В начале апреля 2020 года произошло множество изменений, направленных на поддержку бизнеса в непростое для всех время.

В этой статье освещены наиболее значимые изменения, относящиеся к тем отраслям, которые не признаются особо пострадавшими, а также рассмотрены некоторые меры поддержки малого и среднего бизнеса в пострадавших отраслях.

Бухгалтер может передохнуть

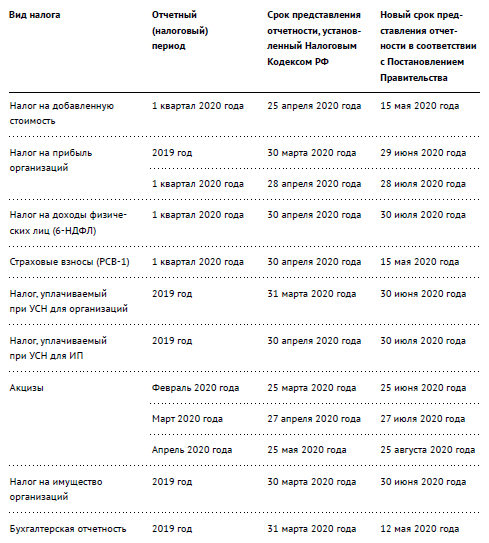

В связи с установлением режима нерабочих дней в апреле и начале мая 2020 года для всех организаций, были перенесены сроки представления отчетности и уплаты налогов, сборов и страховых взносов1.

Отчетность, срок представления которой, в соответствии с Налоговым Кодексом РФ, приходится на март-май 2020 года, может быть представлена на 3 месяца позже. Это актуально для:

- налоговых деклараций (за исключением налоговых деклараций по налогу на добавленную стоимость);

- налоговых расчетов о суммах, выплаченных иностранным организациям доходов и удержанных налогов;

- расчетов сумм налога на доходы физических лиц, исчисленных и удержанных налоговыми агентами;

- расчетов по авансовым платежам;

- бухгалтерской (финансовой) отчетности.

Налоговая декларация по НДС и Расчет по страховым взносам за 1 квартал 2020 года представляются в налоговый орган в срок до 15 мая 2020 года.

7 апреля Минфин и ФНС опубликовали разъяснения2, касающиеся сроков предоставления бухгалтерской отчетности за 2019 год (если такая бухгалтерская отчетность не регулируется специальными положениями, например, о государственной тайне). Эта отчетность представляется в налоговый орган в первый рабочий день после срока, установленного Налоговым Кодексом РФ, то есть – 6 мая 2020 года. Однако, после выступления Президента РФ и объявления 6-8 мая 2020 года нерабочими днями, срок представления был автоматически перенесен на 12 мая 2020 года.

Для удобства приведена сравнительная таблица по основным формам бухгалтерской и налоговой отчетности.

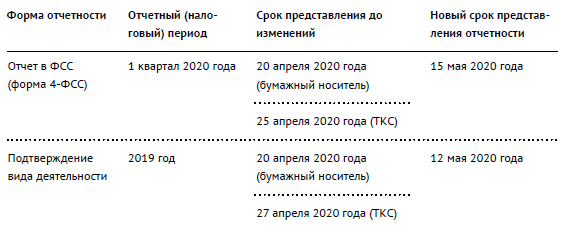

Сроки представления отчетности в Фонд социального страхования также были изменены:

Пенсионный фонд оказался наименее лояльным к плательщикам страховых взносов и не стал переносить сроки из-за объявления апреля нерабочим месяцем. Пенсионный фонд требует представлять СЗВ-М и СЗВ-ТД ежемесячно не позднее 15 числа месяца, следующего за отчетным. При нарушении указанного срока на плательщика страховых взносов и руководителя будут наложены штрафы.

Перенос сроков представления отчетности не влечет продление сроков уплаты налогов (авансовых платежей по налогам), в том числе в случае, когда в соответствии с Налоговым Кодексом РФ срок уплаты налога (авансового платежа по налогу) установлен не позднее даты представления налоговой декларации (расчетов).

Таким образом, возникает некоторый логический конфликт: представить отчетность можно позже, а вот уплата налога большинством организаций должна быть осуществлена в срок. Штрафы за просрочку оплат начисляться не будут и счета не заблокируют, но начисление пени за просрочку платежа никто не отменял.

Взносы в Пенсионный фонд стали меньше, но не для всех

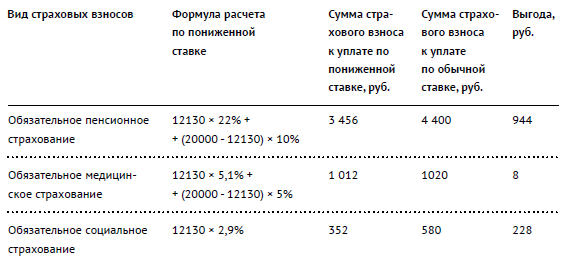

Плательщики страховых взносов, признаваемые субъектами малого и среднего предпринимательства, с 1 апреля 2020 года по 31 декабря 2020 года применяют следующие тарифы страховых взносов по оплате труда своих сотрудников (для части оплаты труда, превышающей МРОТ)3:

Более того, в Налоговый Кодекс РФ внесены поправки, продлевающие указанные тарифы на 2021 год и последующие годы4. То есть действовать такие тарифы будут вплоть до их изменения.

