на региональном уровне.

Также в статью 380 Налогового Кодекса РФ введен пункт 3.3, гласящий о том, что налоговые ставки, определяемые законами субъектов Российской Федерации в отношении движимого имущества, не освобожденного от налогообложения, не могут превышать в 2018 году 1,1%.

Регионы устанавливают на 2018 год как наличие льготы, так и размер ставки при ее отсутствии.

Для Москвы и Московской области на период с 2018 года по 2020 год установлена налоговая ставка в размере 0% в отношении движимого имущества, принятого организацией с 1 января 2013 года на учет в качестве основных средств, за уже известными исключениями.

Учитывая установление в Налоговом Кодексе РФ предельной ставки только на 2018 год, велика вероятность ее пересмотра на 2019 год и последующие периоды.

Все лучшее – детям!

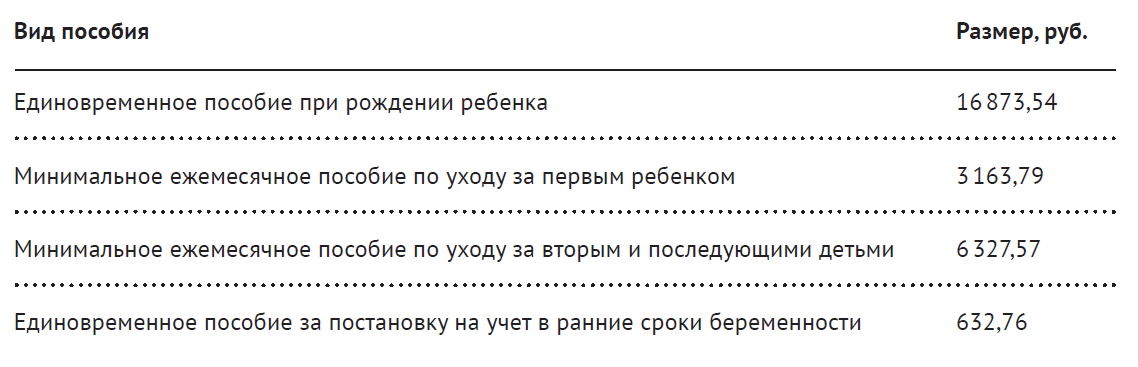

С 2018 года введены новые пособия на рождение (усыновление) первого и второго ребенка в семьях, среднедушевой доход в которых не превышает 1,5 кратную величину прожиточного минимума, установленного в субъекте РФ. Право на получение ежемесячной выплаты возникает при рождении (усыновлении) ребенка после 1 января 2018 года.

Ежемесячная выплата в связи с рождением (усыновлением) первого или второго ребенка осуществляется в размере прожиточного минимума для детей, установленном в субъекте Российской Федерации в соответствии с Федеральным законом от 24 октября 1997 года 134-ФЗ «О прожиточном минимуме в Российской Федерации» за второй квартал года, предшествующего году обращения за назначением указанной выплаты.

Прожиточный минимум на детей в целом по России составляет около 10 тысяч рублей.

Также в феврале 2018 года будут проиндексированы на коэффициент 1,032 пособия, выплачиваемые в связи с рождением ребенка.

В 2018 году пособия составят:

С 2018 года индексация «детских» пособий будет проходить ежегодно по состоянию на 1 февраля.

Амнистия по налогам физических лиц и индивидуальных предпринимателей

28 декабря 2017 года Президентом РФ был подписан законопроект, согласно которому налоговыми органами будут списаны недоимки физических лиц по транспортному налогу, налогу на имущество физических лиц, земельному налогу, образовавшиеся по состоянию на 1 января 2015 года, а также задолженности по пеням, начисленным на указанные недоимки.

Также будут списаны задолженности индивидуальных предпринимателей по страховым взносам «за себя», начисленные до 1 января 2017 года.

Решение о списании задолженностей принимается налоговым органом на основании данных о задолженностях физических лиц и индивидуальных предпринимателей.

Если в части задолженностей по налогам физических лиц администратором всегда являлась ФНС, то данные о страховых взносах были переданы в ФНС внебюджетными фондами только в прошлом году. При этом передача данных о начисленных и уплаченных страховых взносах (особенно по юридическим лицам) была произведена некорректно. У многих налогоплательщиков обнаружились давно погашенные задолженности, потерялись данные об уплате и данные деклараций за 2016 год.

Так как в прошлом году уже были прецеденты некорректного учета данных о расчетах по страховым взносам, индивидуальным предпринимателям, у которых есть задолженности, необходимо предварительно провести сверку с налоговым органом с целью полного списания задолженности.

Нет процентов? Будут!

С 1 июня 2018 года в случае, если в договоре займа прямо не указано, что заем является беспроцентным, проценты начисляются по ключевой ставке Банка России, действующей в период начисления процентов.

Указанные положения введены в статью 809 Гражданского Кодекса РФ. Теперь отсутствие упоминания о процентах в договоре не является основанием их не начислять.