Для наглядности приведу пример расчета страховых взносов за апрель (подлежат уплате в мае 2020 года).

Пример.

Заработная плата сотрудника за апрель 2020 года составила 20 000 рублей. МРОТ, установленный федеральным законом5, составляет 12 130 рублей:

То есть, выгода действительно составляет 15%, но пониженные тарифы применяются с суммы заработка сотрудника, превышающего МРОТ, а не со всей суммы. Тем не менее, понижение существенное (в два раза), особенно для тех работодателей, которые платят своим сотрудникам высокие зарплаты.

Такие меры направлены сразу на достижение двух целей:

- снижение налоговой нагрузки на малый и средний бизнес;

- дополнительный стимул для «повышения» оплаты труда сотрудников.

Часть зарплаты за счет бюджета

Для организаций, осуществляющих вид деятельности, признанный особо пострадавшим от распространения вирусной инфекции, Правительство РФ утвердило правила6 предоставления субсидий в целях частичной компенсации затрат, в том числе на оплату труда своих сотрудников в апреле и мае 2020 года.

Размер субсидии составляет сумму МРОТ по состоянию на 1 января 2020 года или 12 130 рублей.

Предоставляется субсидия тем организациям и предпринимателям, кто по состоянию на 1 марта 2020 года вел основную деятельность в пострадавших отраслях. Налоговым органом составляется реестр организаций, претендующих на получение субсидии. Для включения в реестр должны выполняться следующие условия:

- организация или предприниматель должны быть указаны в реестре субъектов МСП по состоянию на 1 марта 2020 г.;

- получатель субсидии не находится в процессе ликвидации, в отношении него не введена процедура банкротства, не принято решение о предстоящем исключении из ЕГРЮЛ;

- по состоянию на 1 марта 2020 г. отсутствует недоимка по налогам и страховым взносам, в совокупности превышающая 3000 руб.;

- количество работников получателя субсидии в месяце, за который выплачивается субсидия, составляет не менее 90% количества работников в марте 2020 г.

Для получения субсидии организации необходимо подать заявление в налоговый орган по ТКС, через личный кабинет или в виде почтового отправления.

Для получения субсидии за апрель 2020 года организация направляет заявление в налоговый орган в период с 1 мая до 1 июня 2020 года, для получения субсидии за май 2020 года — с 1 июня до 1 июля 2020 года.

При отсутствии оснований для отказа в предоставлении субсидии налоговый орган в течение 3 рабочих дней со дня направления заявления, но не ранее 18-го числа месяца, следующего за месяцем, за который предоставляется субсидия, производит расчет размера субсидии, формирует реестр и направляет его в Федеральное казначейство.

Перечисление субсидии осуществляется Федеральным казначейством не позднее 3 рабочих дней со дня, следующего за днем получения Федеральным казначейством реестра.

Не обошлось и без ложки дёгтя

После заявления Президента в состав поправок к Налоговому Кодексу РФ вошла и поправка7 о введении нового объекта налогообложения налогом на доходы физических лиц.

С 1 января 2021 года обложению НДФЛ подлежат проценты по всем вкладам (остаткам на счетах) в банках, находящихся на территории РФ, по ставке 13%.

То есть, теперь даже с очень скромных сумм процентов по депозитам будут взиматься налоги. Однако, не стоит спешить снимать денежные средства со своих счетов до конца 2020 года, так как:

- процентные доходы, полученные в 2020 году, не подлежат обложению;

- налоговая база определяется как превышение суммы доходов в виде процентов, полученных налогоплательщиком в течение налогового периода по всем вкладам (остаткам на счетах) в указанных банках, над суммой процентов, рассчитанной как произведение одного миллиона рублей и ключевой ставки Центрального банка Российской Федерации, действующей на первое число налогового периода;

- не подлежат обложению доходы в виде процентов, полученных по вкладам (остаткам на счетах) в рублях, процентная ставка по которым в течение всего налогового периода не превышает 1 процента годовых;

- не подлежат обложению доходы по счетам эскроу.

То есть, если брать за основу текущую ключевую ставку (5,5%), то в общем порядке обложению будет подлежать сумма процентов, полученная налогоплательщиком за год, за вычетом 55 000 рублей.

Если доходы по вкладам номинированы в валюте, то такие доходы пересчитываются в рубли по официальному курсу Центрального банка Российской Федерации, установленному на дату фактического получения дохода (поступления денежных средств).

Отчетность по полученным процентам физическим лицам подавать не придется. Налог уплачивается не позднее 1 декабря года, следующего за истекшим налоговым периодом (календарным годом), на основании направленного налоговым органом налогового уведомления об уплате налога. Сведения о доходах физических лиц (своих клиентах) подают банки.

- Пункт 3 Постановления Правительства РФ №409 от 02.04.2020 г.

- Письмо Минфина и ФНС N 07-04-07/27289 от 07.04.2020 г.

- Статья 6 Федерального закона от 01.04.2020 № 102-ФЗ.

- Подпункт 9 статьи 2 Федерального закона от 01.04.2020 № 102-ФЗ.

- Федеральный закон от 27.12.2019 N 463-ФЗ «О внесении изменений в статью 1 Федерального закона «О минимальном размере оплаты труда».

- Постановление Правительства РФ №576 от 24.04.2020 г.

- Статья 2 Федерального закона от 01.04.2020 № 102-ФЗ.

Другие статьи по темам