Также установлено своеобразное предостережение относительно завышения размера процентов для заимодавцев юридических лиц, не осуществляющих профессиональную деятельность по предоставлению потребительских займов. Размер процентов за пользование займом по договору займа, заключенному между гражданами или между юридическим лицом и заемщиком-гражданином, в два и более раз превышающий обычно взимаемые в подобных случаях проценты и поэтому являющийся чрезмерно обременительным для должника, может быть уменьшен судом до размера процентов, обычно взимаемых при сравнимых обстоятельствах.

Отсрочка для ИП по уплате дополнительных страховых взносов

Дополнительные страховые взносы на обязательное пенсионное страхование уплачиваются индивидуальным предпринимателем в случае, если его доходы за год превышают 300 000 рублей в размере 1% от суммы превышения.

Срок уплаты дополнительных взносов раньше был установлен до 1 апреля года, следующего за отчетным периодом. Начиная с уплаты дополнительных страховых взносов по итогам 2017 года срок уплаты до 1 июля 2018 года.

Указанные изменения не дают больше времени для расчета суммы, так как срок подачи декларации по упрощенной системе налогообложения (самая распространенная система налогообложения у ИП) по-прежнему остается 30 апреля. Указанная норма дает исключительно отсрочку по уплате суммы страховых взносов, уплачиваемых исходя из фактически полученных доходов.

Внимательно заполняйте «Расчет по страховым взносам»

ФНС продолжает ужесточать порядок заполнения расчета по страховым взносам и санкции за его нарушение. За 2017 год плательщикам страховых взносов опять придется сдавать новую форму.

Срок подачи нового расчет по страховым взносам не изменился – до 30 января 2018 года

Расчет по страховым взносам не будет принят налоговыми органами в том случае, если при подаче будут обнаружены расхождения между разделами 1 (сводными данные по начислениям) и разделом 3 (персонифицированные данные).

В прошлом году налоговые органы принимали расчет с указанными расхождениями и требовали предоставить уточненный расчет. В 2018 году такие расхождения будут являться основанием для отказа и начисления штрафа, если плательщик страховых взносов не успеет в срок подать правильный расчет.

Продолжая тему страховых взносов, сообщаем, что предельная величина доходов физических лиц для начисления по стандартному тарифу в 2018 году составляет:

- для страховых взносов на социальное страхование – 815 000 рублей;

- для страховых взносов на обязательное пенсионное страхование – 1 021 000 рублей.

Пределов по взносам на обязательное медицинское страхование, по-прежнему, не установлено.

Материальная выгода физического лица: доход или нет?

В Налоговый Кодекс внесены поправки относительно налогообложения доходов физических лиц в виде материальной выгоды от экономии на процентах.

С 1 января 2018 года материальная выгода от экономии на процентах облагается НДФЛ только в случаях, если:

- доход получен от взаимозависимой организации (индивидуального предпринимателя) или работодателя;

- доход является материальной помощью или формой встречного исполнения обязательства перед физическим лицом.

Также с 1 января 2018 года, если организация прощает физическому лицу долг, то у него возникает доход (материальная выгода) в виде суммы прощенной задолженности только в том случае, если организация взаимозависима по отношению к физическому лицу.

Если факта взаимозависимости нет, то и дохода в целях уплаты НДФЛ не возникнет.

НДС – делим без порогов

До наступившего года обязанность по ведению раздельного учета была возложена на тех налогоплательщиков, сумма затрат по необлагаемым НДС операциям превышала 5% от общей суммы затрат.

С 2018 года раздельный учет необходимо вести всем налогоплательщикам, осуществляющим как деятельность, облагаемую НДС, так и деятельность, не облагаемую НДС. Правило 5% перестает действовать.

При этом право на признание вычетов по НДС по затратам, относящимся к необлагаемой деятельности в пределах 5% сохраняется.

Таким образом, указанные поправки усложняют учет, но не увеличивают налоговую нагрузку.

С Новым Годом, с новым отчетом!

До 1 марта 2018 года всем работодателям необходимо подать в Пенсионный фонд РФ новый отчет СЗВ-СТАЖ о страховом стаже своих работников.

СЗВ-СТАЖ заполняется и представляется страхователями на всех застрахованных лиц, находящихся со страхователем в трудовых отношениях или заключивших с ним гражданско-правовые договоры, предметом которых является выполнение работ.

В отчете необходимо указать всех своих работников, период работы в отчетном периоде, основания для начисления льготного стажа и прочие показатели.

Также с 1 января 2018 года вводятся новые формы деклараций по транспортному и земельному налогу. Декларация по земельному налогу не претерпела значительных изменений.

В новой декларации по транспортному налогу дополнительно необходимо будет указать:

- дату регистрации транспортного средства;

- дату снятия с учета транспортного средства;

- год выпуска транспортного средства;

- код налогового вычета;

- сумму налогового вычета (в рублях).

Срок подачи деклараций по транспортному и земельному налогам не изменился – до 1 февраля 2018 года.

Другие статьи по темам